When US Treasuries Play a Reverse Card

Rather than being sold, Treasuries will be sought after for their safety, predictability and yield.

In the card game Uno, playing a Reverse card reverses the direction of the game. If the play moved to the right, it reverses direction and moves to the left.

The consensus view is the US dollar (USD) and US Treasuries are both weakening as global capital flows to other currencies and investments such as cryptocurrencies, commodities, precious metals, reshoring industries and of course AI.

It would surprise quite a few players if US Treasuries play a Reverse card and capital flows out of current darlings and into Treasuries. How is this even possible, given that the USD is on a terminal trajectory to zero due to out-of-control federal borrowing / debt?

Here's how the Reverse card scenario plays out. All the current investment darlings are based on two conditions that are currently locked away in the Denial Basement:

1. Virtually every asset class other than commercial real estate is in a gargantuan, unprecedented bubble that will track all the other bubbles in history by popping, surprising everyone who believes the extreme valuations are fully justified and therefore not a bubble.

2. The essentially limitless expansion of the money supply and public / private debt driving the global asset bubble has been normalized, i.e. accepted as "the way it is," a condition that is sustainable based on the self-serving fantasy that AI and technology are ushering in an era of super-abundance of everything we value: energy, resources, leisure and of course financial wealth.

Unbeknownst to those who believe that the Denial Basement is impenetrable, the Monster Id is currently melting the thick steel walls like they're butter. All bubbles pop for the same reason all extremes reverse: the pendulum--of excess, momentum, euphoria, greed, confidence, hubris--reaches a point of exhaustion and then gravity takes hold and the swing to the other extreme gathers momentum.

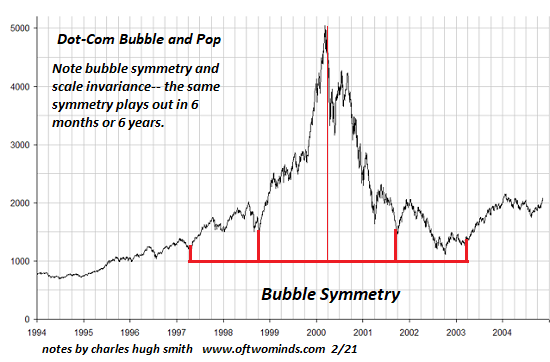

When asset bubbles pop, there's a symmetry to its collapse. The initial decline mirrors the last push to the peak. Since this final push higher is generally near-verticial, the drop is the reverse: a steep decline.

The smartest money missed profiting from the bubble peak due to prioritizing return of capital rather than return on capital. (Hence Buffett's $400 billion stash of cash.)

The smart money kept dancing as long as the music was playing, but once the music stopped, they noticed the bow of the Titanic was dipping lower into the icy waters of the North Atlantic. Those tasked with protecting the capital of the wealthy revert from greed (maximizing return on capital) to safety: return of capital.

The credulous money remains greedy, and continues to "buy the dip" until their capital is depleted. Due to this "buy the dip" buying, the collapse of the bubble back to its initial starting point is frequently interrupted by manic bear market rallies that inspire a fervent belief that "the bottom is in" so it's time to buy, buy, buy.

Alas, nature and markets are not always warm and fuzzy, and since the conditions that inflated the bubble are no longer controlling the game, the dynamics have changed, and "buy the dip" only works for short-term players.

Those tasked with protecting the capital of the wealthy seek two things: investments that guarantee a return of capital and some positive yield / return on capital. A handful of sovereign bond markets offer both.

Why only a handful? For these reasons:

1. Liquidity. Since there's several hundred trillion dollars sloshing around global asset markets, the ideal bond market is liquid enough that money managers can move tens of billions of dollars in and out without moving the bid and ask much.

2. Stable currency valuations set by the market, not the issuing state. There's one threat to the desired return of capital that money managers can't control: the valuation of the underlying currency. A 4% yield looks inviting, but if the issuing state suddenly devalues the currency by 10%, the positive gain reverses into a loss. So the ideal bond market is based on a liquid, transparent currency that can't be devalued by central state / central bank decree.

Any currency that's pegged to another currency, either formally or informally, is disqualified as the valuation is hostage to A) arbitrary decrees changing the peg and B) changes in the underlying currency. In summary: the currency underlying the bond market is the risk.

Superman looks invincible until the Kryptonite Monkey of currency devaluation jumps on his back.

3. A solid, transparent foundation comprised of A) the diversity and strength of the issuing nation's economy and B) the predictability / stability of the legal and financial systems governing the bond market.

As raising cash and escaping risk become paramount, the bubble popping spreads to all asset classes. Everything eventually gets sold to raise cash / pay down debt, including safe haven assets.

