Will Cash Always Be Trash, Or Will It One Day Be King?

When the phantom wealth evaporates and risk assets go bidless, cash will once again be king, for the simple reason there will be so little of it.

Occasionally it's a good idea to step away from the daily grind to consider the larger issues we all face--for example, the future of the money we earn and the bits we invest in something we hope holds or increases its value.

At present, cash is trash: cash earns almost no yield, and in some countries it now earns a negative interest rate, meaning it costs you to park your cash in a bank.

Even cash equivalents such as one-year Treasury bonds pay almost nothing.

Those who avoided debt and risky assets since 2009 have seen their cash lose value when adjusted for inflation, while those who borrowed to the hilt and bought risk-on assets such as stocks, junk bonds and high-end housing have skimmed monumental gains for doing what the central banks incentivized: borrowing money and buying speculative risk-on assets.

Correspondent Kevin K. recently sent me a link to a home in the San Francisco Bay Area that was purchased around the crash era (2008-09) for $1.4 million, and sold last year for $2.1 million.

Assuming a conventional 20% down payment of $280,000, the savvy buyer borrowed $1.12 million at historically low rates and offloaded the house 6 years later for a cool $560,000 profit (assuming a 6% sales commission and closing costs).

That's a 200% return on the $280,000 cash down payment--a healthy reward for borrowing to the hilt for a mere 6 years.

Anyone who margined to the hilt in 2009 and rode the stock market higher with borrowed money easily earned returns in excess of 200%.

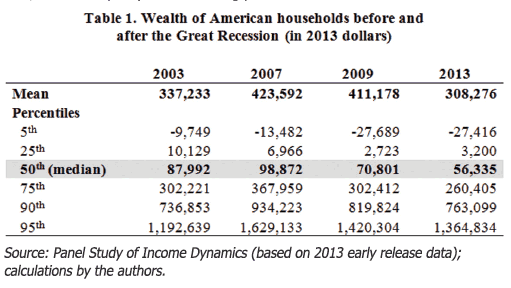

Yet how many people did so? Consider this chart of the wealth of U.S. households before and after the Global Financial Meltdown and Great Recession.

By the look of it, even the top 5%--individuals earning taxable incomes of $120,000 or more, according to the Social Security Administration, or households with total incomes around $350,000, according to the U.S. Census Bureau (Table F-3. Mean Income Received by Each Fifth and Top 5 Percent of Families, XLS file)--have yet to regain the value of assets owned in 2007, before the Global Financial Meltdown/Great Recession.

If the top 5% had borrowed/margined to the hilt and dumped all that dough into risk assets, their net wealth would have skyrocketed. Clearly, few did so.

This suggests those who did margin/borrow to the hilt were in the top 1% or .1%. 95% of 2009-2012 Income Gains Went to Wealthiest 1%: Average inflation-adjusted income per family climbed 6% between 2009 and 2012, the first years of the economic recovery. During that period, the top 1% saw their incomes climb 31.4% — or, 95% of the total gain — while the bottom 99% saw growth of 0.4%.

What would have to happen for cash to be transformed from trash to "cash is king"? The basic answer is: all the risk-on credit/asset bubbles that have richly rewarded those who have speculated with borrowed money will have to implode and be impervious to central bank attempts to re-inflate the bubbles.

What conditions would have to be present for credit/assets to implode and not recover?

We are in uncharted territory in terms of the global bubble in credit and risk-on assets, so the answer isn't immediately clear. Here are some possibilities:

1. Credit growth falters.

2. Borrowing dries up (despite abundant credit).

3. A global scramble for cash to pay debt and the costs of lavish lifestyles triggers the liquidation of risk-on assets.

4. The risk-on assets go bidless, i.e. nobody wants luxury yachts, super-cars, estates, etc. at any price because the value is plummeting.

5. As phantom wealth evaporates, everyone realizes the collateral propping up the mountains of debt is either impaired or non-existent.

When the phantom wealth evaporates and risk assets go bidless, cash will once again be king, for the simple reason there will be so little of it. When the opposite of the present dynamic is "impossible," then the "impossible" becomes not just likely but inevitable.

Get a Job, Build a Real Career and Defy a Bewildering Economy(Kindle, $9.95)(print, $20)

Are you like me? Ever since my first summer job decades ago, I've been chasing financial security. Not win-the-lottery, Bill Gates riches (although it would be nice!), but simply a feeling of financial control. I want my financial worries to if not disappear at least be manageable and comprehensible.

And like most of you, the way I've moved toward my goal has always hinged not just on having a job but a career.

You don't have to be a financial blogger to know that "having a job" and "having a career" do not mean the same thing today as they did when I first started swinging a hammer for a paycheck.

Even the basic concept "getting a job" has changed so radically that jobs--getting and keeping them, and the perceived lack of them--is the number one financial topic among friends, family and for that matter, complete strangers.

So I sat down and wrote this book: Get a Job, Build a Real Career and Defy a Bewildering Economy.

It details everything I've verified about employment and the economy, and lays out an action plan to get you employed.

I am proud of this book. It is the culmination of both my practical work experiences and my financial analysis, and it is a useful, practical, and clarifying read.

Test drive the first section and see for yourself. Kindle, $9.95 print, $20

"I want to thank you for creating your book Get a Job, Build a Real Career and Defy a Bewildering Economy. It is rare to find a person with a mind like yours, who can take a holistic systems view of things without being captured by specific perspectives or agendas. Your contribution to humanity is much appreciated."

Laura Y.

Gordon Long and I discuss The New Nature of Work: Jobs, Occupations & Careers(25 minutes, YouTube)

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Get a Job, Build a Real Career and Defy a Bewildering Economy(Kindle, $9.95)(print, $20)

Are you like me? Ever since my first summer job decades ago, I've been chasing financial security. Not win-the-lottery, Bill Gates riches (although it would be nice!), but simply a feeling of financial control. I want my financial worries to if not disappear at least be manageable and comprehensible.

And like most of you, the way I've moved toward my goal has always hinged not just on having a job but a career.

You don't have to be a financial blogger to know that "having a job" and "having a career" do not mean the same thing today as they did when I first started swinging a hammer for a paycheck.

Even the basic concept "getting a job" has changed so radically that jobs--getting and keeping them, and the perceived lack of them--is the number one financial topic among friends, family and for that matter, complete strangers.

So I sat down and wrote this book: Get a Job, Build a Real Career and Defy a Bewildering Economy.

It details everything I've verified about employment and the economy, and lays out an action plan to get you employed.

I am proud of this book. It is the culmination of both my practical work experiences and my financial analysis, and it is a useful, practical, and clarifying read.

Test drive the first section and see for yourself. Kindle, $9.95 print, $20

"I want to thank you for creating your book Get a Job, Build a Real Career and Defy a Bewildering Economy. It is rare to find a person with a mind like yours, who can take a holistic systems view of things without being captured by specific perspectives or agendas. Your contribution to humanity is much appreciated."

Laura Y.

Gordon Long and I discuss The New Nature of Work: Jobs, Occupations & Careers(25 minutes, YouTube)

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

| Thank you, Ray W. ($50), for your superlatively generous contribution to this site-- I am greatly honored by your steadfast support and readership. |