Housing: The Foundations of the Middle Class Are Crumbling

Bottom line: with the loss of predictability, we've also lost any sense of future financial security.

Home ownership has been the foundation of middle-class stability and security for so long that it defines middle-class status as much as income. From the end of World War II in 1945 on, the deal was simple: buy a house and you'll build equity that's even better than a savings account because you get the tax break of deducting mortgage interest and you get a roof over your head at a cost that's equal to or even lower than renting a house. Once you've paid off the mortgage, the costs of ownership drop, enabling a secure retirement.

Every one of these assumptions has either crumbled or is now in doubt. A recent report in The Guardian sketches out the forces undermining housing as the source of security:

'I feel trapped': how home ownership has become a nightmare for many Americans

Scores in the US say they're grappling with raised mortgage and loan interest rates and exploding insurance premiums.

"I've come to view home ownership and healthcare as destabilizing forces in my life," said Bernie, a 45-year-old network engineer from Minneapolis. To finance owning his and his wife's $300,000 home and saving for the future, the couple was foregoing medical and dental treatment of any kind and cutting back on expenses everywhere, he said, despite a pre-tax household income of more than $250,000.

Let's break down what's changed:

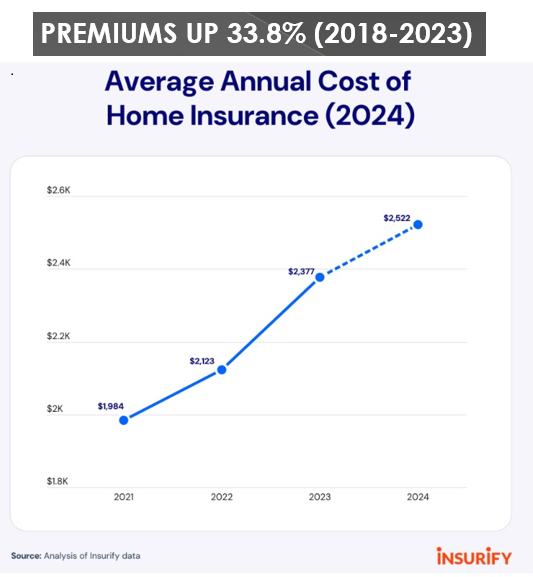

1. The non-mortgage costs of ownership are no longer predictable or affordable. For decades, the cost to insure one's home was modest and predictable, not changing much year to year. Now that insurers are losing billions of dollars as a result of increasingly extreme weather events, rates are rising even in places outside flood, fire and hurricane zones.

Insurance rates are doubling or tripling in a few years, and insurers are leaving markets entirely or increasing the deductible that must be paid by the owners before insurance kicks in, and reducing the coverage.

Property taxes are soaring in many locales. Property taxes were another cost that was relatively modest and predictable. Those conditions no longer apply in many locales: local governments are jacking up property taxes, and / or soaring home valuations are pushing taxes up to nosebleed levels. (I just looked up the annual property tax on a friend's house in California: north of $18,000 a year. And no, it's not a mansion in Malibu, and he bought it 20 years ago.)

The costs of home repairs and maintenance are also skyrocketing. The average age of homes in the U.S. is around 40 years, but closer to 50 years in slow-growth states. As the quality of materials and construction have slowly declined, even houses that are 25 years old or less may require costly repairs--especially if construction defects were undiscovered until major damage had been done.

Routine work such as trimming large trees that pose risks to houses now cost a small fortune. The Guardian article noted estimates for a new roof of $60,000, a sum that equals the construction cost of an entire new house two generations ago. Eye-watering costs of materials are now the norm.

Again, the major changes are not just in costs, but in the loss of predictability. What was modest in cost was not just modest, it was predictable. Now the costs are far higher and future costs cannot be assumed to be affordable.

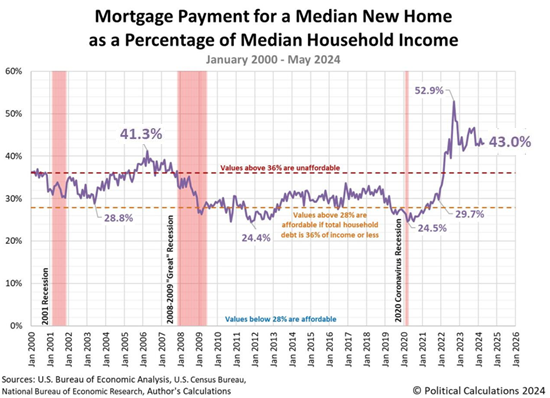

2. Mortgage costs are also higher, and there's no guarantee interest rates will fall back to 3.5% mortgage rates.

As this chart illustrates, the cost of servicing today's mortgages is significantly higher than in years past.

