Dollar Demand = Global Economy Has Skidded Over the Cliff

Borrowing in USD was risk-on; buying USD is risk-off.

There is a lively debate about the global demand for U.S. dollars:

Global finance faces $9 trillion stress test as dollar soars (Telegraph.co.uk)

The Dollar Squeeze – How Problematic Is It? (Acting Man)

The Global Dollar Funding Shortage Is Back With A Vengeance And "This Time It's Different" (Zero Hedge), which references a Bank for International Settlements (BIS) paper: Global dollar credit: links to US monetary policy and leverage.

Correspondent Mark G. went through the BIS report and offered these insightful comments:

"Unless you enjoy multivariate regression analysis I suggest skimming the BIS working paper. Major points I got were:

1. Almost all of the dollar denominated debt and bond growth since 2009 was generated by the global shadow banking system. Banks per se were smaller players in issuing this debt, and US-based banks (i.e. the ones in reach of Federal Reserve life preservers) were minor. Sovereign wealth funds are large players in this. When we think of huge sovereign wealth funds held by major hydrocarbon exporters then the pucker factor rises.

One implied result of the BIS paper is that it will be extremely difficult or impossible for Federal Reserve emergency liquidity operations to stem a panic, even if the Fed is inclined to do so. AEP in the Telegraph article stated this more directly. The real problem is that modern bailout operations have large fiscal components as well as monetary components. Looking at the Bundestag's chronic heartburn with Greece and the EFSF is educational. Alternatively, consider how well proposals for a larger TARP type program aimed primarily at foreign entities would be received by the US Congress. And especially in 2016.

2. A major revelation was that $1 trillion of the dollarized lending went into Chinese companies. However the authors claim most of this lending was through Chinese banks.

3. "Emerging Markets" again account for 1/2 of the total offshore dollarized loans and bonds. This is $4.5 trillion and mainly centered in Brazil, Russia, India, China, etc.

4. From page 20:

"Fourth, since the crisis, the Federal Reserve's compression of term premia via its bond buying has led to a surge in US dollar borrowing through bond markets. Time-varying regressions and VARanalysis also indicate that inflows into bond mutual funds played a significant role in transmitting monetary ease, giving evidence of the portfolio rebalancing channel of the Federal Reserve large-scale bond purchases. In particular, given the low expected returns of holding US Treasury bonds (in relation to expected short-term rates), investors have sought out and found dollar bond issuers outside the US, many rated BBB and thus offering a welcome credit spread."

These dollarized bond funds were the "conservative" play for those players unwilling to also assume exchange rate risk.

"BBB..." This is already the S&P/Fitch ground floor of "investment grade." And that was the rating assigned to these foreign issuers during a time of free money and bubble expansion. We already know the bulk of bond mutual fund buyers are institutions. And many are required to flush any paper that falls below investment grade. And being 'smart money' they will have tried to hedge their risks against such a 'Credit Event' with credit default swaps (CDS).

We also know that CDS contracts typically require the CDS writer to begin posting progressively higher amounts of cash collateral as the credit outlook darkens for the underlying instrument. For instance, even if S&P/Fitch merely change the outlook from 'positive' to 'neutral' the required posted collateral percentage rises. And again from neutral to negative and so forth.

In the case of dollar loans and bonds the collateral needs to be in dollars. Therefore even if the CDS writer manages to borrow Euros with wet ink they still have to exchange these for dollars. See USD/Euro FX trend for the result."

Thank you, Mark, for the detailed analysis. Here are my initial thoughts:

Thank you, Mark, for the detailed analysis. Here are my initial thoughts:

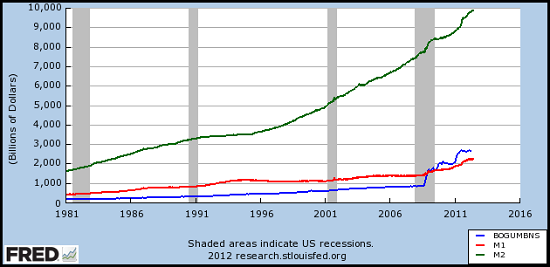

1. Currencies respond to supply and demand like any other commodity. As such, it's instructive to to look at the supply of U.S. dollars and see how it's changed since 2008:money supply (Wikipedia)

2. However you measure money supply, the supply of dollars hasn't risen by much: MZM Money Stock has risen $2 trillion since 2010, Adjusted Monetary Base rose from $1 trillion to $3 trillion, and M2 Money Stock from around $8 trillion to around $10 trillion.

To put that roughly $2 trillion increase in money supply in context:

The GDP of the U.S. is about $17 trillion.

Global GDP is around $72 trillion.