As capital gains reverse into losses, money managers accustomed to sneering at Treasury yields paying a pathetic 3% while assets were reaping 30% gains annually suddenly change priorities to earning any safe yield that comes with a guaranteed return of capital without any offsetting devaluation in the currency.

The one sovereign bond market that best meets these qualifications is the US Treasury market: liquid, transparent, valuation set by market force not state decrees, not pegged to any other currency, and predictable based on the diversity and adaptability of the US economy and the relative predictability of its legal and financial system.

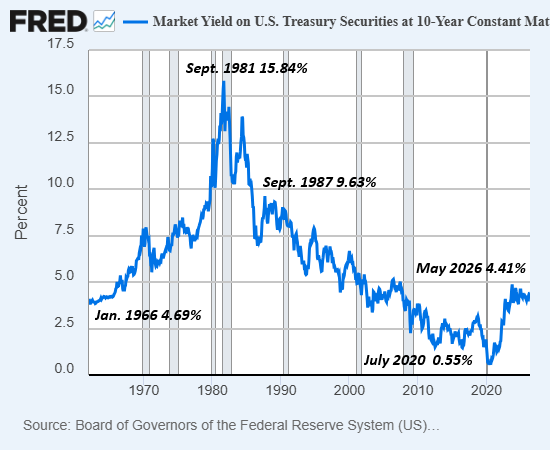

Rather than being sold, Treasuries will be sought after for their safety, predictability and yield. It's widely assumed that yields will drop toward zero in a recession, but this is recency bias not reality: in inflationary eras, yields rise even as capital exits the stock market. Consider this chart of the 10-year Treasury bond yield.

That's how US Treasuries play the Reverse card. While everyone's partying around the AI super-abundance punch bowl, the Monster Id is melting the last steel containment shield in the Denial Basement. Denial will turn to anger--this can't be happening--to bargaining--look, just make the market go back up once more so I can get out whole--to depression--it's gone, it's all gone--to acceptance. Oh well, time to start over.

There's a remarkable irony in this reversal: the profligate borrowing of the US Treasury looks unsustainable when Treasuries are being sold. But when asset bubbles pop and those reaping 30% gains annually have lost 30% of their entire capital, then even if a modest percentage of the hundreds of trillions left sloshing around the global economy seek the safety and predictable yield of Treasuries, that modest percentage will be more than enough to fund federal borrowing.

The total value of global assets cannot be measured with certainty, but estimates of liquid assets (cash and securities / cash equivalents) place the total around $450 trillion. US debt (the entire Treasuries market) is $31 trillion, about 7% of current global liquid assets.

This doesn't include real estate or fixed assets. (Please note estimates vary widely depending on what's being counted.)

All the Money in the World, And Who Has It (2022)

How Much Money Is in the World in 2026? Shocking Figures (Updated 2026-02-04)

Should the asset bubbles pop, total assets will fall significantly, but the sum of cash and cash equivalents will be extraordinarily large as fixed assets collapsing in value will be sold and converted to cash.

If 10% of all privately held wealth seeks the safety and yield of US Treasuries, that's a very large pool of capital trying to get a piece of a relatively limited asset class.

Some final points that must be made. Assets that looked safe as inflation hedges get sold because inflation in the cost of living doesn't necessarily translate to inflation of asset valuations. If demand craters, valuations fall. Once capital appreciation reverses to losses of capital, money managers will seek any safe yield and a return of capital over risking further downside.

Resources rise in value in global growth. But demand can drop far faster than supply, and so even limited resources can crash in price in a deep recession that crushes demand.

Individual investors can absorb losses in the hope that prices will soon return to nosebleed levels, but money managers don't have that luxury. The winning strategy in terms of saving their jobs is sell everything, put the capital in Treasuries earning some yield, and await the return of organic demand after the washout of all asset valuations reaches exhaustion.

Recency bias stretches back 17 years to 2009. Few believe a deflation of asset valuations is possible, or that yields could rise or that Treasuries will be in high demand while all the current darlings are being sold.

Money managers have a different risk calculus than individual investors / gamblers. And since they manage large sums, what they process through their OODA loop will influence markets. So it usually pays to put ourselves in their shoes. Losing our own money is one thing, losing other people's money is another.

My book Investing In Revolution is available at a 10% discount ($18 for the paperback, $24 for the hardcover and $8.95 for the ebook edition).

Introduction (free)

Become

a $3/month patron of my work via patreon.com

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Harvey D. ($200), for your beyond-outrageously generous subscription to this site -- I am greatly honored by your steadfast support and readership. |

Thank you, Irving W. ($70), for your wondrously generous subscription to this site -- I am greatly honored by your support and readership. |

|

|

Thank you, Melissa S. ($7/month) for your splendidly generous subscription to this site -- I am greatly honored by your support and readership. |

Thank you, Paulsat ($70) for your enormously generous subscription to this site -- I am greatly honored by your support and readership. |