Feedback Loop of Recession: Housing Bust, Debt and Layoffs

Astute reader Trey S. recently posed an important question which is of pressing concern to all of us:

"Not sure if you have an insights, but I've been trying to look at non-bubble markets like Raleigh, North Carolina to see if the housing crash will hit all of America or just bubble markets. In November, home sales in downtown Raleigh - a prime gentrifying neighborhood - just stopped. I mean they hit a wall. I've been waiting for spring to see if it's a seasonal slow down or if the bubble effect is spreading.

My dad owns a construction company in Charlotte, another area that is 'strong,' but he says construction activity has halted. On a typical day, his phone would ring 80-100 times; yesterday it rang twice. This seems counter to what analysts describe happening in North Carolina.

In my mind this is the big question: If housing problems are truly contained to bubble cities, we'll be all right as a nation. But if Austin and Raleigh crash then we really are headed to the Great Depression, part II."

Excellent question, Trey. Thank you for your report. In my view the answer becomes clear if we view the housing crash as simply part of a larger nationwide debt orgy which is skidding to a halt. Simply put: when consumers can't/won't borrow trillions and spend the borrowed funds, then the economy contracts.

This is what was once considered a healthy, normal business cycle: expansion of credit leads to an exhaustion of creditworthiness which leads to a contraction of credit and spending which leads to consumers and businesses saving, which then builds the savings needed to fund the next credit expansion.

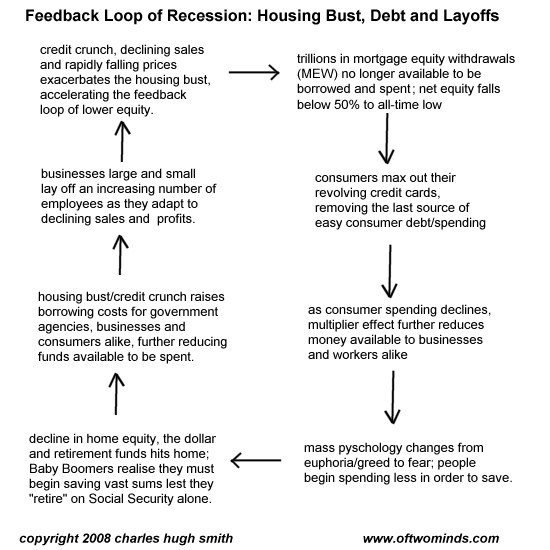

Since the Fed stopped the cycle in 2001-2003 by dropping rates to essentially zero, then the U.S. has not had a healthy business-cycle contraction since a brief recession in 1991. Now that credit has been so thoroughly abused, the contraction will feed on itself, as suggested by the following diagram.

The most important driver of easy-to-access and easy-to-spend cash has been the home. As these quotes reveal, home equity extraction has totalled trillions of dollars in the housing bubble: a staggering $863 billion was withdrawn in a mere three months at the top of the mania in 2005.

I have been unable to locate any reliable statistics on whether the vast majority of this was extracted in bubble-mad cities, but it seems the entire nation indulged in massive equity withdrawal.

As recently as the first quarter of 2007, American homeowners pulled out $450 billion from their homes and presumably blew most of it (there really is no way to know, but borrowers' claims to have "invested" 40% of the proceeds are suspect, to say the least.)

In the most recent quarter (Q4 2007), borrowing fell dramatically to $145 billion for the three month period. In other words: the home ATM is running out of cash.

Home-Equity Extraction Eases: (from June 2007)

In the first quarter, "home equity extraction: net of fees fell 8% to $449.6 billion at a seasonally adjusted annual rate from the fourth quarter, the lowest since the fourth quarter of 2003 well below the peak of $863.7 billion in the third quarter of 2005. The data are prepared by Fed economist James Kennedy according to a model he built with Mr. Greenspan; they aren’t from an official Fed publication.

