Bubbles, Inflation and Overcapacity

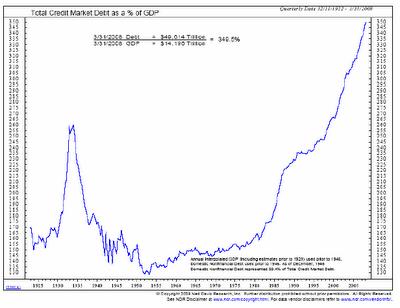

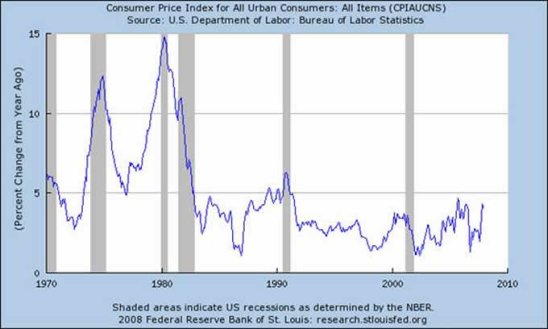

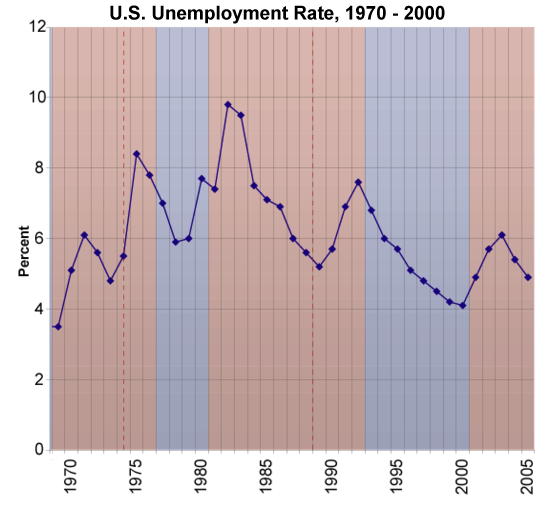

The global central banks have flooded the world economy with hot money for years. Why has this created massive asset bubbles rather than inflation? In the 1970s, expanding credit triggered a decade-long bout of high inflation as cheap money chased scarce goods. Why hasn't the massive expansion of credit/hot money of the past decade caused inflation? Short answer: overcapacity. Let's look at a few charts to recall the enormity of the current credit bubble: the trillions of dollars of credit created, the trillions borrowed in mortgages and other credit to chase asset prices upward, the trillions created as assets like housing rose in bubblicious euphoria, and the trillions extracted from those skyrocketing assets: Despite the trillions being created, borrowed and pumped into the economy, inflation remained benign: With all that money flowing around, jobs were relatively plentiful, setting a floor under consumption and consumer credit: Even as all this money chased goods, services and assets, interest rates fell, earning savers less and less return: Meanwhile, the capacity to make stuff like steel exploded: So here's the dynamic which enabled low interest rates and low inflation even as credit exploded and bubbles rose in one asset class after another. 1. Massive expansion of credit was paralleled by a massive expansion of industrial capacity in China and indeed the entire world. 2. This expansion of capacity was matched by an expansion of supply in commodities. As the industrialization of China (one of the so-called BRIC nations--China, Russia, India and Brazil) and other developing nations drove demand for commodities, the incentives to exploit new sources drove up supply of almost everything: oil, iron ore, coffee, etc. 3. While prices have fluctuated in an upward bias, at no time did the cost of commodities rise to levels which threatened global growth except for the oil spike in 2008. Adjusted for inflation, oil is well within historical boundaries even at $80/barrel. 4. To feed the giant credit-dependent machine they'd fostered, central banks kept lowering interest rates and increasing liquidity/money supply. This drove the returns on savings and bonds down to absurdly low levels, forcing money managers to chase riskier assets to make a decent return on investments. 5. This need to earn higher returns drove vast floods of money into assets, inflating one bubble after another. 6. Though consumption also skyrocketed, the vast expansion of industrial capacity and commodity supplies actually outpaced rising consumption, keeping supply and demand more or less in balance and prices relatively stable. In essence, the hot money was forced to chase assets for higher returns while China's capacity to make goods matched and then exceeded global demand for goods. The only way credit can drive inflation is if the supply of desired goods is limited. Many of us foresee a time when oil will be that commodity which is no longer able to match demand, but for now, the rise of production in Russia, Africa and elsewhere has kept pace with (now slackening) demand. Indeed, we might well see demand fall enough as the global recession takes hold that oil will fall to $30/barrel. China's capacity to produce goods now exceeds global demand. Add in the rest of the world's enormous overcapacity and you get deflation, not inflation.In one industry after another, massive overcapacity is the stark reality. For example, the world can manufacture twice as many vehicles as there are customers for those vehicles. The two key exceptions are grain and oil. If grain supply doesn't match demand, and reserves have been drawn down, then prices could rise suddenly. At some point oil supply will fall below demand, but when that point will occur is unknown. Until either or both grain and oil fall into scarcity, then inflation in goods and services has no foundation. As long as interest rates remain near-zero, then the pressure to borrow money and chase asset prices higher remains in force. No trend lasts forever. At some point interest rates will rise, risky assets will fall from favor and global scarcity in key resources will arise. How long can the central banks inflate the exponentially-expanding credit bubble? No one knows, but we can say the end-point will arrive when no one wants to borrow more money even at zero interest rates. Get Survival+: Structuring Prosperity for Yourself and the Nation on amazon.com or in ebook and Kindle formats. A 20% discount is available from the publisher. Expanded free eBook now available (85,300 words, 136 pages): iPod and iPhone owners: Read Survival+ on your iPod or iPhone by downloading the Kindle app and then buying the book from the Kindle store. Here's how. Thank you, Michael H. ($10), for your much-appreciated generous donation to this site. I am greatly honored by your support and readership.

Permanent link: Bubbles, Inflation and Overcapacity

Want more annoying analysis? Here it is!

in HTML: Survival+ in PDF: Survival+

Of Two Minds is now available via Kindle: Of Two Minds blog-Kindle