Have We Reached Peak Federal Reserve?

As the Fed-induced asset bubbles in stocks, bonds and real estate follow the inevitable Supernova track to implosion, that we've reached Peak Federal Reserve will be obvious--in hindsight.

Billionaires and political lackeys alike have been falling all over themselves in the rush to praise the Federal Reserve's unprecedented monetary intervention since 2008. That billionaires and political hacks, apparatchiks and toadies cannot laud the Fed's Cargo Cult enough is no surprise: the billionaires and the government that feeds them both gained handsomely from the Fed's policies:

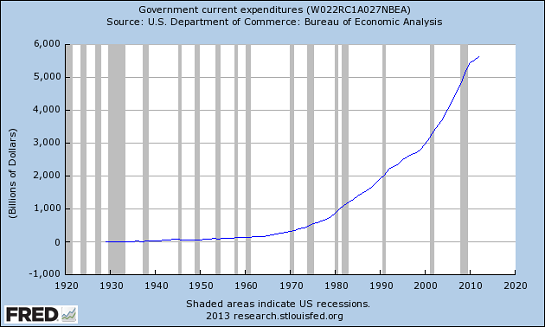

Government spending: up strongly since the Fed began pumping nearly-free credit and ample liquidity.

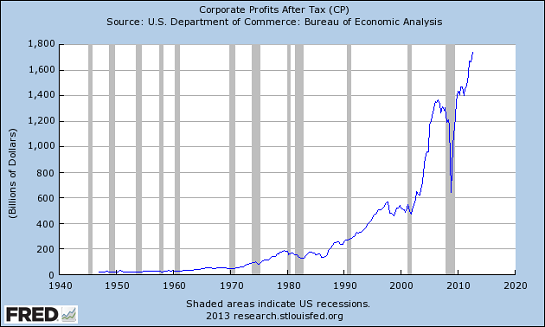

Corporate profits: soaring to new heights in the Fed-Bubble Era.

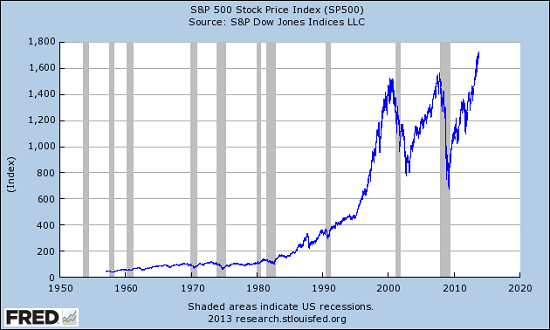

S&P 500: new nominal highs for stocks in the Fed-Bubble Era.

But what about the consequences for the non-billionaire, non-government, non-financial real economy?

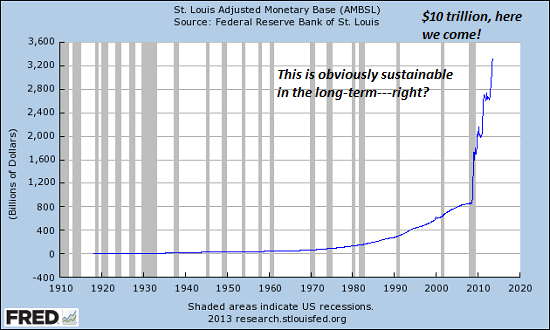

Monetary base: this is what happens when the Fed creates money out of thin air to buy Treasury bonds and mortgages. Does this look remotely sustainable in the long-term?

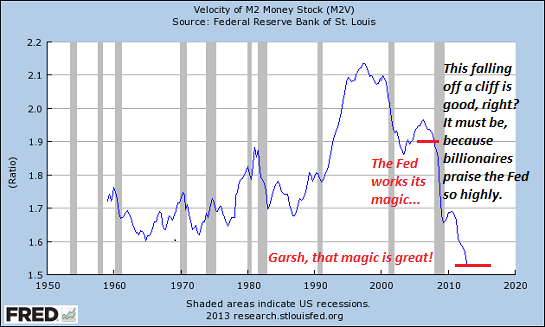

Money velocity: in a strong economy, money velocity is high (for example, the mid-1990s) and weak in recessions (for example, 1973, 1982 and 2002). Money velocity has fallen to unprecedented levels, lower than any recession of the past 40 years.

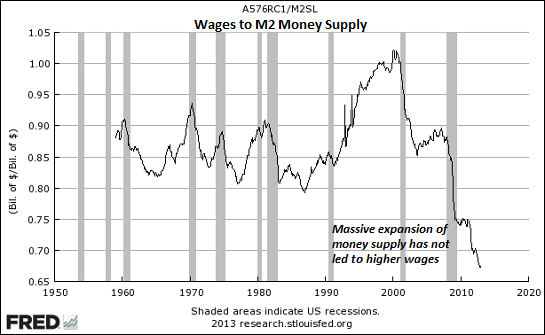

Here's what all that Fed magic (jacking up money supply and lowering interest rates to near-zero) accomplished in terms of wages:

Here is household income, adjusted for inflation since 2000: it's hard to overstate how successful the Fed's policies have been in the real economy; no wonder billionaires and political toadies can't praise the Fed enough. Real household income only fell 7.2% under the Fed's billionaire-politico-friendly policies.

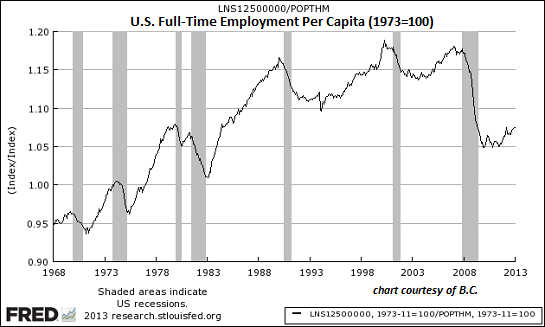

Employment per capita: this is employment adjusted for population growth: back to the levels of the late 1970s.

Full-time employment: all the way up to the same level of 13 years ago, while the U.S. population grew by 28%.

These charts provide ample evidence that we've reached Peak Federal Reserve: its monetary policies (zero interest rate policy--ZIRP, quantitative easing--QE, purchasing $1+ trillion home mortgages to jack up the housing market, etc.) have boosted the fortunes of billionaires and free-spending, easily-bought politicos but left wages and employment to stagnate.

All the Fed's goodies for the billionaires--the assets bubbles in stocks, bonds and real estate--have reached the point of "as good as it gets." From here on in, these bubbles have nowhere to go but down. As the Fed-induced asset bubbles follow the inevitable Supernova track to implosion, that we've reached Peak Federal Reserve will be obvious--in hindsight.

The Nearly Free University and The Emerging Economy:

The Revolution in Higher Education

Reconnecting higher education, livelihoods and the economy

We must thoroughly understand the twin revolutions now fundamentally changing our world: The true cost of higher education and an economy that seems to re-shape itself minute to minute.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Once we accept responsibility, we become powerful.

Kindle: $9.95 print: $24

| Thank you, Boris P. ($5/month), for your wondrously generous subscription to this site-- I am greatly honored by your support and readership. |