The Anxiety Economy

We're told to stop being so darn negative even as the tsunami of inequality washes away the beach chairs of the bottom 90%.

The disconnect between the happy story of the economy is growing healthily, so all is well and the insecurity and stagnation experienced by the bottom 90% of wage earners has been widening since the wheels fell off in 2008. One would be forgiven for assuming that a smartly growing economy would increase the general sense of security and reduce the general awareness of precarity. But alas, this assumption is false: the sense of precariousness is rising as the sense of security has slid off a cliff.

Welcome to the Anxiety Economy, a term coined by longtime correspondent Bart D., who describes the term thusly:

"By my reckoning the Anxiety Economy is an adjunct to (and perhaps to some degree a product of) the Landfill Economy model.

There was a time when the economy was designed to provide surety and stability. Jobs were stable, opportunities to create increasing wealth (particularly small business creation) were uncomplicated and products were designed to be genuinely better and longer lasting with every iteration. I think this typified the late 1800s to the early 1970s.

Since the 1970s we've seen stable jobs drastically reduce along with the durability and usefulness of new product iterations and trying to comply with the massive regulatory burden of businesses as simple as washing dogs or growing vegetables has become mind bending and expensive.

We get bombarded in news and other media with stories of house fires, chronic illnesses and car crashes in places very far away and disconnected from us (interspersed with, and no doubt sponsored by, marketing for insurances of every kind) that make us feel that the risks we face of loss of assets and health are waaaay bigger than they actually are. So that we buy expensive insurances.

All of this means we feel far less certain about long term income, our ability to run business and create wealth, we understand that everything we buy will fail pretty fast and needs to be replaced and we have a wildly over exaggerated sense of the need for expensive insurances.

These things make for very high anxiety about sustaining our lifestyle. Adding to this is the shift in economic activity from making things of merit to commodifying (and rendering taxable and insurable) the things families once did for each other--most significantly child rearing and aged care. We feel we can't rely on family to care for us or are made to feel guilty/a burden on family if we lean on them to look after us in old age.

The economic system is now designed to make people feel:

--Uncertain about our ability to meet the cost of future needs

--Locked into a constant and ever shortening cycle of replacement for what should be 'durable goods'

--Inadequate in their abilities to do business and make wealth

--Over-exposed to risk

--Unsure about their future health and care.

You mentioned the need to simplify our lives--Amen to that! And this is a growing sentiment I'm hearing from many people. The issue is the Anxiety Economy makes it very hard to achieve that simplification. It actively blocks people from disengaging. Because once that movement takes hold, the power of wealth will decline dramatically."

In other words, the Anxiety Economy benefits the few at the expense of the many--the definition of a broken, exploitive economy that is optimized to generate enormous asset-inflation wealth for the top 10% who own the vast majority of income producing assets while sapping the purchasing power and security of wage earners.

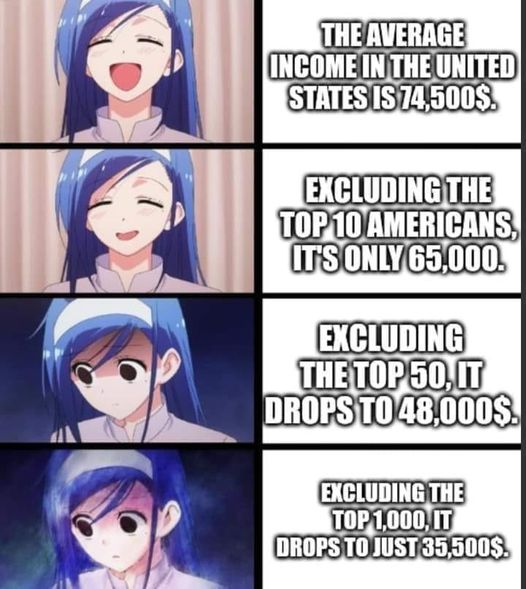

The status quo's high-profile, highly paid cheerleaders have a quiver full of tricks to mask the Anxiety Economy's soaring inequality. One old trick that still works on the unwary is to tout average household income and average household wealth. This is a trick because stupendous sums of income and wealth accrue to the very top of the wealth pyramid in the U.S., and this massively distorts the average income.

Median income also fails to capture the extremes of income inequality that characterize the American economy, but it's less distorted than average income.

In 2022, the average US household income was $105,555, while the median was $74,580.

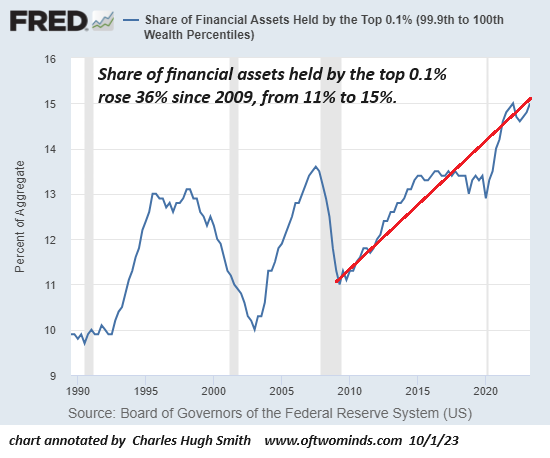

As this St. Louis Federal Reserve chart shows, the top 0.1% of households--130,000 households out of 130 million--own 15% of the nation's financial wealth.

This wealth is highly concentrated within the top 0.1%. While I cannot vouch for the accuracy of the statistics cited in this graphic, the general idea is simple math: strip out the apex of the income-wealth pyramid, and the average income-wealth numbers plummet to Earth.

