Our Huge, Stinking Mountain of Debt: Student Loans

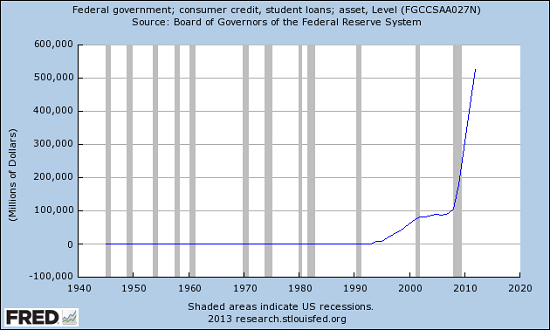

Imagine a huge, stinking mountain of debt, which represents all of the debt in the world... now look at this chart of student loan debt.

Notice anything about this chart of student loan debt owed to the Federal government? Direct Federal loans to students have exploded higher, from $93 billion in 2007 to $560 billion in early 2013. This gargantuan sum exceeds the gross domestic product (GDP) of entire nations—for example, Sweden ($538 billion) and Iran ($521 billion). Non-Federal student loans total another $500 billion, bringing the total to over $1 trillion.

Does this look remotely sustainable? Does it look remotely healthy for students, society, taxpayers now on the hook for a half-trillion dollars in potential defaults or the U.S. economy?

Frequent contributor Jeff W. explains the underlying dynamics of this wholesale shift of student-loan debt to Uncle Sam:

Why did Uncle Sam take over the student loan business? I don’t know for sure, of course. But I surmise that it has to do with the nature of debt money. As debt money is being created, it stimulates aggregate demand and circulates in the economy creating (false) prosperity. As long as the government and central banks can keep pumping new debt money into the economy, the economy runs well enough to keep the sheeple satisfied, e.g., housing bubble debt creation years, especially 1992-2006. The banks also profit enormously from the creation of trillions of dollars of new debt money.

Problems develop, however, when there are defaults. Note carefully that when a borrower defaults on a loan, the debt money he and the bank created continues to circulate. It is only when debts are paid back that the debt money disappears from circulation. Thus a condition of debt saturation or debt revulsion (where the people are sick of debt and want to pay off existing debt and refuse to take on more debt) is fatal to a debt money regime.

Central bankers carefully guard against deflation because it causes debt revulsion. If a borrower thinks that $1.00 that be borrows today will have to be paid back, after some years of deflation, with a dollar worth $1.10 or $1.20, the borrower will likely refuse to take out a loan. Debt revulsion causes problems for government (reduced tax revenues, unemployment), but even worse problems for the banks, for the same reason that auto revulsion causes problems for the auto industry or aluminum siding revulsion causes problems for the aluminum siding industry.

Defaults do not reduce the quantity of debt money in circulation, but they can and do bankrupt lenders. By doing so, they damage the debt issuing infrastructure. This is what happened in 1929. Not only were people refusing to take on new debt in the Depression, but the conveyor belt for issuing new debt was badly damaged by the failures of thousands of banks.

Thus defaults are not so bad if the debt-issuing infrastructure is not damaged by them. By Uncle Sam keeping the student loans on his books, and because Uncle Sam is backed by Infinite Fiat (i.e. the ability to create money in unlimited quantities via the Federal Reserve--editor), students can default on their loans without damaging any banks. Banks can still make fees from issuing loans and servicing loans, but they are protected from defaults. It is the best of all possible worlds!

Uncle Sam can also lie about the value of the student loans in his portfolio and thus make his balance sheet appear healthier than it really is and thereby help prop up his all-important fiat dollar. Win-win!

Finally in brief: 1) Student loan defaults are expected; 2) Politicians will be allowed to buy votes with selective student loan forgiveness; 3) Loaning money to people who are not expected to pay back their loans is the final frontier of debt money creation: if you can figure out how to protect the debt-issuing infrastructure, limitless new debt money can be created by loaning to the innumerable deadbeats who inhabit this world.

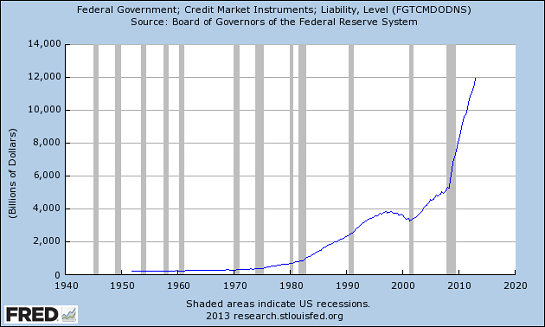

Sometimes I picture in my mind a huge, stinking mountain of debt, which represents all of the debt in the world. The debt mountain is usually growing, but because of defaults, fissures and sinkholes often appear; so even as it is expanding, parts of it are collapsing. Insiders know which parts of the mountain are safe and solid, but small investors are often plunged into one of the many bottomless pits that pockmark the surface of the rotten debt mountain.Thank you, Jeff, for an insightful overview of the state's role in pumping debt money into the economy and transferring risk to the taxpayers. When one pile of stinking debt becomes too risky for the bankers, this pile is transferred to the Federal government and the taxpayers. Haven't we seen this before? Hmm....are there any possible consequences of this huge, stinking pile of Federal debt expanding?

My new book The Nearly Free University and The Emerging Economy (Kindle eBook) is available at a 20% discount ($7.95, list $9.95) this week. Read the Foreword, first section and the Table of Contents.

The Nearly Free University and The Emerging Economy:

The Revolution in Higher Education

Reconnecting higher education, livelihoods and the economy

With the soaring cost of higher education, has the value a college degree been turned upside down? College tuition and fees are up 1000% since 1980. Half of all recent college graduates are jobless or underemployed, revealing a deep disconnect between higher education and the job market.

It is no surprise everyone is asking: Where is the return on investment? Is the assumption that higher education returns greater prosperity no longer true? And if this is the case, how does this impact you, your children and grandchildren?

We must thoroughly understand the twin revolutions now fundamentally changing our world: The true cost of higher education and an economy that seems to re-shape itself minute to minute.

The Nearly Free University and the Emerging Economy clearly describes the underlying dynamics at work - and, more importantly, lays out a new low-cost model for higher education: how digital technology is enabling a revolution in higher education that dramatically lowers costs while expanding the opportunities for students of all ages.

The Nearly Free University and the Emerging Economy provides clarity and optimism in a period of the greatest change our educational systems and society have seen, and offers everyone the tools needed to prosper in the Emerging Economy.

Read the Foreword, first section and the Table of Contents.

print edition (list $20, now $18)

Kindle edition: list $9.95, for one week only, $7.95 (20% discount)

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Once we accept responsibility, we become powerful.

Kindle: $9.95 print: $24

| Thank you, Wayne A. ($25), for yet another splendidly generous contribution to this site-- I am greatly honored by your steadfast support and readership. |