The Grand Experiment Part 2: Unlimited State Creation of Credit and Cash

An unprecedented tsunami of state-borrowed and Fed-printed money has failed to fix the systemic crisis.

What happens when all systemic risk ends up concentrated in the central state? Let's start by noting that the central state (Federal government) backstops every category of risk: major flooding, crop failure, bank failure, student loans, old-age pensions, healthcare for the elderly and low-income, disability, and so on.

The Federal government pays for all these programs by collecting taxes and borrowing the difference between tax receipts and expenditures by selling Treasury bonds.

The foundational faith of this concentration of risk in the state is that crises that require massive deficit spending--borrowing vast sums to "get us through a rough patch"-- will be intermittent and brief.

The Great Depression upended that faith: certain types of systemic financial crises were neither intermittent nor brief but chronic and resistant to conventional fixes.

The unprecedented borrowing and spending of World War II spawned a new faith: that the only fix to chronic systemic financial crises was to borrow and spend monumental amounts of money that in essence replaced all private-sector demand lost in the crisis and then some. This "fixed" the chronic crisis by flooding the real economy with enough money that households and businesses could pay down or liquidate old debt (i.e. deleverage) and earn enough to save money that accumulated the capital to fuel a new round of credit expansion.

In terms of risk and moral hazard, all systemic risk was offloaded onto the state, and the consequences of poor risk/money-management decisions were obliterated by the tsunami of borrowed Federal money.

In the quasi-religion of Big Government Borrowing as the risk-free fix to all crises, those saved by Big Government borrowing/spending are victims: victims of unpredictable Nature (drought, illness) or financial crises beyond individual's control (bank failures).

But this worldview excludes moral hazard, that is, the causal connection between poor choices/high risks and poor outcomes. Once the state backstops every loss, regardless of origin, it not only backstops innocent victims, it also backstops non-victims, those who made poor choices that resulted in losses and the parasitic criminal class of those gaming the unlimited backstops of the state.

This dominance of moral hazard discourages integrity and responsibility and incentivizes risky speculation and irresponsible choices and lifestyles. My Mom (83) has told me that she's heard men of her generation exclaim that there is no need to modify their unhealthy lifestyle because "the government will pay for another bypass."

I cite this as an example to show that moral hazard in a system where the state backstops every risk is not reserved for financiers; it infects every recipient of state backstops.

If the state offers someone a near-zero-down payment mortgage at a low interest rate (for example, an FHA or VA mortgage), this is the equivalent of offering a gambler in a casino a compelling deal: keep any winnings (if the house rises in value) and the state absorbs any losses that result from the house declining in value (defaults, etc.)

As noted in the series' first two parts, The Source of Systemic Crisis: Risk and Moral Hazard (August 21, 2013) and The Grand Experiment: Offloading Risk onto the State (August 22, 2013), the potential losses from open-ended risk are also open-ended, while the state's ability to borrow money to backstop every loss is intrinsically limited.

In other words, the Big Government Backstops Everything faith is that crises and losses will be intermittent and shallow, and thus well within the government's ability to unleash a cleansing tsunami of borrowed money that will flood the economy with enough cash and credit to wash out any and all losses.

Systemic financial crises can be fixed with More of the Same--just unleash an even larger tsunami of free (borrowed) money to wash away the losses and financial ills.

The problem with this faith is that the open-ended concentration of risk in the state creates open-ended demands for backstops that eventually exceed the state's ability to borrow money. It's absolutely critical to grasp the difference between government borrowing in World War II and government borrowing in the present.

In World War II, the state imposed wage/price controls and forced full employment by the military draft (here's 15.5 million jobs and you're going to take one) and an extraordinary expansion of industrial production of weaponry and war materiel.

This created a vast pool of private savings that could be invested in War Bonds, the Treasury bonds sold to fund the war. This accumulated savings also provided the capital foundation for the postwar expansion of credit and consumer spending.

