Two Ways to Fix Generational Wealth Inequality

One way or another, some significant percentage of the wealth of the nation will have to start supporting children and young families if this nation is going to have a future worth saving.

When I address knotty issues such as generational wealth inequality, I am naturally asked: "what do you propose as a solution?" As I concluded in my recent post

Go Ahead and Rage at Boomers, But the Problem Is the Entire Economic Order (8/1/25):

It doesn't have to be this way, but we're going to have to change our values and the fundamental structures of our economy if we want a different outcome.

So let's dig in, starting with an analogy.

We go to the dentist or oral surgeon, and the diagnosis is not good. Our gums have receded, our teeth are getting loose and if we don't undergo painful, costly surgery, we're going to start losing teeth. If we do nothing, fixing the future problems will be even more painful and costly than acting now.

But then someone else says all that is "doom and gloom," we're fine, everything will sort itself out without any pain or cost. This is what we want to hear, of course, but it's not reality-based; the realistic assessment is our teeth will fall out if we do nothing, and then our problems will be much worse. It's not going to sort itself out if we do nothing.

In the realm of economics and finance, there are veritable armies of apologists and PR flacks whose job (self-appointed or paid) is to reassure us everything is fine and it will all sort itself out without any pain, sacrifice or cost.

In summary: the Fed, AI, crypto, fusion, etc. Some form of financial engineering or techno-wizardry will make all our problems go away without any pain, sacrifice or cost.

The apologists and PR flacks paint a very pretty picture, but back in the real world, none of these supposed fixes will fix the generational wealth divide. There are two oft-proposed "it will all sort itself out without any of us having to do anything" pseudo-solutions:

1. As the economy grows, the younger generations will get wealthier as wages rise. That sounds good, but the economy has been growing smartly for many years and this has basically done nothing to close the generational wealth gap, so this is fantasy, not reality.

2. As Boomers pass on, their immense wealth will pass on to their offspring. Once again, this sounds nice but it's not realistic. One issue is the majority of this wealth is an artifact of unsustainable asset bubbles, i.e. phantom-wealth that will disappear when the bubbles pop.

The second issue is the cost of care is now so high that even $1 million can be consumed down to the last morsel. As I noted in

The Stoicism of the Caregiver (3/5/25):

The financial costs of care are staggering. A bed in private assisted living is around $75,000 and up a year, a private room in a nursing home is around $150,000 a year, and round-the-clock care at home costs from $150,000 to $250,000+ annually.

The Crushing Financial Burden of Aging at Home (WSJ.com, paywalled)

"Christine Salhany spends about $240,000 a year for 24-hour in-home care for her husband who has Alzheimer's. In Illinois, Carolyn Brugioni's dad exhausted his savings and took out a home-equity line-of-credit to pay for home healthcare."

More than 11,000 people in the U.S. are turning 65 every day and the vast majority--77% of Americans age 50 and older according to an AARP survey--want to live as long as possible in their current home. At some point, many will need help. About one-fourth of those 65 and older will eventually require significant support and services for more than three years, according to the Center for Retirement Research at Boston College.

About one-third of retirees don't have resources to afford even a year of minimal care, according to the Boston College center.

"The new inheritance is not having enough money to give to kids but to have enough money to cover long-term care costs, says Liz O'Donnell, the Boston-based founder of Working Daughter, an online community of caregivers.

The costs of home care are so high that not just inheritances are exhausted; the home equity is also drained. $350,000 sounds like a lot of money but that might cover two years in a nursing home but not be enough to cover two years of round-the-clock care at home.

The cost of maintaining the home doesn't go away: property taxes, insurance and maintenance expenses must be paid, too.

In other words, the idea that the retired generation will leave ample inheritances is increasingly detached from reality. As noted, the new inheritance is to get through the years of caregiving without acquiring debt.

63 million adults are moonlighting as caregivers, with little support.

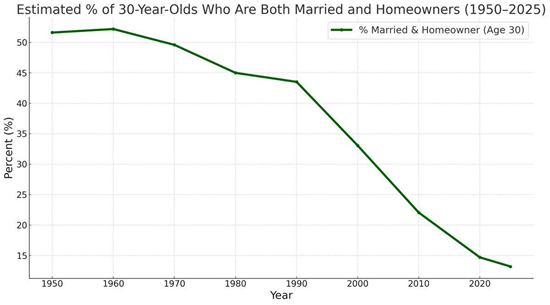

So where does that leave us? Let's start with an eye-opening chart depicting the percentage of young people who are both married and homeowners:

Shocking Chart Exposes America's "Civilizational Crisis". Note that the rate has fallen from 45% to 15% in the 35 years during which the economy became increasingly dependent on credit-asset bubbles for its "growth."

