Will Crushing Student Loans and Worthless College Degrees Politicize the Millennial Generation?

The existing social and financial order is crumbling because it is unsustainable on multiple levels. The central state is not the Millennials' friend, it is their oppressor.

No generation of young people is ever politicized by hunger in distant lands or issues of the elderly. It's no rap on youth that self-interest defines what issues have the potential to radically transform their political consciousness; the transformative cause must reveal the system is broken for them and that it intends on sacrificing their generation to uphold the Status Quo.

The Millennial generation, also known as Gen-Y (Gen-Y comes after Gen-X), is generally defined as those born between 1982 and 2004.

The oldest Millennials were children during the first Iraq War in 1991 (Desert Storm) and just coming of age in 2001 (9/11 and the war in Afghanistan) and the start of the second Iraq War (2003).

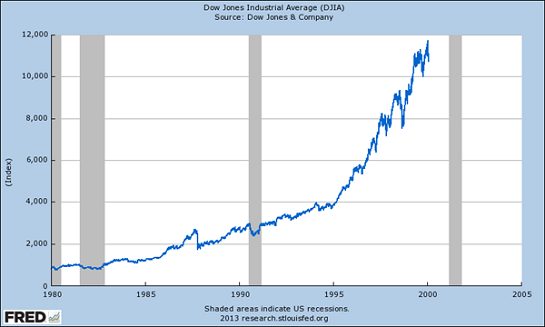

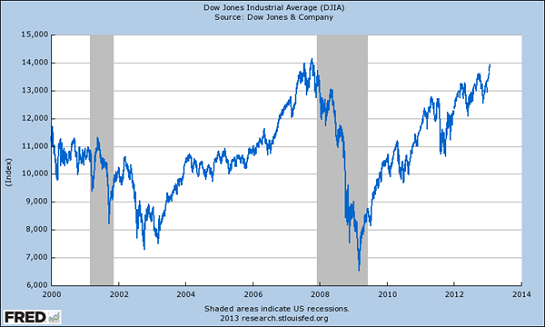

The Millennials have entered adulthood in a era characterized by permanent low-intensity wars and central-bank/state managed financial bubbles--2001 to the present. In other words, the only experience they have is of centralized state mismanagement on a global scale.

The gross incompetence of the government and central bank--not to mention the endless power grabs by these centralized authorities--has not yet aroused a political consciousness that the system is irrevocably broken, not just for older generations but most especially for them.

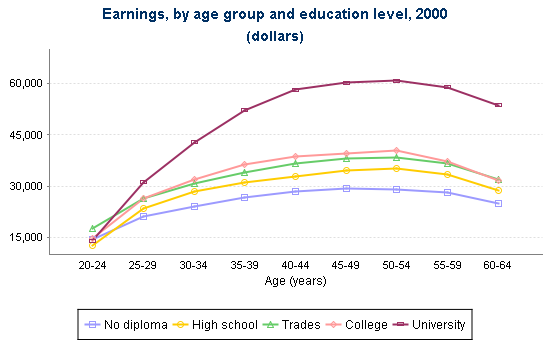

Anecdotally, it appears the Millennial generation is still operating on the fantasy that all they need to do to get a secure, good-paying job and a happy life is go to college and enter the Status Quo machine of government/corporate America.