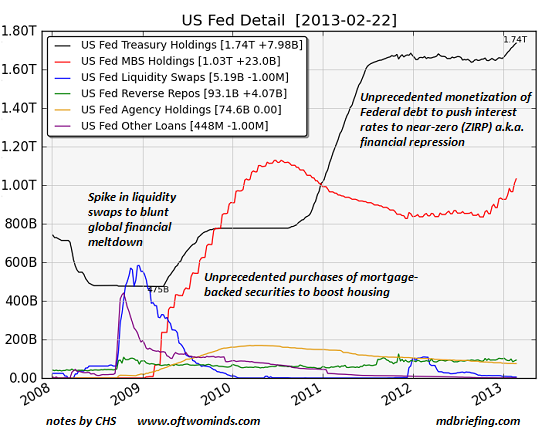

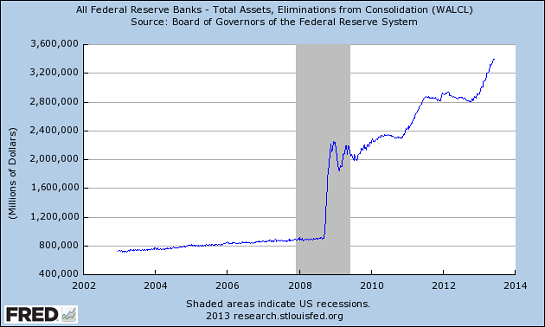

The present borrowing and spending tsunami is fundamentally different: rather than rely on private savings being invested in Treasury bonds (debt), the central bank (Federal Reserve) creates trillions of dollars which it uses to buy Treasury bonds and home mortgages:

$2.6 trillion created and counting:

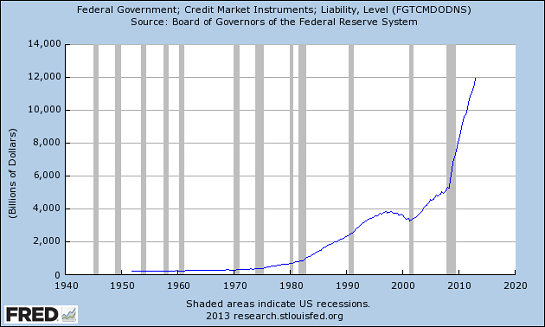

Meanwhile, Federal debt has exploded as borrowing a tsunami of money has turned from "getting through a rough patch" to chronic massive deficit spending:

Note the structural gap between Federal receipts and spending:

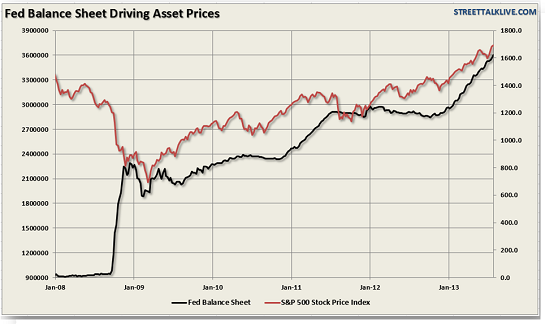

Another critical difference between the World War II tsunami of state money and the present is that the money created by the Fed isn't going into the real economy, it's feeding speculative asset bubbles. Note the near-perfect correlation of the S&P 500 stock market index and the Fed's balance sheet/creation of money:

In other words, the state/central bank backstopping of systemic risk now focuses on creating phantom wealth via speculative bubbles rather than forcing full employment. Rather than "draft" 15 million unemployed into a low-paying civilian equivalent of the World War II military machine, the state/central bank has endeavored to inflate asset bubbles that are supposed to create a "wealth effect" that will magically persuade households and enterprises to go out and borrow and spend.

What are the consequences of a central bank creating trillions of dollars for speculation and a central state borrowing trillions of dollars on a permanent basis?As noted before, risk cannot be extinguished, it can only be offloaded onto someone else or masked for a short time.

The consequences of this sleight-of-hand (the Fed creates money to buy Federal bonds so the government can borrow and blow trillions of dollars) are not yet visible, but there will be consequences at some point; the risks have only been temporarily cloaked.

Federal debt has risen $7.1 trillion since the current systemic financial crisis began in August, 2008, from $9.6 trillion to $16.7 trillion. (You can see for yourself on Treasury Direct). That is an astonishingly large increase. Add in the nearly $3 trillion created and injected into the financial sector by the Fed and the total money-tsunami unleashed to "fix" this systemic financial crisis is close to $10 trillion.

This unprecedented tsunami of money has failed to fix the crisis. Instead, it has created a vast and as-yet invisible risk of collapse of the state/central bank system itself. By concentrating systemic risk into the state, we have not extinguished risk; we have only pooled it into a reservoir dammed by one barrier: the state's ability to borrow and spend virtually unlimited amounts of money.

As I have described in Why Isn't There a Demonstrably Correct Economic Theory? (August 16, 2013), creating money and credit simply creates more claims on existing real-world resources--it doesn't create new wealth or resources. When those claims vastly exceed the underlying wealth/resources, the system of credit and currency claims will implode.

Borrowing and printing $10 trillion hasn't fixed anything; it has only raised the reservoir of risk to the top of the dam. Cracks are opening as the pressure builds, and we should not be surprised when risk and consequence reconnect and the dam gives way.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, Robert Z. ($125), for your outrageously generous contribution to this site-- I am greatly honored by your steadfast support and readership. |