Rich Middle Class, Poor Middle Class

This great generational injustice is the direct consequence of central banks lowering interest rates to zero and inflating asset bubbles.

How can middle class households have similar incomes but some are asset-rich and others are asset-poor?

Spending and saving habits matter, of course; some households spend virtually all their net income while others "pay themselves first" and scrimp to do so.

But the really big differences in wealth are the result of what assets the household bought and when they were bought.

Those who bought assets at the top of bubbles may still be underwater once inflation is factored in; those who bought long before the Federal Reserve and other central banks inflated credit bubbles every few years have substantial equity even after the bubbles inevitably crash to Earth (revert to the mean).

For example, a household that bought $25,000 of 30-year Treasury bonds paying 12% in the early 1980s and reinvested the $3,000 annual interest (at much lower yields) ended up with over $100,000 by 2012.

Those who bought Apple stock shortly after Steve Jobs took the reins in 1997 did even better.

But few of us are blessed with the insight and courage to make big bets at just the right moment, and hold the bets for decades. Most of us buy homes when we scrape up the down payment, or upon getting married, having children, moving to a new locale, etc. Few of us have the years or willingness to attempt to time long real estate cycles.

Few of us acquire substantial amounts of stock in a corporation unless we work for the company and are granted stock options.

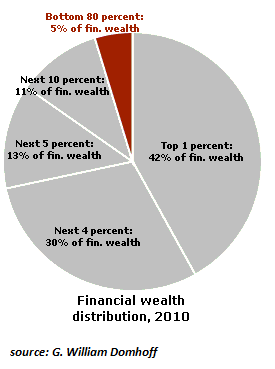

Thus it is no surprise that relatively few households below the top 5% hold substantial financial assets such as stocks and bonds.

Stagnating wages for the lower 90% haven't made it any easier to save up capital to invest. As noted yesterday in Neofeudalism 101: Strip-Mining the Upper Middle Class, most of the income gains of the past 40 years have flowed to the very top of the income pyramid.

For all these reasons, the family home remains the foundation of most middle class households' wealth. Unfortunately, the Federal Reserve's policies have generated one credit bubble after another, destroying the old paradigm that buying a house was a reliable way to build equity.

As we can see in the chart of the Case-Shiller Index for the nation and the San Francisco Bay Area, those who bought in the bubble years have little to no equity despite their large monthly mortgage payments.

Buying a house in the bubble years was an unmitigated disaster in terms of building wealth. Only those who bought in the pre-bubble years of 1987 to 1998 built substantial equity--equity that didn't vanish even when the bubble popped.

Many households that bought modest homes in the early 1970s and held onto them now have $1 million+ in equity if they happened to live in highly desirable locales such as San Francisco, West Los Angeles, Honolulu, pricey boroughs in New York City, etc.

These households were not any different that the other 60% of households that owned homes. Their great fortune (pun intended) resulted from two unexpected bits of luck: buying before asset bubbles inflated, and buying property in areas that became extremely desirable to buyers on a global scale.

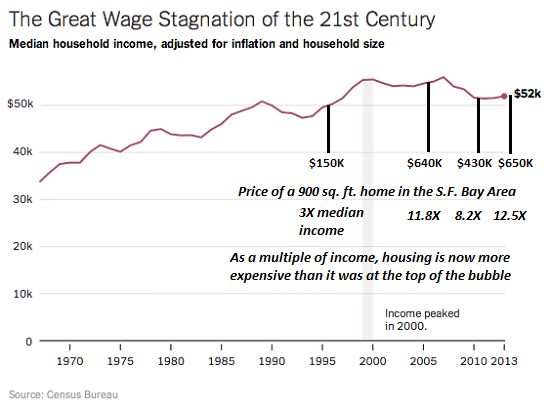

Based on multiples of inflation-adjusted income, housing in highly desirable areas is now more expensive than it was at the top of the 2007 bubble. Viewed from the metric of multiples of annual median income, housing in the San Francisco Bay Area has been unaffordable to all but very high-income households for the past 17 years.

