2022: The Year of Breakdown

In other words, our economy and society have been optimized for failure.

If we look at the fragility and instability of essential systems, it's clear that 2022 will be the year of breakdown.

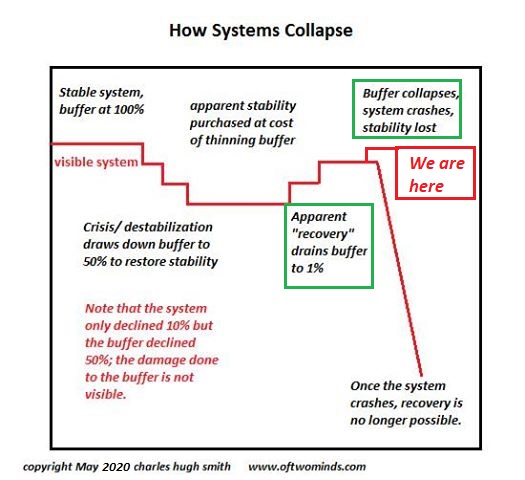

Let's start by reviewing how systems break down, a process I've simplified into the graphic below.

1. Regardless of whether it was planned or not, all systems are optimized to process specific inputs to generate

specific outputs. Each system is pared down to maximize efficiency as the means to maximize profits. This efficiency in

service of maximizing profits requires trade-offs that only become visible when some key part of the system fails.

The system that ships containers around the world offers a useful example. Shipping containers revolutionized

shipping and reduced costs by commoditizing containers (all standard sizes), container ships (specifically designed to carry

thousands of containers and container ports with specifically designed cranes, docks and truck lanes / queueing.

It's possible to load a container on some other craft with a jury-rigged crane, but the efficiency of that is essentially

a fraction of the optimized system: the jury-rigged crane will only be able to load a handful of containers, the ship

will only be able to carry a few containers, and the likelihood of the containers shifting increases.

The infrastructure and labor are both highly specialized. Calling out the National Guard to speed up container

offloading is a useless gesture unless the Guard can deliver more cranes and experienced operators.

The greater the optimization, the greater the fragility as the breaking of any one link brings the entire system

to a halt. Throwing in equipment and labor that the system isn't designed to use will fail.

Virtually every essential system has been stripped of redundancy, resilience, reserves and adaptability as the means

to fully optimize inputs, processes and outputs. The system works well if every link in the dependency chain

is working perfectly. Should one link go down, the entire system goes down.

2. Cost-cutting has stripped systems of back-up staffing and expertise. Full-time workers have been replaced by

gig workjers, contract workers, part-time staff on call, etc. Experienced staff cost too much so they've been

let go as well, so there is no depth in numbers or knowledge.

3. Management is top-heavy with MBAs and bean-counters with little pragmatic experience or knowledge of the systems

they're managing. Management is optimized to advance those who can generate big profits, not those with

experiential skills needed to meet crises in real-world dependency chains, production, breakdowns, etc. So when the

system comes apart, managers simply don't have the knowledge or skills to solve real-world problems.

The skills that are most desirable when everything is running smoothly are useless in crisis. Who do you want

to go into combat with, the continuously promoted officer who won high marks for filing reports on time or the officer

with actual combat experience who got passed over for promotion because he/she didn't devote the proper attention to

paperwork, meetings, virtue-signaling and derriere-kissing?

Unfortunately the vast majority of our systems are managed by people who lack the long experience and hands-on

skills needed to meet cascading crises.

4. Systems are now so complex and opaque that they are in effect optimized to fail in ways that are impervious

to quick fixes. Bureaucratic mission drift, virtue-signaling, the erosion of accountability, multiplying platforms

and software and the endless expansion of compliance and regulatory burdens have loaded every system with

numerous points of failure and procedural friction that contributes little or nothing to the organization's core

mission. As resources are devoted to make-work procedural black holes, the mission decays and collapses at the first crisis.

Stop me if you've heard this before: contacting essential services (tax payments, etc.) rarely generates a timely

reply, much less a solution; a new bridge or subway line takes decades to build and is billions over budget;

software projects intended to streamline complex regulatory processes (building permits, etc.) never work right

and end up slowing the whole system down, fraud is rampant, software security is laughably poor....the list is almost

endless.

5. Once the system has been stripped of resources, experienced staff, back-up equipment and supplies and loaded

with unproductive friction, even a small crisis will bring down the entire system. In the graphic below, all

of these resources are the buffer that enables systems to respond to the pressing demands of crises. Once these are

gone, the only possible result is systemic collapse.

6. We've collectively lost the ability and willingness to deal with crises for which there is no happy-story

ending. We only want to hear the optimistic story, the glimmers of hope, the miracle cures, the painless

tech fix, etc., and if we get a dose of reality instead, we're quick to dismiss the bearer of inconvenient news

as an alarmist, a doom-and-gloomer, etc.

In other words, our economy and society have been optimized for failure. Drifting along in a daze of

disconnected-from-reality complacency we are completely unprepared to deal with realities that don't respond to

magical thinking, optimism, hope and tech fantasies.

My new book is now available at a 20% discount this month:

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States (Kindle $8.95, print $20)

If you found value in this content, please join me in seeking solutions by

becoming

a $1/month patron of my work via patreon.com.

Recent Videos/Podcasts:

The Central Bank System Has Failed, It's Time To Redraw America’s Grand Strategy (39 min)

Jay Taylor and I discuss why Inflation is a Runaway Freight Train (21 minutes)

A Grand Strategy to Address the Global Crisis (54 min., with Richard Bonugli)

XI's GAMBIT: A Bridge Too Far? (41 min, with Gordon Long)

My recent books:

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

(Kindle $9.95, print $25)

Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic

($5 Kindle, $10 print, (

audiobook):

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake

$1.29 Kindle, $8.95 print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print)

Read the first section for free

Become

a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Chris R. ($25), for your much-appreciated generous contribution to this site -- I am greatly honored by your support and readership. |

Thank you, Michael M. ($50), for your splendidly generous contribution to this site -- I am greatly honored by your steadfast support and readership. |

|

|

Thank you, Bryan J. ($5/month), for your monumentally generous pledge to this site -- I am greatly honored by your support and readership. |

Thank you, James A. ($50), for your awesomely generous contribution to this site -- I am greatly honored by your steadfast support and readership. |