3. Those who locked in low mortgage rates are trapped in their current homes, as they can't afford to move and pay interest rates that are 50% to 100% higher than the low rates they secured years ago. The Federal Reserve intervened massively in the private mortgage market in the post 2008 era, effectively socializing the mortgage market as the means to push mortgage rates down to encourage "growth."

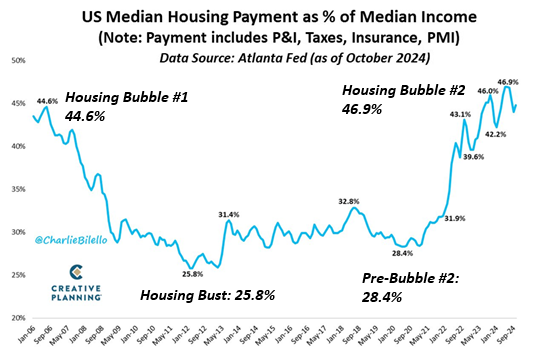

The Fed's intervention helped inflate Housing Bubble #2, just as the subprime excesses of the early 2000s helped inflate Housing Bubble #1. These distortions were intended to fuel home buying, but they also fueled massive increases in housing valuations.

4. The total costs of ownership--the monthly nut including mortgage and other costs--now exceeds the peak in Housing Bubble #1. Buying a house now is not a guaranteed pathway to financial security, it's a wager that valuations will continue to soar ever higher, generating capital gains that will offset the decades of higher costs of ownership.

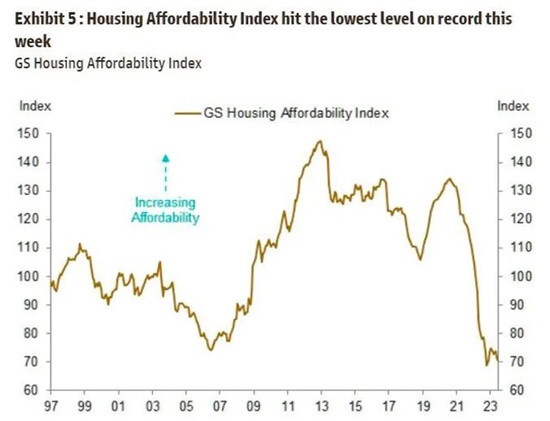

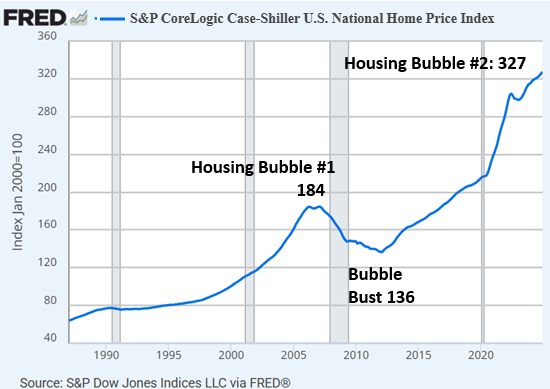

5. The triple-whammy of soaring valuations, mortgage rates and other costs of ownership has made housing unaffordable in many locales. By any measure, housing affordability has declined to levels that equal or exceed the trough of Housing Bubble #1.

The Case Shiller National Housing Index offers a snapshot of Housing Bubble #2.

6. Land, materials and labor are no longer cheap. In traditional economics, the high costs of housing can be reduced by reducing demand or increasing supply. Increasing supply at affordable prices is far more challenging now than in the postwar decades. The easy-to-build land was built out long ago, and high-rise condominiums come with higher construction costs and the uncertainties of common-area expenses, which in some cases skyrocket to equal or exceed the costs of ownership.

