Goliath dies not because collapse occurs, but because scale mistakes itself for life. What survives was never his.

This guest essay by longtime correspondent 0bserver speaks to a dynamic woven into all of my work: the intrinsic impossibility of fixing what technocratic management broke with more technocratic management. Attempts to do so result in doing more of what's failed, with fatal consequences for the systems being "fixed," as the technocratic elite holds the power to impose policies but is immune to the consequences of the failure of those policies. Those fall on the system, which then veers into incoherence and Model Collapse.

I've been reading Luke Kemp's

Goliath's Curse: The History and Future of Societal Collapse with care, because the book is serious, well-researched, and written from within institutions that spend their days thinking about systemic fragility. Kemp is not unserious, nor is he shallow. His diagnosis of elite failure, complexity, inequality, and institutional overreach aligns with much of what many of us have been warning about for years.

Where I think the book ultimately fails, however, is not in what it sees--but in what it cannot see from the altitude at which it operates.

Kemp's collapse framework is managerial. Collapse is treated as a system-level pathology to be prevented through coordination, governance, and institutional reform. This makes sense given his professional formation and affiliations, but it creates a blind spot that becomes more consequential the longer one reads: continuity is assumed, not explained.

The book speaks fluently about sustainability, inequality, elite capture, and long-term risk. Yet it does not seriously engage with inheritance--not inheritance as wealth alone, but inheritance as transmission: skills, trades, family structure, norms, fertility, competence, and responsibility carried forward across generations. Sustainability is framed as system stability rather than generational renewal.

This omission matters, because collapse is not the absence of order. It is the failure of particular scales of organization. When large institutions fail, life does not disappear--it reorganizes. The question is not whether systems can be stabilized indefinitely, but whether anything capable of inheritance remains when stabilization fails.

Luke Kemp is excellent at identifying fragility in centralized systems. He is far less interested in, or perhaps less equipped to examine, the base-rate reality that most societies muddle through breakdowns via informal order, households, and local competence. This is where pessimism overweights evidence. Failure is dramatic and legible; endurance is quiet and distributed.

Where this becomes decisive is in Kemp's proposed solutions.

When collapse looms, the remedies offered are more coordination, better governance, stronger institutions, improved global frameworks, and smarter management of risk. Complexity is to be handled by expertise; inequality by policy; instability by coordination. The scale that failed is asked to save itself.

This is the core problem.

The solutions operate at the same level as the failure.

Centralization is offered as the cure for overextension.

Governance is offered as the cure for institutional fragility.

Coordination is offered as the cure for complexity.

The very mechanisms meant to prevent collapse amplify its consequences when they fail.

Recent history supplies proof--not theory.

The financial collapse of 2008 rescued banks while households absorbed the loss. Large institutions were recapitalized immediately; families lost homes, savings, and years of accumulated effort. Recovery was declared long before household continuity returned.

The pandemic reinforced the same pattern. Large corporations were deemed essential, while small and local businesses were declared nonessential and shuttered. Compliance favored scale; capital consolidated upward; independent capacity quietly disappeared.

A third proof is now unfolding without crisis declarations. Large banks continue to grow while private equity consolidates trades and local services--plumbing, HVAC, electrical, veterinary clinics, small manufacturing. Businesses are bought, debt-loaded, stripped, and optimized for extraction. Ownership disappears, stewardship evaporates, and nothing is left to inherit when failure arrives.

These outcomes are not policy accidents.

They are the predictable result of scale-first solutions.

Systems are stabilized.

Households are tested.

Continuity bears the cost.

What troubles me most is that Goliath's Curse critiques elites and inequality while failing to recognize how insulated analysis itself has become. Collapse expertise that cannot be lived becomes abstract. Risk is modeled without skin in the game. Moral urgency is asserted without moral grounding. The book makes moral claims--about obligation, responsibility, and injustice--without ever naming the source of those obligations.

This creates a quiet contradiction. Moral language is necessary to motivate coordination, but moral foundations are left ambiguous to preserve managerial flexibility. In the absence of grounding, obligation eventually collapses into power.

Nassim Nicholas Taleb has a name for one failure mode here: the intellectual yet idiot--not stupid, not malicious, but insulated from consequence. I don't think Luke Kemp himself is the target. The framework is. Collapse theory that remains legible only to institutions will always propose institutional solutions, even when the problem has already migrated below that level.

The real threat is not collapse per se. Systems rise and fall. The real threat is the dissolution of the family and the erosion of inheritance.

Institutions can be recapitalized. Markets can reprice. States can fragment and re-form. Families cannot be substituted.

When families fail to reproduce competence, culture, and responsibility across generations, nothing downstream inherits. What follows is not collapse but vacancy.

Goliath dies not because collapse occurs, but because scale mistakes itself for life. What survives was never his.

That is the argument I think Goliath's Curse gestures toward but cannot complete from where it stands. The book diagnoses fragility well. It does not yet explain endurance.

And in the end, endurance--not prevention--is what decides the future.

This is a guest essay by longtime correspondent 0bserver.

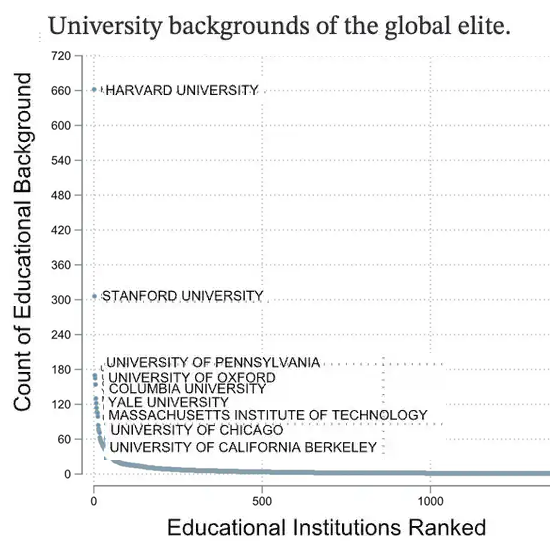

CHS here: note that the global technocrat elite follows a power law distribution in where they attended university:

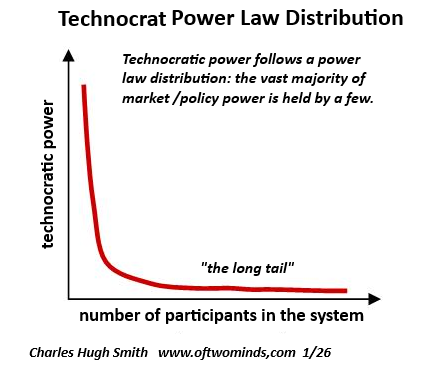

...and the power they wield in markets and institutions:

My new book Investing In Revolution is available at a 10% discount ($18 for the paperback, $24 for the hardcover and $8.95 for the ebook edition).

Introduction (free)

Check out my updated Books and Films.

Become

a $3/month patron of my work via patreon.com

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Robert M. ($7/month), for your outrageously generous subscription

to this site -- I am greatly honored by your support and readership.

|

|

Thank you, Green Dragon Gal ($7/month), for your magnificently generous subscription

to this site -- I am greatly honored by your support and readership.

|

|

Thank you, ChiSox ($7/month) for your superbly generous subscription

to this site -- I am greatly honored by your support and readership.

|

|

Thank you, Claire ($7/month) for your splendidly generous subscription

to this site -- I am greatly honored by your support and readership.

|