Maybe focusing on next quarter's profits and reaping short-term gains from financializing everything under the sun with debt weren't such great ideas after all.

Traditionally, the two taboo subjects are sex and money. Perhaps we should add demographics, as sex and money determine demographics which then determine the trajectory of the economy and society.

Sex, Money and Demographics are wide open to interpretation. I'm sketching out what I consider "obvious," but what's "obvious" to others may well be completely different.

The Modern Era has untethered a great many socio-economic bonds. In the current era, economics reigns supreme: everything is interpreted through a financial lens. But social-cultural forces--more difficult to measure than money--are intertwined with economic forces.

For example, the social-cultural obligation of men to marry the woman they impregnated decayed not just because the state began supporting single mothers with social welfare but as part of broader social forces untethering social obligations across a wide spectrum.

Birth control equalized the untethering of sex and the responsibilities / obligations of bearing a child. Women were as free as men to have sexual relations that were untethered from becoming pregnant /bearing a child.

The equalization of gender roles played out culturally, socially and economically. The signal value of Modernity is the elevation of the Self / Individual above all the constraining orders: family, the employer, the state. All these structures are now viewed through the lens of the Self.

Culturally, the notion that women should have fewer freedoms than men due to traditional gender roles was no longer justifiable. Women could choose a traditional gender role, but they could also choose to pursue employment and opportunities traditionally reserved for males.

Legal and financial structures changed to reflect this. Legal mandates required women's sports to be funded on par with men's sports.

Larger economic-financial forces were also at work. As inflation and globalization ate away the purchasing power of wages in the 1970s, households found that one wage-earner (traditionally the husband/father) could no longer earn enough to support the desired middle-class lifestyle of homeownership and secure finances.

So "women's liberation" melded with financial necessity. Women were "liberated' from the household in order to earn wages to increase the purchasing power of household income.

In strictly financial terms, financializing the household economy was highly expansive and profitable. Replacing all the services performed by the stay-at-home mom with corporate services financialized the traditional household economic functions, and the vast expansion of household credit--credit cards, and then later, home equity loans--financialized the savings and frugality of the traditional household.

As the household's income soared, it was spent on childcare, eldercare, takeout meals, housecleaning services, au pairs, etc.--replacing all the services performed by the stay-at-home mom with financialized transactions that turned a profit for someone or some enterprise. As the costs of these services rose, debt--the financialization of the household budget--filled any gaps that opened between income and spending.

Japan's giant real estate asset bubble in the late 1980s transformed housing from shelter into a financialized asset. This financialization of housing has gone global, and since capital (which views housing as nothing more than an asset generating appreciation and income) has far deeper pockets than households (which view housing as shelter and long-term security), capital can always outbid households.

It makes perfect sense to capital to leave dwellings empty. Renting creates overhead and risk, and since the core driver of housing as an asset is appreciation due to the bidding war of capital seeking low-risk assets to snap up, then it's sensible to hoard housing because it can't be replaced at the original price.

So dwellings sit empty. They're not shelter, they're an asset to hoard. This is the net result of the financialization of households and housing.

The net result of this global financialization of households and housing is only the wealthiest households can afford to buy a house and have children. And the net result of this is crashing birth rates and rising debt as households and states attempt to maintain their desired lifestyles by borrowing money.

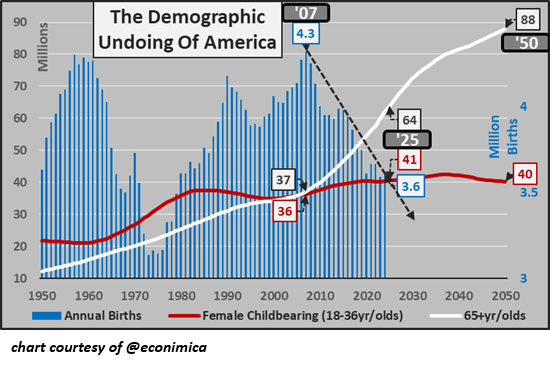

Here's a snapshot of America's demographics. Population scale is on the left, births scale is on the right. females of childbearing age are stable (between 35 and 40 million) while the number of elderly (65+) is rising, on track to almost double in one generation (from 2007 to 2027).

Ultimately, the elderly depend on the younger generations to keep the economy/society functioning. That gets harder as the number of elderly rises and the number of young workers entering the workforce crashes.

Yes, AI and robots will fix all this, but AI and robots are not "free," they have inherently high costs. So will they pay for themselves? By what means, if they are not consumers generating profitable transactions?

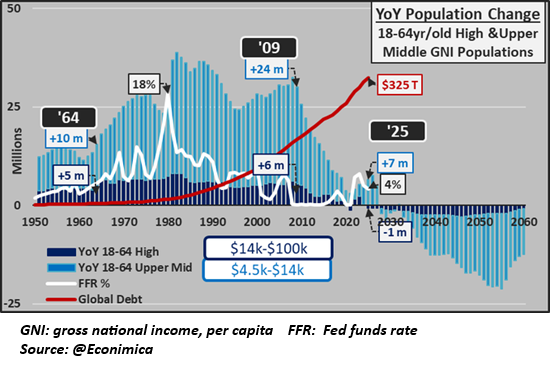

Here's a snapshot of China's demographics. Births have fallen rapidly from 24 million annually to 7 million annually. The Fed Funds Rate and global debt are shown as the financial backdrop of low interest rates fueling skyrocketing debt, which ultimately must be paid by the workforce. China's population--along with many other developed and developing nations--will decline as a demographic consequence of falling birth rates.

Untethering individuals from social obligations has boosted financialization profits and debt, but at the cost of undermining the household, which is the foundation of child-rearing and the next generation. To Capital--focused on higher valuations and profits next quarter--financializing the household and shelter were nothing more than opportunities to rake in higher profits and gain--the same modus operandi as financializing healthcare.

Capital is about to discover the long-term consequences of their financialization of the household and shelter is the demographic collapse of their societies and economies. Maybe focusing on next quarter's profits and reaping short-term gains from financializing everything under the sun with debt weren't such great ideas after all.

My book Investing In Revolution is available at a 10% discount ($18 for the paperback, $24 for the hardcover and $8.95 for the ebook edition).

Introduction (free)

Check out my updated Books and Films.

Become

a $3/month patron of my work via patreon.com

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Sean M. ($7/month), for your wondrously generous subscription

to this site -- I am greatly honored by your support and readership.

|

|

Thank you, Craig F. ($70), for your marvelously generous subscription

to this site -- I am greatly honored by your support and readership.

|

|

Thank you, Marian F. ($7/month) for your splendidly generous subscription

to this site -- I am greatly honored by your support and readership.

|

|

Thank you, Freedman ($7/month) for your enormously generous subscription

to this site -- I am greatly honored by your support and readership.

|