The well-paid apologists are already poring over statistics to "explain this away" and we can imagine the "explanations" that will be offered: young people simply don't want to get married and own a home. Um, OK, and so they also prefer financial precarity and nihilism, too, right?

I think there's far more truth in film director Celine Song's quote than in anything the apologists and PR hacks come up with. The quote is from

'Everybody's starved of affection' (The Guardian, paywalled):

"I think it has so much to do with how deeply broken our economic systems are, especially in the US. As we have learned, the American dream is not achievable. You cannot jump your class. But what's one of the few ways that you can still jump your class? Well, marriage."

In other words, stripped of plastic platitudes, the only way out is to marry way above mere middle class. The above chart reveals the low success rate of this "Cinderella" strategy. There simply aren't enough top 10% people who haven't already married another top 10% person left to meet the "Cinderella" demand.

OK, so now we're finally down to the painful, costly options, where the urge to attack the messenger becomes overwhelming. Look, I'm not saying I'm a fan of these options, I'm saying my job is to offer a realistic appraisal, and everyone can take that any way they want.

There are only two realistic ways to close the generational wealth inequality gap:

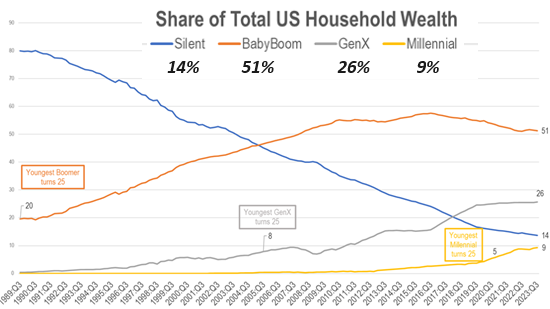

1. The Everything Bubble pops and wipes out 2/3 of the phantom wealth, the vast majority of which is held by the top 10% and the older generations (Boomers and the older cohort of Gen X). The gap is closed not by the younger generations getting wealthier but by the older generations getting poorer.

History suggests this is a very common way of closing the gap: all bubbles pop, and those who never owned the assets that bubbled up have nothing to lose. The wealthy lose most of their wealth, and that narrows the gap.

2. The younger Gen-Xers, Millennials and Gen Z start voting in high enough percentages to wrest political power from the older generations, and the younger political leaders who replace the old leaders come up with a much different policy-tax mix that addresses generational wealth inequality directly.

One way or another, some significant percentage of the wealth of the nation will have to start supporting children and young families if this nation is going to have a future worth saving.

How this plays out is anyone's guess. One thing I've learned the hard way as a business owner and self-employed precariat is: "liking" or "not liking" has nothing to do with it. We either get the painful, costly work done now or the problems quickly get beyond being fixable at any cost.

I laid out my own views two decades ago:

Boomers, Prepare to Fall on Your Swords (June 2005)

Check out my new book Ultra-Processed Life and my updated Books and Films.

Become

a $3/month patron of my work via patreon.com

Subscribe to my Substack for free

My recent books:

Disclosure: As an Amazon Associate I earn from qualifying purchases originated via links to Amazon products on this site.

Ultra-Processed Life print $16, (Kindle $7.95, Hardcover $20 (129 pages, 2025) audiobook Read the Introduction and first chapter for free (PDF)

The Mythology of Progress, Anti-Progress and a Mythology for the 21st Century print $16, (Kindle $6.95, audiobook, Hardcover $24 (215 pages, 2024) Read the Introduction and first chapter for free (PDF)

Self-Reliance in the 21st Century print $15, (Kindle $6.95, audiobook $13.08 (96 pages, 2022) Read the first chapter for free (PDF)

When You Can't Go On: Burnout, Reckoning and Renewal $15 print, $6.95 Kindle ebook; audiobook Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States (Kindle $6.95, print $16, audiobook) Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet (Kindle $6.95, print $15, audiobook $17.46) Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $3.95, print $12, audiobook) Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel) $3.95 Kindle, $12 print); read the first chapters for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print) Read the first section for free

Become a $3/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Janet D. ($3/month), for your exceedingly generous subscription to this site -- I am greatly honored by your support and readership. |

Thank you, Shawn ($7/month), for your marvelously generous subscription to this site -- I am greatly honored by your support and readership. |

|

|

Thank you, Randy G. ($70), for your superbly generous subscription to this site -- I am greatly honored by your support and readership. |

Thank you, Frans L. ($70), for your splendidly generous subscription to this site -- I am greatly honored by your support and readership. |