The Rise and Fall of Great Powers

The very attempt to reform an unstable, diminishing-return system often precipitates its collapse.

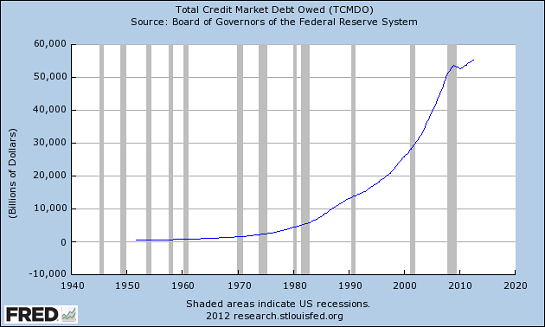

Our collective interest in the rise and fall of empires is not academic. The meteoric rise of China and the financialization rotting out global capitalism are just two developments that suggest we are entering an era where some great powers will collapse, others will remake themselves and others will gain ascendancy.

In How Empires Fall (April 17, 2013), I discussed Adrian Goldsworthy's How Rome Fell: Death of a Superpower and an old favorite on the same topic, Michael Grant's excellentThe Fall of the Roman Empire.

Paul Kennedy's influential book from 1987, The Rise and Fall of the Great Powers, seeks generalizations about what causes the rise and decline of great powers, be they empires or nation-states.

Kennedy avoids the temptation to extract grand theories from history, quietly mocking Wallersteins's "world systems" and related analyses. In this he follows fellow historian Fernand Braudel, who also hesitated to draw overarching theories from the messy history of capitalism.

Kennedy proposes one mechanism that he claims does hold true over time: it's not the absolute wealth and power of any one nation or empire that matters, it's the economic growth rate of competitors and its wealth and power relative to theirs that matter. A nation whose economic base is growing at a lower rate than a competitor slowly become relatively weaker than its rival, even though its absolute wealth is still increasing.

He also notes a tendency for powers in relative decline (i.e. those growing less robustly than their neighbors/rivals) to spend more on military security as their position in the pecking order weakens. This diversion of national surplus to military spending further saps their economic vitality as funds are shifted from investment to unproductive military spending. This creates a feedback loop as lower investment weakens their economic base which then causes the leadership to respond to this weakening power with more military spending.

This feedback creates lags, where an economically weakening power may actually increase its military power, until the overtaxed economy implodes under the weight of the high military spending.

This dynamic certainly seems visible in the history of the Soviet Union, which at the time of this book's publication in 1987 was unanimously considered an enduring superpower with a military that many believed could conquer Western Europe with its conventional forces.

This debate over the relative superiority of Soviet arms now seems quaint in the light of the collapse of the USSR a mere four years later, but it worth recalling that one of the most influential defense-doctrine books of the early 1980s was The The Third World War: August 1985 a novel by Sir John Hackett, about a fictional Soviet attack on Western Europe in 1985.

It was widely recognized by the late 1980s that the Soviets' relative power was in decline compared to the U.S., as the U.S. had worked its way through the malaise and restructuring of the 1970s and re-entered an era of strong economic and technological growth in the 1980s, rapidly outpacing the sclerotic Soviet economy.

It's also worth recalling the truly dismal status of the Soviet and Eastern Bloc economies compared to the Western economies: common inexpensive consumer items such as kitchen toasters were rare luxuries. In other words, while the Soviet economy was probably still expanding in the 1980s, the rate and quality of its expansion was considerably less than the growth of the West.

If one economy grows by 1% a year and another grows by 5% a year, in a mere decade the faster-growth economy will have expanded by more than 62%, while its slower-growing rival's economy grew only 10.5%.

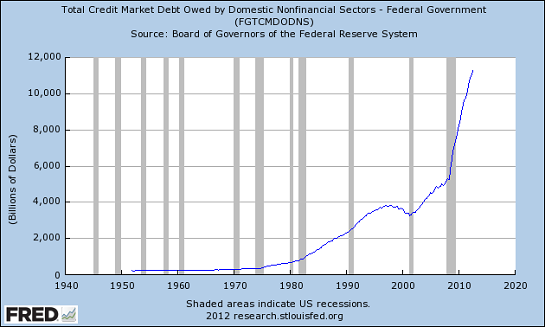

Many observers (especially on the Left, where suspicion of military spending is never far below the surface) see the U.S. as following this same path to decline and fall, as post-9/11 defense spending has skyrocketed while growth has stagnated. Despite what I see as wasteful spending on overlapping intelligence agencies and insanely costly programs like the F-35 fighter, U.S. defense spending remains around 5% of GDP (Pentagon/National Security budget is around $690 billion, GDP is around $15 trillion).

Though statistics from the Soviet era are not entirely reliable, various scholars have estimated that fully 40% of the Soviet GDP was being expended on its military and military-industrial complex.

During the height of the Reagan buildup, the U.S. was spending about 6% of its GDP on direct military expenditures. If you include the Security State (CIA, NSA, et al.), the Veterans Administration and other military-related programs (DARPA, etc.), the cost was still less than 10% of GDP.

How about America's position relative to other Great Powers or alliances? Interestingly, America's decline has been noted (and predicted) since the 1970s. Other nations such as Japan were growing much faster and were expected to overtake the U.S., based on the extrapolation of high growth rates into the future.