According to the Bureau of Labor Statistics (BLS),

"Real average hourly earnings increased 0.8 percent, seasonally adjusted, from May 2023 to May 2024.

The change in real average hourly earnings combined with a decrease of 0.3 percent in the average

workweek resulted in a 0.5-percent increase in real average weekly earnings over this period."

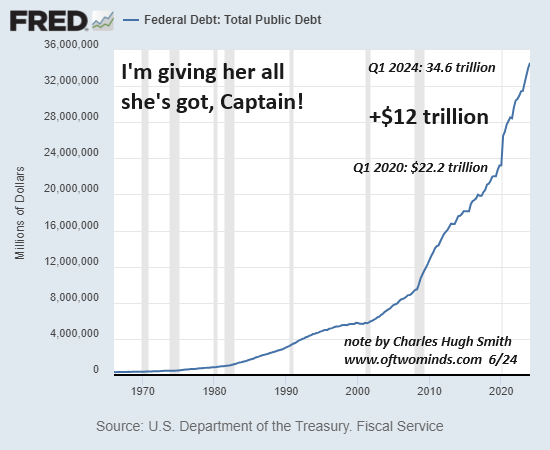

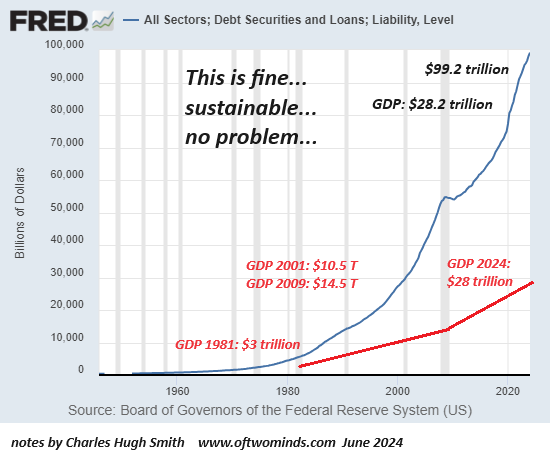

Assuming the official inflation statistics are actually accurate (try not to bust a gut laughing), that's a mighty thin dime of additional earnings for those earning $20/hour. Whoopie. Now consider the completely unprecedented enormity of the debt-funded stimulus (never mind the Federal Reserve's $4 trillion in stimulus and open-ended goosing of the stock market via proxies) since 2020--$22 trillion in new borrowing since Q1 2020--and we see just how paltry the gains were for wage earners. Here's Federal debt, up $12 trillion:

And here's total debt, up $22 trillion.

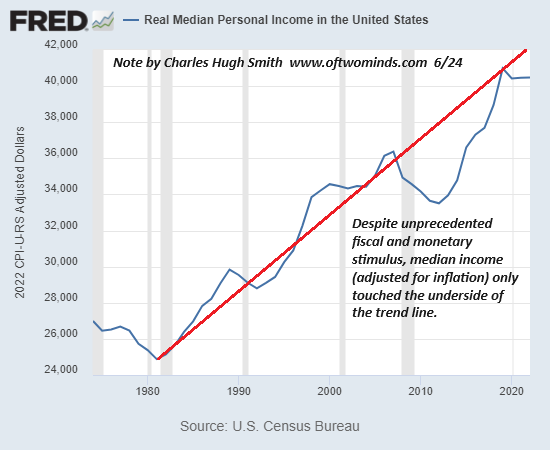

And to show how sustainable income increases failed to materialize, here is a chart of real (adjusted for inflation) median personal income. Note the collapse that occurred after the Global Financial Meltdown of 2008, and that personal income never recovered the trendline other than a brief pandemic-stimmy-induced spike that quickly faded.

In summary: wage earners never recovered from the 2008 meltdown. No wonder the gap between the cheerleaders' delusional insistence that we're all getting richer in every way, every day and the lived reality of the work force who didn't have the means to buy stocks at the 2009 bottom or buy a portfolio of rental houses in 2010.

We're told to stop being so darn negative even as the tsunami of inequality washes away the beach chairs of the bottom 90%. The Anxiety Economy is remarkably profitable for the top few and remarkably unhealthy for everyone else. They're pleased to prescribe us meds to take the edge off the Anxiety Economy, but meds won't fix what's broken in our economy or social order.

Podcasts:

Crisis, Sacrifice and the New Economy, with Emerson Fersch (1 hour)

Financial Nihilism, Inflation & The Collapsing American Dream.

My recent books:

Disclosure: As an Amazon Associate I earn from qualifying purchases originated via links to Amazon products on this site.

Self-Reliance in the 21st Century print $18, (Kindle $8.95, audiobook $13.08 (96 pages, 2022) Read the first chapter for free (PDF)

The Asian Heroine Who Seduced Me (Novel) print $10.95, Kindle $6.95 Read an excerpt for free (PDF)

When You Can't Go On: Burnout, Reckoning and Renewal $18 print, $8.95 Kindle ebook; audiobook Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States (Kindle $9.95, print $24, audiobook) Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet (Kindle $8.95, print $20, audiobook $17.46) Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook) Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel) $4.95 Kindle, $10.95 print); read the first chapters for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print) Read the first section for free

Become a $3/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Kenneth L. ($7/month), for your splendidly generous subscription to this site -- I am greatly honored by your support and readership. |

Thank you, Michael W. ($40), for your much-appreciated generous subscription to this site -- I am greatly honored by your steadfast support and readership. |

|

|

Thank you, Sam F. ($200), for your beyond-outrageously generous subscription to this site -- I am greatly honored by your steadfast support and readership. |

Thank you, Greg ($70), for your superbly generous subscription to this site -- I am greatly honored by your support and readership. |