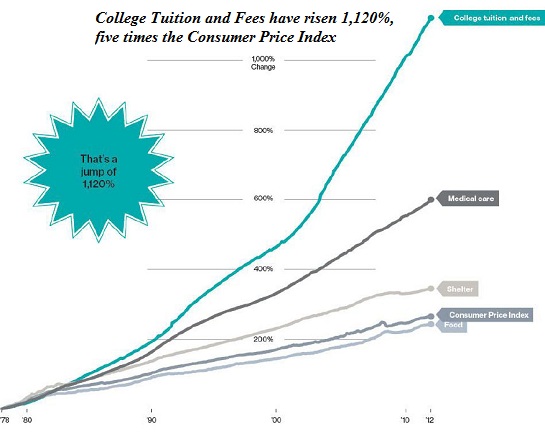

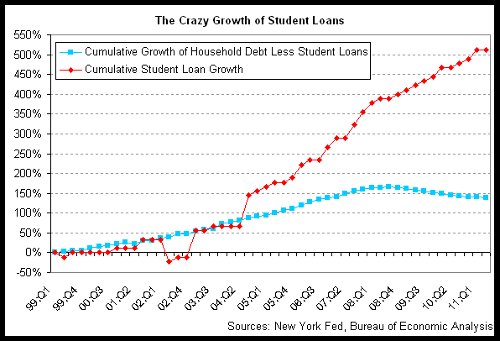

There are two fatal flaws in this fantasy: the $1+ trillion student loan industry and a transforming economy. The higher education industry in the U.S. operates as a central state-enabled and funded cartel, limiting supply while demand (based on the fantasy that a college degree has critical value) soars. This enables the cartel to keep raising prices even as the value of its product (a diploma) sinks to near-zero.

Since the Federal government issues and guarantees all student loans, the higher education cartel is (like sickcare, national defense and the mortgage industry) effectively socialized, i.e. funded and managed by the central state.

If you understand the student loan system is predatory, parasitic and exploitive, you have reached first base of a meaningful political awareness. If you understand the central state (Federal government) funds and enforces this system, you've reached second base. If you understand the vast majority of college degrees do little to prepare you to be productively employed in the real economy, you have reached third base.

If you understand the Status Quo is unsustainable and does not operate according the the fantasy model you've been told, congratulations, you're close to home base.

I have covered all the salient issues repeatedly:

The Fatal Disease of the Status Quo: Diminishing Returns (May 1, 2013)

College Grads: It's a Different Economy (May 3, 2013)

Bernanke's Neofeudal Rentier Economy (May 7, 2013)

Degrowth and Anti-Consumerism (May 9, 2013)

Centralization and Sociopathology (May 21, 2013)

Present Shock and the Loss of History and Context (May 22, 2013)

Generation X: An Inconvenient Era (guest post) (May 23, 2013)

The Nearly-Free University (November 15, 2012)

The central state is not your friend, it is your oppressor. The loan shark that won't let you discharge your student loan debt without appealing each ruling against you three times is the government (and its hired-gun proxies).

The oppressor who demands you work your entire life to pay interest on public debt squandered on neocolonial wars and various cartels (sickcare et al.) is your central state.

The entity who demands you pay higher taxes so the generation entering retirement gets all that it was promised, even though the world has changed and the promises are no longer sustainable? The central state.

The oppressor that will devote its enormous resources to investigate and crush you if you actively resist the bankers and financiers who pull the political lackeys' strings? The central state.

At some point, the Millennial generation will have to awaken to the fact that the only way to change its fate is to grasp political power and redirect the policy and mindset of the nation. Centralization is the black hole that is destroying the nation's social and economic vigor. Decentralization, transparency, accountability, adaptability, social innovation, a community-based economy--these are the key features of a sustainable social order.

The existing social and financial order is crumbling because it is unsustainable on multiple levels. The Status Quo will cling to its false promises and corrupt centers of power until the moment the whole thing implodes.

Related links of interest:

Dear Class of ‘13: You’ve been scammed How the College-Industrial Complex drove tuition so high

My Generation’s Disease

Podcast with Mike Swanson of WallStreetWindow.com on student loan debt and the Nearly Free University: Charles Hugh Smith On the Forces of Centralization and Soaring Education Costs. I always enjoy discussing issues with Mike, a polymath with a wide range of interests and experiences.

Podcast with Mike Swanson of WallStreetWindow.com on student loan debt and the Nearly Free University: Charles Hugh Smith On the Forces of Centralization and Soaring Education Costs. I always enjoy discussing issues with Mike, a polymath with a wide range of interests and experiences.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, John M. ($10/month), for your outrageously generous subscription to this site -- I am greatly honored by your support and readership. | Thank you, Joseph P. ($100), for your outrageously generous contribution to this site -- I am greatly honored by your support and readership. |

Read more...