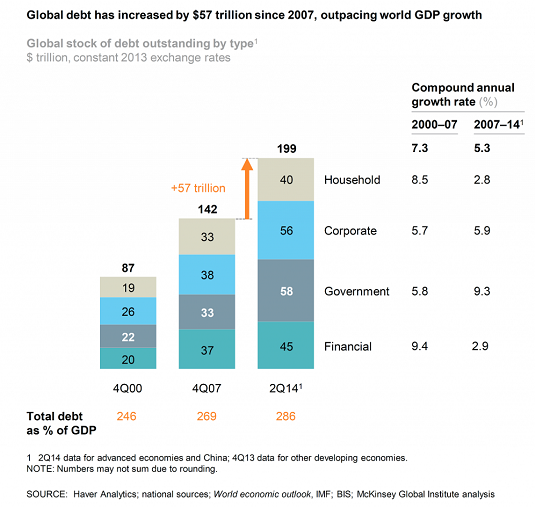

Global debt rose $57 trillion from 2007 to 2014:

3. If there is demand for $9 trillion USD, that dwarfs the increase in US money supply. It also dwarfs the expansion in the Federal Reserve's balance sheet, roughly $3.5 trillion since 2008.

4. Borrowing in U.S. dollars was the easy, profitable trade as long as the dollar was declining. Traders being traders, everybody jumped into the easy, profitable trade with all four feet. Now that the dollar has reversed, everyone who is holding debt in dollars is losing money every time the USD ticks higher.

5. Much of the shadow banking system is opaque, and assumptions made about the outstanding debt in USD are likely to be not just wrong but grossly under-estimated. See #2 above.

If you wanted a trade that was guaranteed to blow up, you couldn't do much better than "dollar bond issuers outside the US, many rated BBB." As Mark noted, once this gunwales-at-sea-level debt gets downgraded a notch, institutional owners will be obligated to sell, regardless of any other conditions. Selling will beget selling.

6. U.S. Treasuries are essentially the only super-liquid safe haven offering a yield above 1%. And what do you need to buy Treasuries? U.S. dollars. The point here is the demand for USD is not limited to those scrambling for USD to pay off dollar-denominated debt--it's a global consequence of the global economy skidding off the cliff into recession.

Borrowing in USD was risk-on; buying USD is risk-off. As the real global economy slips into recession, risk-on trades in USD-denominated debt are blowing up and those seeking risk-off liquidity and safe yields are scrambling for USD-denominated assets.

It's important to recall that buyers of U.S. Treasuries are getting not just the 2+% yield-- they're getting the capital appreciation from the USD rising against their home currency. Depending on the home currency, those who dumped their home currency and bought USD last summer have gained 17% to 25%, even if they received 0% yield.

Add all this up and we have to conclude that, in terms of demand for USD--you ain't seen nuthin' yet.

Get a Job, Build a Real Career and Defy a Bewildering Economy(Kindle, $9.95)(print, $20)

Are you like me? Ever since my first summer job decades ago, I've been chasing financial security. Not win-the-lottery, Bill Gates riches (although it would be nice!), but simply a feeling of financial control. I want my financial worries to if not disappear at least be manageable and comprehensible. And like most of you, the way I've moved toward my goal has always hinged not just on having a job but a career.

Are you like me? Ever since my first summer job decades ago, I've been chasing financial security. Not win-the-lottery, Bill Gates riches (although it would be nice!), but simply a feeling of financial control. I want my financial worries to if not disappear at least be manageable and comprehensible. And like most of you, the way I've moved toward my goal has always hinged not just on having a job but a career.You don't have to be a financial blogger to know that "having a job" and "having a career" do not mean the same thing today as they did when I first started swinging a hammer for a paycheck.

Even the basic concept "getting a job" has changed so radically that jobs--getting and keeping them, and the perceived lack of them--is the number one financial topic among friends, family and for that matter, complete strangers.

So I sat down and wrote this book: Get a Job, Build a Real Career and Defy a Bewildering Economy.

It details everything I've verified about employment and the economy, and lays out an action plan to get you employed.

I am proud of this book. It is the culmination of both my practical work experiences and my financial analysis, and it is a useful, practical, and clarifying read.

Test drive the first section and see for yourself. Kindle, $9.95 print, $20

"I want to thank you for creating your book Get a Job, Build a Real Career and Defy a Bewildering Economy. It is rare to find a person with a mind like yours, who can take a holistic systems view of things without being captured by specific perspectives or agendas. Your contribution to humanity is much appreciated."

Laura Y.

Gordon Long and I discuss The New Nature of Work: Jobs, Occupations & Careers(25 minutes, YouTube)

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

| Thank you, John D. ($100), for your outrageously generous contribution to this site-- I am greatly honored by your steadfast support and readership. |