Proponents of building more housing in urban / suburban areas--YIMBYs--yes in my back yard--face hurdles of geography, aging infrastructure, parking, and the high costs of insurance, mortgages, materials and labor, along with many restrictive zoning and planning regulations designed to maintain the status quo.

As for reducing demand: the population of the U.S. was 265 million in 1995, and it's now 345 million: an increase of 80 million people, roughly the same as the entire population of Germany (83 million).

7. The costs of housing have opened generational and regional divides. Boomers and Gen-Xers who bought homes decades ago in the 1990s or early 2000s locked in much lower purchase prices and had multiple opportunities to refinance mortgages at lower rates as the Fed interventions pushed rates down. Recent buyers have no equivalent set of built-in advantages.

Regional divides are increased. A modest home purchased in a middle-class urban area decades ago has increased 10-fold in some areas and not even kept up with inflation in others. The winners are now sitting on a million dollars in equity, a windfall the less fortunate did not reap.

As the urban winners cash in their equity and move to desirable towns, they quickly bid up housing to the point local residents can no longer afford to buy a home in their hometown. And since the wealthy also snap up housing as investment properties--short-term vacation rentals--households that would be considered middle-class by income are doomed to being renters.

"Middle class" is no longer middle-class, it's a seat in the casino that most exit as losers.

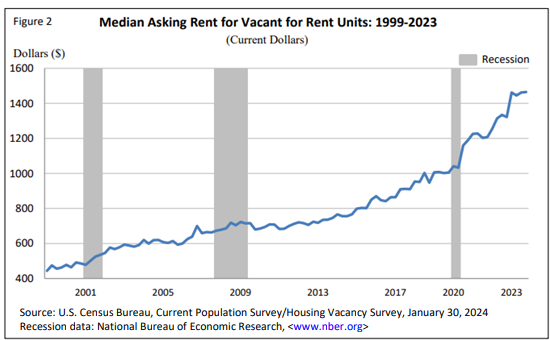

8. Renting is no longer a cheaper option. Rents have soared along with home prices, and once again, the predictability of future costs has vanished: rents can increase 30% overnight, just as insurance and property taxes can leap up far beyond anyone's projections.

Bottom line: with the loss of predictability, we've also lost any sense of future financial security. Buying a house is now a wager: a wager that the costs of ownership won't stair-step up to eat us alive, and a wager that valuations will continue to rise, offsetting the high costs of ownership with future capital gains.

Should Housing Bubble #2 pop--and all bubbles eventually pop--then homeowners will be dealt a future of ever-higher costs of ownership even as their equity diminishes. Those sitting on a wealth of equity now may find the assumption that this equity is predictably permanent is itself a wager.

The middle class was fundamentally defined by predictable financial security and social stability. Now everything is a wager with unknowable odds. Rather than being a source of stability, housing is now a source of instability for many--and potentially for every homeowner, should costs of ownership continue increasing as Housing Bubble #2 pops.

My recent books:

Disclosure: As an Amazon Associate I earn from qualifying purchases originated via links to Amazon products on this site.

The Mythology of Progress, Anti-Progress and a Mythology for the 21st Century print $18, (Kindle $8.95, Hardcover $24 (215 pages, 2024) Read the Introduction and first chapter for free (PDF)

Self-Reliance in the 21st Century print $18, (Kindle $8.95, audiobook $13.08 (96 pages, 2022) Read the first chapter for free (PDF)

The Asian Heroine Who Seduced Me (Novel) print $10.95, Kindle $6.95 Read an excerpt for free (PDF)

When You Can't Go On: Burnout, Reckoning and Renewal $18 print, $8.95 Kindle ebook; audiobook Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States (Kindle $9.95, print $24, audiobook) Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet (Kindle $8.95, print $20, audiobook $17.46) Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook) Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel) $4.95 Kindle, $10.95 print); read the first chapters for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print) Read the first section for free

Become a $3/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Glenn B. ($70), for your marvelously generous subscription to this site -- I am greatly honored by your support and readership. |

Thank you, Dermot W. ($7/month), for your superbly generous subscription to this site -- I am greatly honored by your support and readership. |

|

|

Thank you, Dan M. ($70), for your magnificently generous subscription to this site -- I am greatly honored by your support and readership. |

Thank you, Thomas1760 ($70), for your splendidly generous subscription to this site -- I am greatly honored by your support and readership. |