Where does this leave us? With the unsettling reality that the generations that reached home-buying status in the 25-year era of 1973 - 1998 and happened to buy homes in locales that would one day become extremely desirable (and who didn't extract all their equity in the bubble years) are now Rich Middle Class Households.

Those who bought homes in the bubble years are Poor Middle Class Households with little or no asset wealth.

Is this just or fair? Of course not. This great generational injustice is the direct consequence of central banks lowering interest rates to zero and inflating asset bubbles in a corrosive (and vain) attempt to generate a wealth effect of households borrowing and blowing their newly created asset wealth.

In an economy that isn't whipsawed by central bank manipulation, the difference between middle class households' asset wealth is largely behavioral, not the random luck of coming of age before central banks began blowing destructive asset bubbles as a matter of policy.

Get a Job, Build a Real Career and Defy a Bewildering Economy(Kindle, $9.95)(print, $20)

Are you like me? Ever since my first summer job decades ago, I've been chasing financial security. Not win-the-lottery, Bill Gates riches (although it would be nice!), but simply a feeling of financial control. I want my financial worries to if not disappear at least be manageable and comprehensible.And like most of you, the way I've moved toward my goal has always hinged not just on having a job but a career.

You don't have to be a financial blogger to know that "having a job" and "having a career" do not mean the same thing today as they did when I first started swinging a hammer for a paycheck.

Even the basic concept "getting a job" has changed so radically that jobs--getting and keeping them, and the perceived lack of them--is the number one financial topic among friends, family and for that matter, complete strangers.

So I sat down and wrote this book: Get a Job, Build a Real Career and Defy a Bewildering Economy.

It details everything I've verified about employment and the economy, and lays out an action plan to get you employed.

I am proud of this book. It is the culmination of both my practical work experiences and my financial analysis, and it is a useful, practical, and clarifying read.

Test drive the first section and see for yourself. Kindle, $9.95 print, $20

"I want to thank you for creating your book Get a Job, Build a Real Career and Defy a Bewildering Economy. It is rare to find a person with a mind like yours, who can take a holistic systems view of things without being captured by specific perspectives or agendas. Your contribution to humanity is much appreciated."

Laura Y.Gordon Long and I discuss The New Nature of Work: Jobs, Occupations & Careers(25 minutes, YouTube)

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Get a Job, Build a Real Career and Defy a Bewildering Economy(Kindle, $9.95)(print, $20)

Are you like me? Ever since my first summer job decades ago, I've been chasing financial security. Not win-the-lottery, Bill Gates riches (although it would be nice!), but simply a feeling of financial control. I want my financial worries to if not disappear at least be manageable and comprehensible.And like most of you, the way I've moved toward my goal has always hinged not just on having a job but a career.

You don't have to be a financial blogger to know that "having a job" and "having a career" do not mean the same thing today as they did when I first started swinging a hammer for a paycheck.

Even the basic concept "getting a job" has changed so radically that jobs--getting and keeping them, and the perceived lack of them--is the number one financial topic among friends, family and for that matter, complete strangers.

So I sat down and wrote this book: Get a Job, Build a Real Career and Defy a Bewildering Economy.

It details everything I've verified about employment and the economy, and lays out an action plan to get you employed.

I am proud of this book. It is the culmination of both my practical work experiences and my financial analysis, and it is a useful, practical, and clarifying read.

Test drive the first section and see for yourself. Kindle, $9.95 print, $20

"I want to thank you for creating your book Get a Job, Build a Real Career and Defy a Bewildering Economy. It is rare to find a person with a mind like yours, who can take a holistic systems view of things without being captured by specific perspectives or agendas. Your contribution to humanity is much appreciated."

Laura Y.Gordon Long and I discuss The New Nature of Work: Jobs, Occupations & Careers(25 minutes, YouTube)

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

| Thank you, Jan K. ($150), for your beyond-outrageously generous subscription to this site-- I am greatly honored by your steadfast support and readership. |