Charting Insolvency: Social Security and Wages

We as a nation need to prioritize the Social Security retirement of those with no other pension incomes.

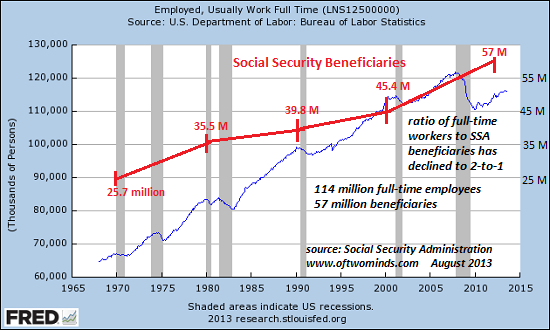

David P. of Market Daily Briefing kindly sent two charts illustrating the problem with Social Security. Yesterday I discussed The Trends Few Dare Discuss: Social Security and the Decline in Full-Time Employment (August 19, 2013); David's charts graphically demonstrate the untenable trend in the ratio of full-time employees (FTE) to Social Security beneficiaries:

The rapid decline in the ratio of workers to beneficiaries in the 1970s reflected both a stagflationary economy that was not conducive to job creation and an increase in SSA (Social Security Administration) beneficiaries of nearly 10 million in the decade.

The ratio recovered as the economy added nearly 30 million more full-time jobs from 1980 to 2000, and the number of beneficiaries added to Social Security rolls declined to roughly half the rate of the 1970s--roughly 5 million additional beneficiaries were added per decade between 1980 and 2000.

The freefall in the ratio since 2000 reflects an extraordinary number of new beneficiaries and a structural decline in full-time employment. These trends are not temporary; as the Baby Boom ages, the number of beneficiaries is set to rise from 57 million to 90 million.

Fantasy and denial aside, there is no evidence that the forces eroding full-time employment will magically vanish in the coming decades.

David's second chart displays the cost of Social Security benefits to private-sector wages. Government sector employees are typically covered by military/Federal pensions or state/agency pensions, and so the key metric here is private-sector wages.

The official projections of the SSA Trustees state future SSA costs as a percentage of GDP, but since GDP is constantly being gamed, that is an untrustworthy metric of the system's viability. Since Social Security is paid for by payroll taxes, the only metric that counts is payrolls.

As explained in yesterday's entry, SSA is designed to favor lower-income workers; those earning $10,000 a year or less (38 million workers) contribute relatively modest payroll taxes in comparison to the benefits they qualify for. (These numbers are drawn directly from Social Security Administration payroll data.)

The system's solvency is thus dependent on higher-income wage earners. If wages exposed to SSA payroll taxes don't expand at the same rate as the costs of benefits, the system is on a one-way trip to insolvency.

Let's say the Social Security system starts running large ($100+ billion) deficits. What does this mean? It simply means the U.S. Treasury needs to borrow more money by selling more Treasury bonds, and/or the Federal government has to cut spending on other programs to divert the $100+ billion annually to SSA.

Borrowing another $100 billion annually on top of the $1 trillion the Federal government has been borrowing annually is not a problem as long as the yields on Treasury debt is near-zero. But if interest rates rise (for whatever reason), the government's ability to borrow trillions of dollars is crimped as the cost of the interest on the rapidly rising debt starts chewing into the funding for programs.

As crazy as it sounds, eventually the government could be spending more on interest than on Social Security ($800 billion a year and rising fast). That would require the Treasury to borrow even more just to pay the skyrocketing interest.

That self-reinforcing debt/interest feedback loop has one and only one end state: implosion.

There are only two ways to fix "pay as you go" systems like Social Security: cut benefits and/or raise payroll taxes. Many people favor eliminating the limit on Social Security payroll taxes, currently $113,700 annually. Since less than 5% of wage earners make more than $113,700 annually, eliminating the limit would raise taxes on about 7.5 million workers and their employers (each pays 7.65% in SSA and Medicare payroll taxes).

Since the top slice of earners take home roughly 40% of total wages, eliminating the limit on SSA payroll taxes would raise a substantial sum. But since the top 10 percent of income earners paid 71 percent of all federal income taxes in 2009 though they earned 43 percent of all income, such a move to eliminate the income limit on SSA payroll taxes would encourage high earners and their employers to shift pay to non-payroll compensation such as stock options.

As a result, linear projections will likely fail to predict reality; the sums raised will likely be considerably less than projected, as many high-earners are small business owners and professionals who can change the mix of compensation (the same is true of global corporations, of course).

Another alternative is to raise the payroll tax and the income limit in a series of steps.

The second option is to change the social contract so that Social Security explicitly secures the retirement of lower-income workers rather than adding to the income of workers with substantial non-SSA pensions/income. Those collecting pensions from other sources would receive less Social Security. Those with no other pension income would receive 100% of their Social Security retirement benefit, while those collecting pensions from other sources would receive less on a sliding scale. Perhaps those with pension incomes above 3 times the median wage ($26,500 X 3 = $79,500 or $6,660/month) would receive no Social Security.

Do those collecting three times the median wage really need the same SSA benefits as those with no other retirement income?

The conventional answer is that any means testing of Social Security would destroy its political popularity, but in reality such means-testing would likely affect only the top (higher-income) 10% of the populace.

"We wuz promised" does not apply to "pay as you go" systems, which are extraordinarily exposed to current trends and realities. It's time for America to examine the social contract/Social Security in an era of declining full-time employment and widening income inequality. We as a nation need to prioritize the Social Security retirement income of those with no other pension incomes.

For more on this topic:

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, Hinze Chow Family ($100), for your outrageously generous contribution to this site-- I am greatly honored by your support and readership. |