Once again the same predictions are being made, only this time it is China that is logging high annual growth rates that are being projected far into the future. The more things change, the more they remain the same.

Kennedy ends his book with a brief chapter looking ahead from 1987. He is careful not to make any outright predictions, but it is fair to say that he completely missed the bursting of Japan's miraculous high growth economy and the implosion of the Soviet Union a mere four years later in 1991. With the benefit of hindsight, we can discern the dynamics that led to these abrupt declines of relative power. But at the time, Japan's economy was universally regarded as superior to the U.S. economy and the USSR was widely viewed as a permanent superpower rival to the U.S.

How can we be so wrong about projecting present trends when we have so much data at our disposal? Why can't we identify the trends that end up mattering? Reading political-economic history books written a few decades ago reinforces our humility: we cannot predict the future, except to say that projecting present trends leads to false predictions.

Virtually no one in 1987 foresaw the limited Internet of the time exploding into a globally dominant technology, yet a mere decade later the web browser, cheaper memory, faster processors and broadband cable and DSL launched a digital revolution.

In 1987, pundits were predicting that Japan's "5th generation" computing would soon dominate what was left of America's technological edge. They were spectacularly wrong, as the 5th generation fizzled and Japan became an also-ran in web technology, a position it still holds despite its many global electronic corporations and vast university research system.

Japan's modern economy was set up in the late 1940s and early 1950s to exploit the world of that time. Sixty years later, Japan is still a wealthy nation, but its relative wealth and power have declined for 20 years, as its political-financial power structure clings to a model that worked splendidly for 40 years but has not worked effectively for 20 years.

The decline is not just the result of debt and political sclerosis; Japan's vaunted electronics industry has been superseded by rivals in the U.S. and Korea. It is astonishing that there are virtually no Japanese brand smart phones with global sales, and only marginal Japanese-brand sales in the PC/notebook/tablet markets.

The key dynamic here is once the low-hanging fruit have all been plucked, it becomes much more difficult to achieve high growth rates. That cycle is speeding up, it seems; western nations took 100 years to rapidly industrialize and then slip into failed models of stagnation; Japan took only 40 years to cycle through to stagnation, and now China has picked the low-hanging fruit and reverted to financialization, diminishing returns and rapidly rising debt after a mere 30 years of rapid growth.

There is certainly evidence that China's leadership knows deep reform is necessary but the incentives to take that risk are low. Perhaps that is a key dynamic in this cycle of rapid growth leading to stagnation: the leadership, like everyone else, cannot quite believe the model no longer works. There are huge risks to reform, while staying the course seems to offer the hope of a renewal of past growth rates. But alas, the low hanging fruit have all been picked long ago, and as a result the leadership pursues the apparently lower-risk strategy that I call "doing more of what has failed spectacularly."

Though none of the historians listed above mention it, there is another dangerous dynamic in any systemic reform: the very attempt to reform an unstable, diminishing-return system often precipitates its collapse. The leadership recognizes the need for systemic reform, but changing anything causes the house of cards to collapse in a heap. This seems to describe the endgame in the USSR, where Gorbachev's relatively modest reforms unraveled the entire empire.

Director Michael Apted has been filming a remarkable series of documentaries following the lives of 14 English people since the age of 7: The Up Series (Wikipedia) is a series of documentary films produced by Granada Television that have followed the lives of fourteen British children since 1964.(The titles: 7 Up, 14 Up, and so on, the latest being 56 Up.) The Up Series, eight films (Seven Up - 56 Up)

We expect those children with few advantages in life (i.e. lower-class) to do less well than those with many advantages, and this linear expectation is fulfilled in some cases. (This is the expectation of the working-class children themselves.)

But in most cases, the individuals' lives are entirely non-linear: some decades they do less well, in others they do much better, and the dynamics that arise and dominate each stretch of their lives are not very predictable.

This series reinforces our humility about predicting the life paths of individuals.

So is there a unifying theme here? I would say yes, and it is embodied in this quote from Charles Darwin, co-founder of our understanding of natural selection and evolution: "It is not the strongest of the species that survives, nor the most intelligent, but the ones most adaptable to change."

This essay is excerpted from Musings Report 16. The Musings Reports are basically a glimpse into my notebook, the unfiltered swamp where I organize future themes, sort through the dozens of stories and links submitted by readers, refine my own research and start connecting dots which appear later in the blog or in my books.

This essay is excerpted from Musings Report 16. The Musings Reports are basically a glimpse into my notebook, the unfiltered swamp where I organize future themes, sort through the dozens of stories and links submitted by readers, refine my own research and start connecting dots which appear later in the blog or in my books.

The Musings Report includes an essay and three other sections: Market Musings, on the financial markets and trading, The Best Thing That Happened This Week and From Left Field.

If you'd like to receive the weekly Musings Reports, please subscribe ($5/month) via the links in the right sidebar or send $50 (the annual one-payment subscription fee) via the PayPal link.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, Chris in Marin ($100), for your outrageously generous contribution to this site -- please email me if you would like to receive the Musings Reports. | Thank you, Andrew F. ($50), for your spendidly generous contribution to this site -- I am greatly honored by your support and readership. |

Read more...