If conventional labor and finance capital have lost their scarcity value, then the era in which financialization reaped big profits is ending.

Why is wealth/income inequality soaring? The easy answer is of course the infinite greed of Wall Street fat-cats and the politicos they buy/own.

But greed can't be the only factor, for greed is hardly unknown in the bottom 90%. The only difference between the guy who took out a liar loan to buy a house he couldn't afford so he could flip it for a fat profit and the mortgage broker who instructed him on how to scam the system and the crooked banker dumping toxic mortgage-backed securities on the Widows and Orphans Fund of Norway is the scale of the scam.

The difference isn't greed, it's the ability to avoid the consequences or have the taxpayers eat the losses, i.e. moral hazard. The bottom 90%er with the liar loan mortgage and the flip-this-house strategy eventually suffered the consequences when Housing Bubble 1.0 blew up in spectacular fashion.

Moral hazard describes the difference between decisions made by those with skin in the game, i.e. those who will absorb the losses from their bets that go south, and those who've transferred the risks and losses to others.

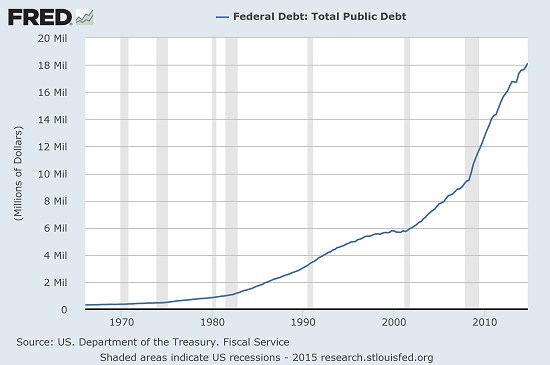

The too-big-to-fail banks that bought political protection simply shifted the losses to taxpayers. Then the Federal Reserve helpfully paid banks for deposits at the Fed while reducing the amount banks had to pay on depositors' savings to near-zero, effectively rewarding the banks with free money for ripping off the taxpayers.

America's financialized cartel-state system institutionalizes moral hazard. This is one cause of rising inequality, as the super-wealthy are immunized by their purchase of political influence.

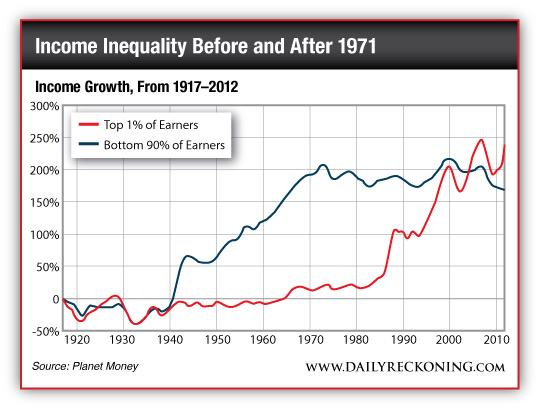

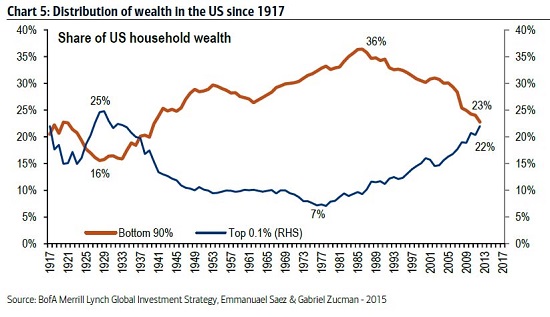

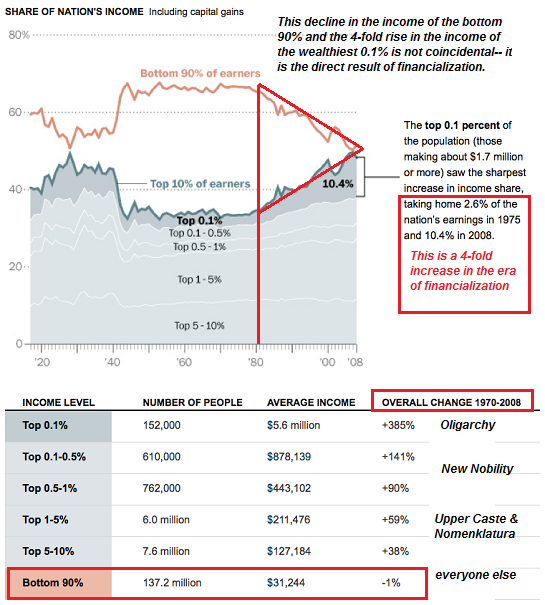

The top .1%'s share of the pie has been rising in the era of financialization and institutionalized moral hazard:

