The Immense (and Needless) Human Misery Caused by Speculative Credit Bubbles

Financialization and the Neocolonial Model of credit-based exploitation leave immense human suffering in their wake when speculative credit bubbles inevitably implode.

Discussions of the global financial crisis tend to be bloodless accounts of policy and "growth." This detachment masks the immense and totally needless human misery created by financial engineering. A correspondent with first-hand knowledge of the situation in Cyprus filed this account:

"RE: the Cyprus economic crisis, the politicians are unbowed by the chaos they caused, still behaving as they have always done, preaching populist platitudes, corrupt as ever, unapologetic. A poll showed that 99% of Cypriots believe their government is corrupt.

Yesterday, the former president, Demetris Christofias, appeared before a tribunal investigating the causes of the economic collapse. He tried to force the tribunal to do what he told them, saying, "I am not just any witness, I was the President of the Republic for 5 years". They told him where to get off and he stormed out.

Little hope for this country. Money leaving. Best talent leaving. Foreign investment in a planned energy hub has been hijacked by the politicians. Cyprus is returning back to what it always was: a tourist destination run by shopkeepers and farmers.Sad days. Most people feel betrayed by the politicians and big powers."

This report highlights a key dynamic of speculative credit/banking bubbles: they require the complicity of central banks and the state. Speculative bubbles based solely on cash have very short lifespans, as the bubble bursts violently as soon as the gamblers' cash has been sucked into the vortex.

Truly devastating speculative bubbles require a vast expansion of credit and the corruption of the political class that feeds off the state. As Credit is ultimately managed by the state, central banks and the banking cartel, no speculative credit bubble can arise without the complicity and collaboration of all three.

Speculative credit bubbles are the hallmark of parasitic financial systems and what I term the Neofeudal-Neocolonial Model of Financialization: In the neofeudal, neocolonial model, speculation by the parasitic Aristocracy is backstopped by the taxpayers--the perfection of moral hazard. The E.U., Neofeudalism and the Neocolonial-Financialization Model (May 24, 2012).

Future taxpayers are burdened with crushing mountains of debt taken on to fund corrupt state fiefdoms and politically sacrosanct cartels and constituencies.

Debt (that profits the parasitic financial Aristocracy) is heavily incentivized while saving capital (cash) is punished with negative yields.The incentives to accumulate cash capital and invest it productively rather than speculatively are systematically destroyed.

This is the essence of the neocolonial model: make money cheap, reward consumption and speculation in asset bubbles and draw once-prudent citizens into debt-serfdom. Those not ready for big-mortgage serfdom are snared with $100,000 student loans.

This is the same mechanism used to stripmine colonies with financialization: no coercion necessary. "They did it to themselves."

This neocolonial model leads to neofeudalism: Once the asset bubble burst, your (phantom) wealth has vanished, but you still owe us the debt. In an economy based on debt, servicing that debt absorbs much of the income. So you need to borrow more to get by.

The destructive incentives, corruption and erosion of productive investment are masked by the rapidly rising phantom wealth created by the bubble in real estate and stocks. Something else happens when speculative credit bubbles inflate housing: rents also rise as the cost of buying homes skyrockets.

As a result, even those who prudently avoided buying into bubbles see their incomes siphoned off.

This is what speculative credit bubbles look like in household terms:

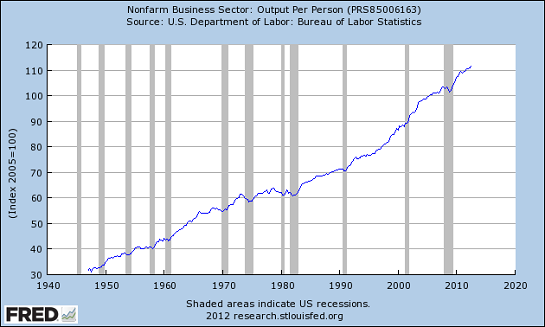

Productivity per worker keeps increasing:

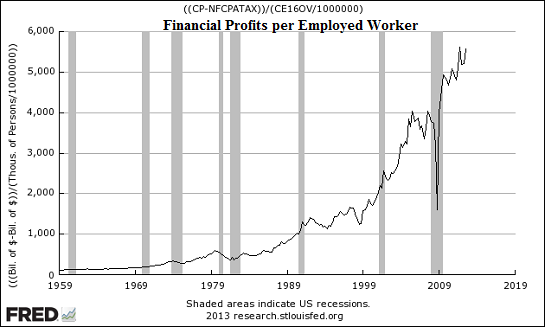

As do financial profits per worker:

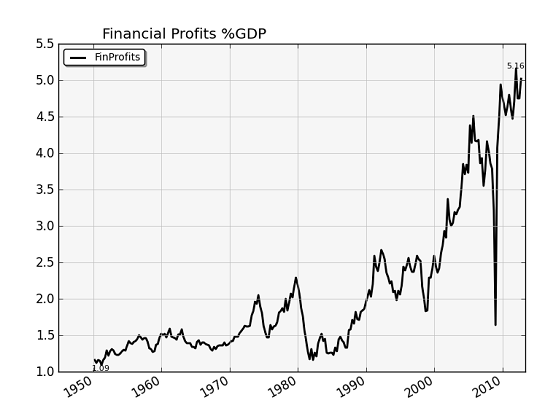

Financial profits as a share of the economy have soared:

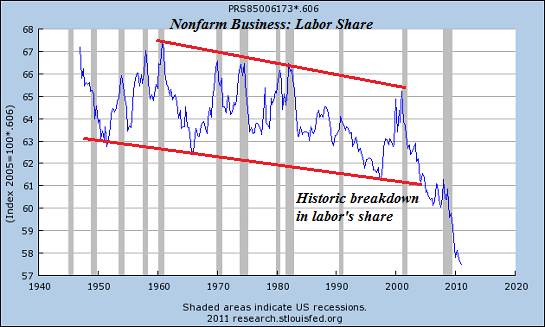

But the share of a financialized neofeudal economy that flows to workers declines:

Adjusted for inflation, real household incomes stagnate even as the credit bubble boosts the value of assets owned by the financial Aristocracy:

The Neofeudal-Neocolonial Model is playing out everywhere as the home economies are ruthlessly pillaged in the financialized version of the old colonial exploitation model:

The Eurozone's Three Fatal Flaws (September 21, 2011)

My definition of Neoliberal Capitalism differs significantly from the conventional view: markets are opened specifically to benefit the Central State and global corporations, and risk is masked by financialization and then ultimately passed onto the taxpayers. In this view, the essence of Neoliberal Capitalism is: profits are privatized but losses are socialized, i.e. passed on to the taxpayers via bailouts, sweetheart loans, State guarantees, the monetization of private losses as newly issued public debt, etc.

The consequences of this vast transfer of risk and the cleanup costs of the credit bubble to citizens and debt-serfs is human misery on an immense scale.

Are you in the New York City region? Meet other OfTwoMinds Like-Minded people(via Meetup) interested in building social capital and exploring the alternative ideas presented here. Check it out! (Thank you, Neil T. for establishing this Meetup.)

Are you in the New York City region? Meet other OfTwoMinds Like-Minded people(via Meetup) interested in building social capital and exploring the alternative ideas presented here. Check it out! (Thank you, Neil T. for establishing this Meetup.)

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, Brent M. ($10), for your most generous contribution to this site-- I am greatly honored by your support and readership. |