From the Calculated Risk Blog of January 31, 2008:

Based on the Q4 GDP data from the BEA, my advance estimate for Mortgage Equity Withdrawal (MEW) is approximately $145 Billion for Q4 (just under $600 billion on a SAAR- seasonally adjusted annual rate) or 5.6% of Disposable Personal Income (DPI).

Given this massive extraction of equity, it is not surprising that U.S. homeowner equity has fallen to an all-time post-world War II low:

Homeowner equity falls below 50%. What's really sobering is that almost 40% of all residential units in the U.S. are not mortgaged, i.e. are "feee and clear." If we subtract this equity, then the remaining 60% of houses and condos obviously retain far less than 50% equity. (Statistical links can be found in Can 4% of Homeowners Sink the Entire Market? (February 21, 2007)

And as we all know, the debt orgy was not limited to housing. Frequent contributor Harun I. sent in this link on the stunning rise of credit card debt-- over $2 trillion last year alone:

When credit cards put you in jeopardy

Consumers have racked up more than $2.2 trillion in purchases and cash advances on major credit cards in just the last year. And it's become a habit for them to spend more than they have. The overall credit card debt grew by 315 percent from 1989 to 2006, according to public policy research firm Demos.

To compound the problem, fewer people are paying their credit cards bills on time. The percentage of people delinquent on their credit cards is the highest it's been in three years, according to CardTrack.com.

Harun also sent in this link to a Jim Juback video suggesting that the housing bust is by default also a retirement bust:

Jim Juback on The retirement crisis (MSN Money video)

We all know the housing bust has created an economic slowdown, a home-building depression and a credit crunch. But no one is talking about the retirement crisis, says MSN Money’s Jim Jubak -- even though soon-to-retire boomers have just lost a whopping $2 trillion in home equity.

Additionally, as Harun noted in a recent email, the Pareto Principle won't go away:

"According to Paulson only 2% of borrowers are in trouble (therefore everything should be okay). Then why all the turmoil? Why all the bailout talk? Why is Bernanke in a panic?

The only answer that makes sense but everyone is overlooking is, leverage. Mortgages are the underpinning of hundreds of trillions in derivatives. A small percentage of defaults is enough to cause massive de-leveraging.

If 2% is causing all this trouble, I hate to see what happens at 4% (64/4 rule)."

It seems the subprime mortgage default rate is already well in excess of 4%:

Default rate on U.S. subprime mortgages continues to rise:

As of August, default rates on adjustable-rate subprime mortgages written in 2007 had reached 8.05 percent, up from 5.77 percent in July, according to Youngblood's analysis of pools of home loans put together by Wall Street banks and sold to investors. By comparison, only 5.36 percent of adjustable-rate subprime loans made last year had defaulted by August 2006. Default rates on fixed-rate subprime mortgages were lower, but were rising at a similar pace.

The Pareto Principle has been covered a number of times here:

Can 4% of Homeowners Sink the Entire Market? (February 21, 2007)

The Great Fall: How Suburbs De-gentrify to Ghettos (November 20, 2007)

Frequent contributor U. Doran has observed that consumer credit troubles are now glaringly visible in rising auto repossession rates:

Entering the repossession lane: Default rate soars on auto loans in pattern likened to mortgage crisis.

Here is a New York Times story on the decline in consumer spending:

The Buck Has Stopped :

BEN S. BERNANKE, the Federal Reserve chairman, told Congress last week that fighting off a possible recession in the United States was Job 1 for his crew. But a consumer-led recession has already begun, according to a new index that reflects how much money Americans can actually spend right now.

The new indicator comes courtesy of Charles Biderman, the founder and chief executive of TrimTabs Investment Research, a proprietary research firm in Santa Rosa, Calif. “The big picture is: the amount of money people have to spend, which includes money on real estate transactions, is plummeting, and it started to break down in October,” he said."

People know the decade-long debt orgy was not healthy; witness this story, Hard Times Heighten Long-Felt Unease.

And in the "unintended but disasterous consequences" column, chalk up hapless governmental agencies completely unrelated to the housing bubble getting nailed for much higher borrowing costs:

Subprime woes affect toll agency: Toll Authority paying $1 million more a month.

