If We Don't Change the Way Money Is Created and Distributed, We Change Nothing

The only real solution in my view is to create and distribute money at the base of the pyramid rather than to those in the top of the pyramid.

Many well-intended people want to reform the status quo for all sorts of worthy reasons: to reduce wealth inequality, restore democracy, create good-paying jobs, and so on.

All these goals are laudable, but if we don't change the way money is created and distributed, nothing really changes: wealth inequality will keep rising, governance will remain a bidding process of the wealthy, wages will continue stagnating, etc.

If the money creation/distribution system isn't transformed, "reform" is nothing more than ineffectual policy tweaks that offer do-gooders the illusion of progress.

Mike Swanson of Wall Street Window and I discuss the The Future of Currencies and CHS's New Book A Radically Beneficial World (33:21)

Few are willing to admit that the way we create and distribute money at the top of the wealth pyramid necessarily generates increasing wealth inequality because once we admit this, we realize 1) the money system itself is the source of inequality and 2) we have to change the money system if we want to stave off the inevitable rise of wealth inequality to the point that it generates social disorder.

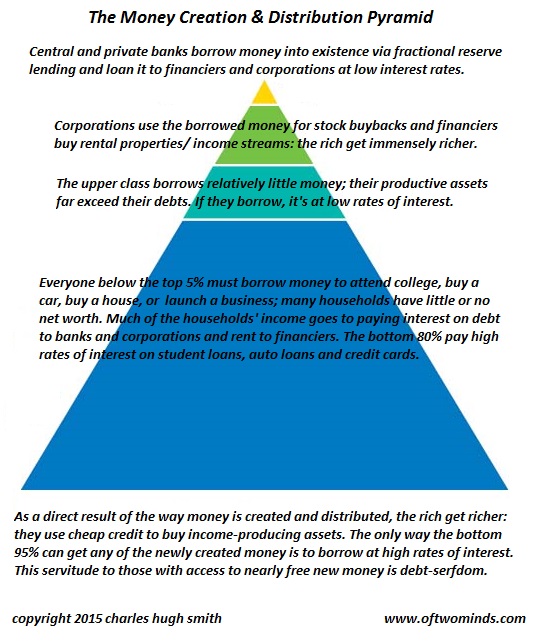

In the current system, money is created by central and private banks at the top of the wealth/power pyramid, and distributed within the top of the wealth pyramid. The only possible output of this system is rising wealth inequality and debt-serfdom for three reasons:

1. Those with first access to nearly free money can outbid savers and serfs who must borrow at much higher rates of interest to snap up income-producing assets. In effect, borrowing unlimited sums at near-zero rates guarantees that those with this privilege have a built-in advantage in buying income-producing assets. The only possible output of this system is the rich get richer as they buy up all the most profitable and lowest-risk income-producing assets.

2. Those who can borrow virtually unlimited sums at less than 1% interest skim vast wealth by loaning the money out to everyone below the top of the pyramid at 4% (mortgages), 8% (other loans), and 18% (credit cards). This funnels much of the national income stream to those who can borrow cheap and lend the money at much higher rates.

3. Since the wealthy already own most of the income-producing assets, the easiest way to boost their wealth is to bid up those assets with cheaply borrowed money. For example, borrowing $100 million and using it for stock buybacks leverages the value of the shares by far more than $100 million.

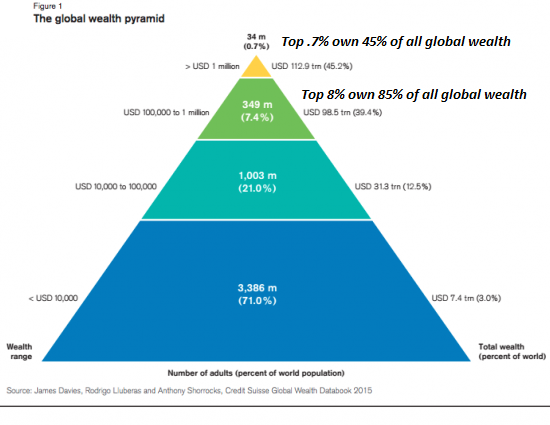

Three different perspectives of the wealth pyramid illustrate how our money system generates wealth inequality as the only possible output of the system:

The system of central banks, private banks and fractional reserve lending is global. The net result is that globally, the vast majority of wealth is owned and controlled by those at the very apex of the wealth/power pyramid: the top 8% own 85% of global wealth.

In the U.S., the wealth-income pyramid can be represented by an inverted pyramid: the bulk of wealth and income are in the hands of the top 5%. The bottom 80% own an essentially trivial percentage of the national wealth.

This pyramid illustrates how the money creation and distribution pyramid works:

There are a number of proposed alternatives to this the rich can only get richer and the rest of us can only get poorer system. The only real solution in my view is create and distribute money at the base of the pyramid, to those generating useful goods and services in the community economy, rather than to those in the top of the pyramid. This money isn't borrowed into existence, so there is no interest to be skimmed by its creation.

I explain how this works in my new book A Radically Beneficial World: Automation, Technology and Creating Jobs for All.

Mike Swanson and I cover many other related topics in this podcast: The Future of Currencies and CHS's New Book A Radically Beneficial World (33:21)

My new book is in the top 10 of Amazon's category of international economics: A Radically Beneficial World: Automation, Technology and Creating Jobs for All. The Kindle edition is $8.45, a 15% discount from its list price of $9.95.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, David B. ($50), for your splendidly generous contribution to this site--I am greatly honored by your support and readership.

|