Are We Approaching Peak Retirement?

If stocks, bonds and real estate all decline going forward, where are pension funds going to earn their 7+% annual yields?

If we look at the foundations of retirement--Social Security, stocks, bonds and real estate--it seems we may have reached Peak Retirement. Let's start the discussion by noting that the primary Federal retirement programs--Social Security and Medicare--are "pay as you go," meaning the checks sent out to beneficiaries this year are funded by payroll tax revenues collected this year from workers.

As Mish and I (as well as others) have tirelessly pointed out, the "trust funds" for these programs are phantoms of imagination. When these programs run deficits, the government raises the money to fund the deficit the same way it funds all its deficit spending--by selling Treasury bonds.

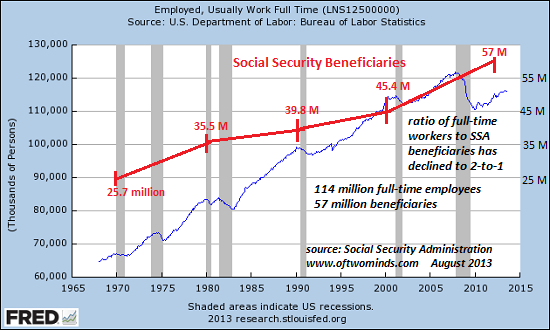

These programs were founded on a demographic illusion, i.e. that the number of retirees (beneficiaries) would magically remain a small percentage of the workforce paying payroll taxes. Alas, the number of beneficiaries is rising fast while the number of full-time workers is stagnating.

Full-time employment and the number of Social Security beneficiaries: the ratio of full-time workers to beneficiaries is already 2-to-1, and set to decline. Below 2-to-1, either payroll taxes will have to icnrease or benefits will have to be trimmed, or some of both.

Public and private pensions are based on earning 7+% returns on investments in stocks, bonds and real estate. Let's look at each asset class and reckon the likelihood of it earning 7+% into the future.

The stock market has traced out a multi-year megaphone pattern that presages a decline to a new low: if this megaphone pattern plays out, the S&P 500 could plummet from its current level around 1700 to the 600 level. Were that to occur, pension funds holding stocks would suffer catastrophic losses.

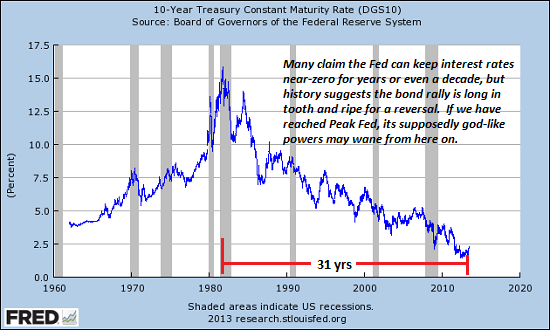

Bonds are ripe for a reversal: as bond yields decline, the market value of existing bonds rises. This also works in the other direction: as yields, rise, the market value of all existing bonds declines. If the god-like powers of the Federal Reserve turn out not to be so god-like and interest rates rise, the market value of all existing bonds could fall dramatically.

Bond market trends rarely last 30 years, so the trend of falling yields is extremely long in tooth and ripe for a reversal, for example, 10 to 15 years of rising interest rates and declining bond values:

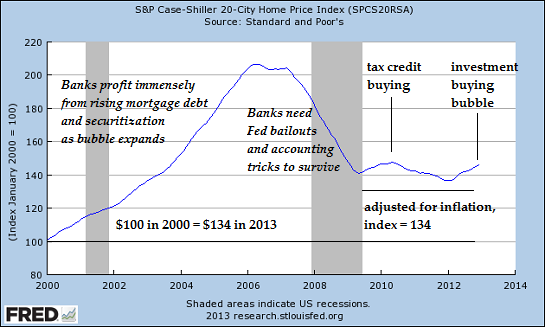

Housing has rebounded weakly, but only as a result of unprecedented intervention by the Federal Reserve and the Federal government: The Fed drove mortgage rates to historic lows, bought over $1 trillion in mortgages and Federal housing agencies such as FHA guaranteed 3% down payment mortgages to just about anyone with a full-time job and a middling credit rating.

Banks have held tens of thousands of defaulted homes off the market to induce an artificial scarcity to drive prices higher. Meet The Monster Of The Housing Market: Presenting "Vampire REOs" Where Half Live Mortgage-Free (Zero Hedge)

All this trillion-dollar manipulation and intervention generated the weak bounce that is now ending.

If stocks, bonds and real estate all decline going forward, where are pension funds going to earn their 7+% annual yields? Please don't say "emerging markets," for those markets are imploding (see India as an example) under the weight of speculative excess, asset bubbles, capital flight, and to-the-moon credit expansion.

If pension funds lose significant percentages of their assets to market declines, earning 7% will be the least of the problems. As for the Federal retirement programs: if the erosion of full-time employment continues as a long-term trend, Social Security and Medicare will both start running massive deficits as the number of Baby Boomer beneficiaries continues rising while the payroll tax base shrinks.

Posts and email responses will be sporadic in October due to family commitments. Thank you for your understanding.

The Nearly Free University and The Emerging Economy:

The Revolution in Higher Education

Reconnecting higher education, livelihoods and the economy

We must thoroughly understand the twin revolutions now fundamentally changing our world: The true cost of higher education and an economy that seems to re-shape itself minute to minute.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Once we accept responsibility, we become powerful.

Kindle: $9.95 print: $24

| Thank you, Arne P. ($25), for your much-appreciated generous contribution to this site-- I am greatly honored by your support and readership. |