So what happens when people stop eating out as often, stop buying carpeting and furniture in vast quanities, cut back on Starbucks lattes, and on and on? Sales slow, and businesses lay off employees. Those newly unemployed have a lot less money to spend, and so consumer spending erodes further in a feedback loop with no apparent end.

Apologists--even otherwise smart people--suggest that consumer spending might drop $300 billion or so--no big deal in a $14 trillion economy. I beg to differ.

First off, let's not forget the multiplier effect. Your $40 spent in a restaurant goes to the establishment's landlord, who spends some of that money, to food distributors, to employees, and so on, all of whom spend money which ends up in other workers' pockets. So the economy doesn't just "lose" your $40 when you don't spend it--everyone in the food chain down the line also loses a little. Cumulatively, that adds up to 3 times the initial amount spent/not spent.

Second, consider the enormous sums of mortgage equity and credit card debt which is no longer available to be borrowed/spent. We can debate the actual number which was borrowed and spent over the past few years, but let's just guesstimate it was $5 trillion. Considering that $863 billion was borrowed in only three months of 2005 (an annual rate of $3.4 trillion), and $2 trillion was added to revolving credit cards in just 2007, this number seems very conservative.

In other words, the actual amount would seem to approach $10 trillion based on the statistics given above:

MEW $3.4 trillion in 2005

MEW $2 trillion in 2006

MEW $600 billion in 2007

Credit card cash withdrawals and new unpaid balances: $4 trillion

We could also add in auto loans and other debt, but let's keep it rounded to trillions.

Wait a minute--$5 trillion is about 50% of annual consumer spending in the U.S. Take away $5 trillion of borrowing/spending over the next three years and you don't get $300 billion a year; with a modest 1.5 X multiplier, you get $5T X 1.5 = $7.5 T or a decline of $2.5 trillion a year--fully 18% of the entire U.S. economy.

Next thing you know, the same apologists will be hyping the wonderful "fact" that 85% of the populace "still have a job." Uh, isn't that a warm and fuzzy way of saying the unemployment rate is 15%--and climbing?

Readers Journal has been updated! As always, readers have shared incisive commentaries on key issues such as pharmaceutical ads and the demise of house flippers/speculators: There's also a new thought-provoking essay by contributor Chuck D. and a new short poem by Verona, My Second Self.

Special bonus update: Recommended Books/Films has been updated with dozens of new books and films. Scroll all the way to the right to see our exciting new film categories, "French Tough-Guy Films" and "Guy Films (no Merchant-Ivory!)". Great fun. If you think all French movies are romantic triangles or cuddly movies like "Amelie," prepare to be blown away.

NOTE: contributions are humbly acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, William S. ($15), for your sustaining, amazingly generous support of this humble site. I am greatly honored by your contributions and readership.

charles hugh smith

Investing In Revolution

Ultra-Processed Life

The Mythology of Progress

Self-Reliance in the 21st Century

Burnout: Reckoning and Renewal

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

A Hacker's Teleology

Will You Be Richer or Poorer?

Pathfinding our Destiny

The Consulting Philosopher

Money and Work Unchained

Inequality and the Collapse of Privilege

Why Our Status Quo Failed and Is Beyond Reform

A Radically Beneficial World

Get a Job, Build a Real Career and Defy a Bewildering Economy

The Nearly Free University

Resistance, Revolution, Liberation

Investing in troubled times

Survival +

Add Of Two Minds to your reader:

CHS

Weekly Musings Reports

Subscribers ($5/mo) receive weekly Musings Reports. At readers' request, there is also a $10/month subscription option.

What subscribers are saying about the Musings (read samples):

"What makes you a channel worth paying for? It's actually pretty simple - you possess a clarity of thought that most of us can only dream of, and a perspective that allows you to focus on the truth with laser-like precision." Jim S.

The "unsubscribe" link is for when you find the usual drivel here insufferable.

2005

2010

2015

2020

2025