Everything Created Digitally Is Nearly Free--Including Money

It is immeasurably easier to digitally create claims on real-world assets than it is to create real-world assets.

We all understand that the cost of everything that can be created digitally is near-zero.This is why music, videos, text-based knowledge and telephone calls (Skype) are now basically free.

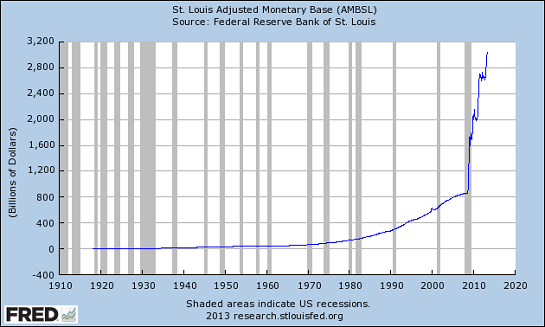

Since money is now created digitally, it too is basically free. We can see how easy it is to digitally create trillions of dollars in this chart of the U.S. monetary base. Roughly $1.2 trillion was created out of thin air essentially overnight back in the good old days of global financial meltdown:

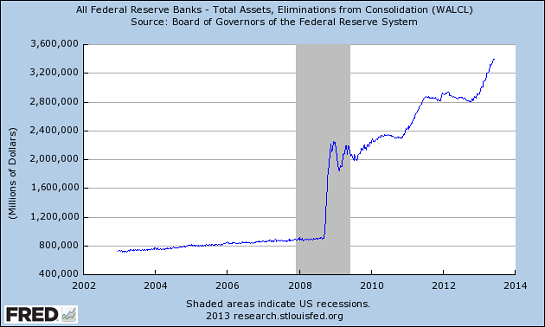

For another look at the wonders of the digital credit creation machine (a.k.a. digital printing press), here are the assets of the Federal Reserve banks: there's the $1.2+ trillion again--hum, Baby! Hit me with another trillion....

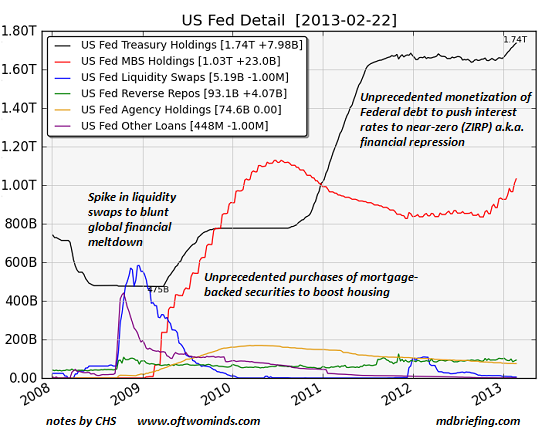

Here's a detailed look at the assets the Fed bought with its digitally created money--mostly Treasury bonds and real estate mortgages:

The key feature of digitally creating credit/money is this: it is immeasurably easier to digitally create claims on real-world assets than it is to create real-world assets.

This is why the digital creation of trillions of dollars in credit/money is distorting and disrupting the real economy of real-world assets: the claims on those assets keep expanding while the actual assets remain stubbornly tied to the real world.

This widening disconnect between rapidly multiplying digitally created claims on real assets and the actual assets has spawned a multitude of pernicious consequences, a few of which I have recently addressed:

How Cheap Credit Fuels Income/Wealth Inequality (May 30, 2013)

Why Serial Asset Bubbles Are Now The New Normal (June 6, 2013)

$179,000 Each--In Debt (June 5, 2013)

The Fleeting Beauty of Bubbles and Bonds (June 3, 2013)

Why Serial Asset Bubbles Are Now The New Normal (June 6, 2013)

$179,000 Each--In Debt (June 5, 2013)

The Fleeting Beauty of Bubbles and Bonds (June 3, 2013)

Since money can be created for free, how does it retain its value? The answer is artificial scarcity. The example of a college diploma is instructive.

Digitally created massively open online courses (MOOCs) have now made instruction as free as text-based knowledge. This means that offering a college-level series of courses is now nearly free--a topic I have discussed in some depth: The Nearly-Free University (November 15, 2012)

Recent studies have found that students who watch MOOCs learn more and test higher than students attending live lectures: Professors Are About to Get an Online Education Georgia Tech's new Internet master's degree in computer science is the future.

So how can colleges extract $100,000+ for something that is basically free? By monopolizing the issuance of diplomas. You can get the education for nearly free, but since the colleges own the right to print diplomas (for free), you have to pay them $100,000 for the piece of paper accrediting your free education.

This is a classic cartel structure: artificially limit the supply of what is in demand.

So how does the Fed artificially create scarcity-value for its freely created trillions of dollars? It restricts access to all that beautiful free money. Wouldn't it be nice if you and I could reach in and grab a couple of million bucks from the overflowing till?

Or almost as good, how about borrowing a couple million at nearly zero interest rates? At .5%, the annual interest payment on $2,000,000 is a measly $10,000.

Alas, access to the nearly free money is restricted to a small financial Elite, the Aristocracy in our neofeudal debtocracy. This tiny Elite can borrow the money for nearly nothing and then go out and buy real-world assets with the digitally created credit.

Debt-serfs have access to limited sums of this free money, but at much higher rates of interest: for example, student loans cost between 6% and 9%.

When debt-serf purchases of assets serve the agenda of the political/financial Elites, for example buying an auto or home, then the free money is doled out to secure the key feature of debt-serfdom--serfs must service all the debt they take on, thereby enriching the financial system that loaned them the money.

And where did the financial sector get the money? From the Federal Reserve.

How about just giving me $500,000 at .5% interest direct from the Federal Reserve, instead of a mortgage at 3.5%? Sorry, it doesn't work that way: the free money must be restricted to the financial Elite so it can profit mightily from its restricted access to all the free money.

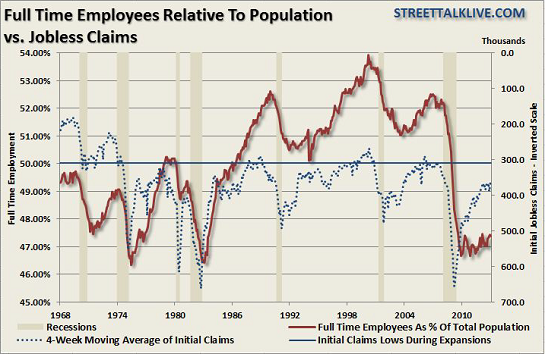

Creating nearly free money and restricting it to benefit a tiny Elite certainly enables debt-serfdom, but it doesn't do much for the real economy. Exhibit 1, fulltime employment:

The Fed can digitally print a trillion dollars at no cost, but that doesn't mean the money flows into the real economy.

Once again we are compelled to ask: cui bono, to whose benefit?

America No Longer Innovative Driven: This is one of the most important video programs I've done with Gordon Long, as we discuss our obsolete education system, the knowledge economy, risk-taking and the bread-and-circuses mindset that dominates our society:

America No Longer Innovative Driven: This is one of the most important video programs I've done with Gordon Long, as we discuss our obsolete education system, the knowledge economy, risk-taking and the bread-and-circuses mindset that dominates our society:

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, James K. ($50), for your astonishingly generous contribution to this site -- I am greatly honored by your support and readership. | Thank you, Daniel E. ($5), for your most generous contribution to this site -- I am greatly honored by your support and readership. |