But that may not be enough to describe the decades of stagnation in incomes of the bottom 90%.

The U.S. economy (along with the global economy) is undergoing a sea change equivalent to an industrial revolution, only this time it isn't just industrial, it's digital.

What's scarce is changing, and since profits flow to what's scarce, that's upending the whole chain of value creation. As Erik Brynjolfsson, Andrew McAfee, and Michael Spence explain in their 2014 article

New World Order: Labor, Capital, and Ideas in the Power Law Economy, the gains from the digital economy follow a

power law distribution: the few at the top reap the majority of the gains while the dregs are distributed to the majority below.

This is akin to the Pareto Distribution, something I have mentioned here many times over the years. This is also known as the 80/20 rule, as the top 20% typically gather 80% of whatever economic unit is being measured: land, sales, etc.

The 80/20 rule distills down to the 64/4 rule, as 80% of 80 is 64 and 20% of 20 is 4:the top 4% reap 64% of the gains.

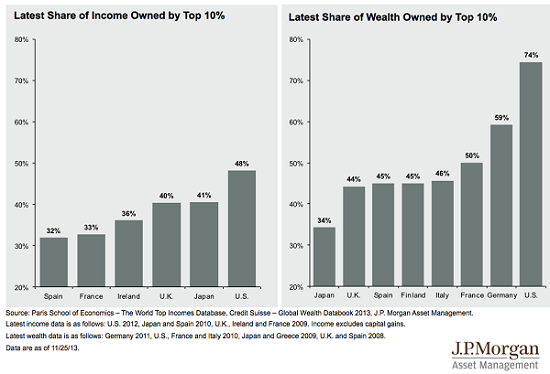

We can see that the top 10% in the U.S. own 74% of the wealth--a rough approximation of the Pareto Distribution:

Spence et al.: Machines are substituting for more types of human labor than ever before. As they replicate themselves, they are also creating more capital. This means that the real winners of the future will not be the providers of cheap labor or the owners of ordinary capital, both of whom will be increasingly squeezed by automation. Fortune will instead favor a third group: those who can innovate and create new products, services, and business models.

The distribution of income for this creative class typically takes the form of a power law, with a small number of winners capturing most of the rewards and a long tail consisting of the rest of the participants. So in the future, ideas will be the real scarce inputs in the world -- scarcer than both labor and capital -- and the few who provide good ideas will reap huge rewards.

Higher education is one example of the declining scarcity value of old models of labor and capital. When college degrees were scarce, college graduates commanded a high scarcity value. Now that tens of millions of people have degrees, the scarcity value is falling dramatically.

In response, people have worked their way up the academic food chain, earning masters degrees and PhDs. But now many of these advanced degrees are also over-abundant, and the scarcity value of MBAs, etc. is declining.

These realities will have major impacts. If conventional labor and finance capital have lost their scarcity value, then the era in which financialization reaped big profits is ending.

If labor has little scarcity value, and productive ideas are what's now scarce, then what has leverage isn't a college degree--it's the ability to move across multiple fields of knowledge, learning new skills and seeking out new collaborations--the attributes of what I call

mobile creatives, a new class I describe in my book

Get a Job, Build a Real Career and Defy a Bewildering Economy.

We can't wait around hoping the Power Elites relinquish their lock on monetary and political power: we have to individually seek out what's scarce in the emerging economy and learn the skills and make the connections to move up the value creation scale on our own power.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Susan B. ($50), for your monumentally generous contribution to this site -- I am greatly honored by your support and readership.

| |

Thank you, Gerard F. ($50), for your splendidly generous contribution to this site -- I am greatly honored by your support and readership.

|

Read more...