How Housing Affordability Can Falter Even as House Prices Decline

The assumption that lower home prices improves the affordability of houses ignores two critical inputs: interest rates and income.

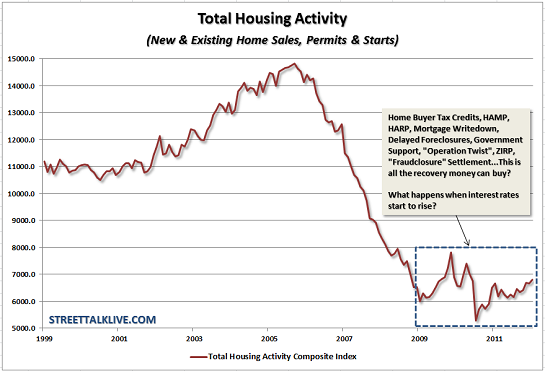

That the U.S. housing market is still in a post-bubble slump is no secret, as revealed by this chart courtesy of streettalklive.com: note that despite unprecedented intervention, including the complete socialization of the U.S. mortgage market (99% of all mortgages are guaranteed by the Federal government) and the socialization of subprime market for poor credit risks (3% down and easy credit from FHA), this chart punctures the happy-talk illusions of a rebound in housing.

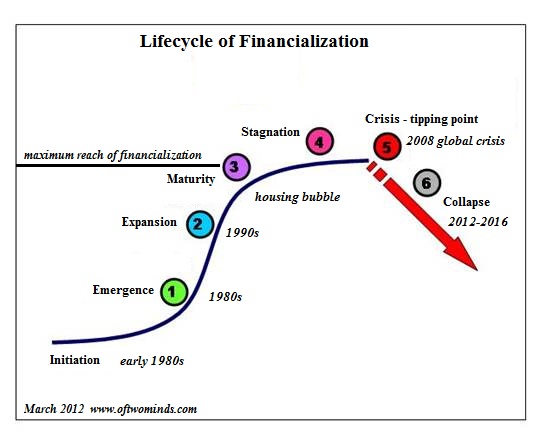

Credit-asset class bubbles cannot be reinflated because they follow an S-curve. No matter how much taxpayer money the Federal government throws into the housing market, it will not reinflate. The financialization (credit/leverage bubble) of housing follows an S-curve as a system, and tweaking the parameters of the inputs (lowering interest rates, buying up toxic mortgages, etc.) doesn't change the curve.

Hubris-soaked central Planners are incapable of understanding that their numerous policy interventions have essentially zero impact on the curve. But if you can't believe systems don't respond to frantic policy measures, then consider these factors:

1. Tens of millions of households are too poor to buy a home (the FDIC calculated 40% of the U.S. households have insufficient income and credit to buy a home) without massive subsidies, and with no skin in the game their purchase is basically a lease with an option to sell later for a private gain at the expense of the government.

if it doesn't work out then it's last one on, first one off: they default with little loss and possibly much to gain, i.e. two years living rent-free in a not-yet foreclosed house.

2. Tens of millions of other households are drowning in underwater mortgages they can afford to pay (barely) but that have crippled their net worth and borrowing power. They are out of the housing market except as potential defaulters.

3. Millions of other credit-worthy buyers have woken up to the fact that buying a house is a form of consumption and a risky "forced savings" investment, as property taxes spiral ever higher and prices continue sagging in many markets. The risk is high and the potential gain is uncertain.

Those snapping up housing for cash are either buying to rent the homes or to speculate that a resurgent housing market will arise and they can "flip" for big profits. This segment simply isn't large enough to soak up all the millions of homes languishing in the "shadow inventory" of homes being held off the market in the vain hope prices will bubble higher.

The general idea of lower home prices is that once prices fall to some magic threshold, buyers will jump in and liquidate the inventory. That notion makes two enormous assumptions:

--Interest rates will stay near-zero when inflation is factored in

--Household income will stop declining.

In other words, there are three inputs to housing affordability, and price is only one of them. Interest rates and disposable income are equally important. Note that income in all quintiles (the entire spectrum of income--high, middle and low) has been declining since the housing bubble topped in 2007:

Official inflation has been running at around 3% a year, and many other measures suggest that number grossly understates reality by gaming the percentages of various inputs.

But taking the official 3% as a reasonable approximation, then buyers of 4% 30-year mortgages are earning a wafer-thin 1% in real return (4% - 3% = 1%) and they are taking a stupendous risk that inflation will remain well under 4% for the next three decades. Any surge in inflation and rates would destroy much of the value of their investment.

Let's take two examples. Let's say a house that sold for $400,000 at the top of the bubble is now selling for $250,000, $50,000 down (20%) with a $200,000 mortgage at 4%. let's say the household earns $50,000, so the mortgage is exactly four times gross income. The interest on the mortgage is $8,000 annually (principal, property taxes, insurance etc. are added to make up the total mortgage payment).

Now let's say the house declines in price to $225,000, so the down payment drops to $45,000 and the mortgage is $180,000. But let's say investors are now demanding 3% above nominal inflation and mortgage rates are now at the historically moderate level of 6%. Meanwhile, the household income has slipped to $45,000 annually as bonuses and hours are trimmed and workers transition to lower paid positions.

The ratio of income to mortgage is still 4-to-1, but the annual interest payment is now $10,800, $2,800 higher--a 35% increase. By any measure, the house is less affordable despite declining $25,000 in price.

This is how affordability can decline even as home prices continue to slide.

SPECIAL OFFER TO OFTWOMINDS READERS: I don't subscribe to many investment services, but I do subscribe to Macrostory.com because I have found Tony's technical analysis insightfully correlates the credit, commodities, currency and stock markets. Of Two Minds readers are being offered a special 20% discount on any subscription toMacroStory.com through Monday March 26. Simply enter promo code OfTwoMinds at checkout.

SPECIAL OFFER TO OFTWOMINDS READERS: I don't subscribe to many investment services, but I do subscribe to Macrostory.com because I have found Tony's technical analysis insightfully correlates the credit, commodities, currency and stock markets. Of Two Minds readers are being offered a special 20% discount on any subscription toMacroStory.com through Monday March 26. Simply enter promo code OfTwoMinds at checkout.

Disclaimer: I receive no commission or payment from this offer. It is presented as a potential benefit to readers who are interested in technical analysis services.

| Thank you, Steve C. ($20), for your remarkably generous contribution to this site -- I am greatly honored by your support and readership. | Thank you, Mike R. (essay), for your insightful and moving essay on Vietnam-era vets and the nature of trauma -- I am greatly honored by your support and readership. |