Rather than attempt to evade Caesar's reach, a better strategy might be to 'go gray': blend in, appear average.

Let's start by stipulating that I don't "like" this forecast. I'm not "talking my book" (for example, promoting nuclear power because I own shares in a uranium mine) or issuing this forecast because I favor it. I simply see it as the most likely trajectory of the global financial system, based on history and the dynamics of human systems. "Liking" it or not liking it has nothing to do with it: the opinions of Titanic passengers who didn't "like" that the ship was sinking didn't affect the outcome.

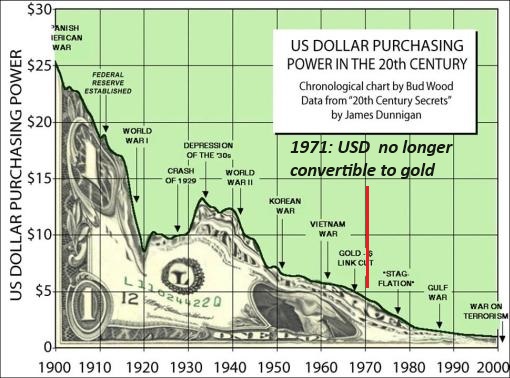

You already know the global financial system is untenable. In a nutshell, the expansion of production and consumption has been funded by the expansion of credit--money borrowed from future resources and income. The rate of expanding debt far surpasses the anemic rates of expanding production, and this rapidly expanding mountain of debt is perched precariously on the phantom collateral generated by The Everything Bubble, the astounding expansion of asset prices as those with the lowest cost access to credit have bid up every asset class, from real estate to gold to bitcoin to stocks to fine art.

All these assets are phantom collateral because they were bid up on the wings of cheap, abundant credit. History is rather decisive: all credit-asset bubbles pop, and the price of the assets round-trips back to pre-bubble valuations. As the bubble pops, credit shifts from being abundant and near-zero in cost to being scarce and dear.

The commercial real estate sector (CRE) is a real-time example of this dynamic. Half-empty buildings are being dumped at a fraction of their peak valuations, and then sold again for even less or abandoned to default and liquidation. This is how all bubbles pop; there is no other template supported by history. Humans cling to magical thinking and grasp at straws rather than face the unwelcome reality that the cycle has turned and there is no happy ending for those who believe the "real value" of an asset is the peak price at the top of the bubble.

Now that we understand the impossibility of keeping The Everything Bubble forever inflated, let's shift our attention to those tasked with keeping the system from collapsing. In my view, the closest analogy is police officers tasked with protecting the often ungrateful and undeserving while being plagued by do-gooders and naysayers who are safely isolated from the wretchedness they demand the cops deal with in a manner that meets with their refined approval.

In other words, us and them: only those who share the responsibility for protecting the often ungrateful and undeserving while being plagued by do-gooders and naysayers can understand. Outsiders know little of the realities and are often naive, basing their convictions on what they think "should happen" rather than the limitations of real life.

This will be the mindset of the authorities tasked with "saving" the system we all depend on--especially the wealthiest who have benefited the most. These is of course the class that feels most entitled to advocate for special treatment: we're rich and important, so you should listen to us and do what works for us.

In other words, like the do-gooders, naysayers and whiners telling the cops how to do their jobs. Those tasked with saving a system sliding toward an inevitable crisis will have little patience for obstructionists, however well-meaning. The attitude of those carrying the responsibility for saving the system will be: do your part, get out of the way, stop whining and be grateful we're saving the system for your benefit.

Let's now shift to a very common belief of "investors": foreseeing this crisis, we've piled up "hard money" assets that are safely hidden from the grubby, illegitimate grasp of authorities. When the crisis sweeps away the bubble, we'll still be rich, and we'll then scoop up all the bargain-priced assets, making ourselves even richer.

It gives me no pleasure to say the obvious: please don't be naive. Those who will be trying to save the system from collapse understand that every asset is only richly valued now because of the credit bubble. From their point of view, "investors" who are planning to preserve the bubble-valuation of their assets and then emerge to snap up everything for pennies on the dollar are, well, the enemy.

Another widespread belief holds that the hyper-wealthy always sneak through the wormhole and emerge with all their goodies intact. This fosters the idea that if they can do it, so can I. History offers examples on both sides: the great estates of the wealthiest Romans did not survive intact when the empire crumbled (or put another way, when control of the shards shifted to a new elite).

As the bottom 99.5% feel the squeeze, their rage at those at the top not paying their fair share will rise exponentially, and the political pressure on authorities to go after the hyper-wealthy will become too intense to ignore. Many of those trying to save the system will have already had enough of coddled billionaires, bankers and financier grifters.

Another conviction that will be revealed as naive is the faith that the rules will stay unchanged, allowing us to hoard our stash and emerge unscathed to scoop up the bargains offered by the less prescient. History is again rather definitive: the rules will change overnight, and continue changing, as needed. One "emergency measure" after another will be imposed and become normalized.

It's important to put ourselves in the shoes of those struggling with the impossible responsibility of keeping the system from collapsing. From their point of view, everyone trying to evade the wealth taxes, windfall taxes, special assessments, etc. are ungrateful whiners, as what will anyone have if the system collapses? We're doing you all a favor, taking only 10% in a wealth tax to preserve the 90% that remains yours.

Another point of naivete is what happens to obstructionists in a full-spectrum surveillance Corporate-state. China has shown other nation-states how to do it properly: every digital communication and transaction is monitored, and while VPNs and other gimmicks offer a few wormholes, the fundamental reality is: it takes an awful lot of effort to not leave a trail of crumbs, and at some point, is it worth all the effort? It's much easier to just pay the wealth tax, the windfall tax, grumble about it, and move on to enjoy life as best we can.

In China, the local authorities politely invite transgressors to tea, and offer a suggestion to mend your ways and keep your nose clean. Those who insist on mucking up the works after the kindly advice will be neutered one way or another.

The naivete also extends to ways to evade surveillance. We're all going to get by on barter. Really? Have you actually tried to exchange stuff with anonymous others? Like many encounters in online boards, people don't show up, they flake out or decide not to make the deal. It's tediously time-consuming and frustrating unless you already have a network of trusted contacts who do this kind of thing all the time.

In my experience, reciprocity with other trustworthy productive people works better than barter. Instead of haggling over price/value, just give stuff away. In a trusted network, whomever gets the free stuff will scrounge up something to give you for free in return. These networks tend to have a "node," an outgoing, friendly, trustworthy person who can find a welcoming home for whatever is being freely distributed, and pass around what's being given to those who gave freely of their surplus.

Another point of naivete is the belief that as an asset soars in value, the authorities will magically restrain themselves from noticing this juicy target. If we factor in history and human nature, we will conclude the opposite is more likely: the authorities will redouble their efforts to track and collect that which is Caesar's from those trying to evade the collection of everyone's "fair share."

Given the resources of the NSA et al., how plausible is it to think little old me is going to leave no digital crumbs as I go on my merry way? Thanks to automation of data scraping, it's going to get easier and cheaper to scrape data looking for miscreants trying to avoid paying "their fair share."

The whole idea of a wealth tax is it's a tax on all wealth, held anywhere in the world. So burying assets offshore only works as long as the authorities turn a blind eye to tax havens. As pressures mount, trusting the eyes to remain blind might not be as "sure-thing" as many seem to believe.

As specific assets soar in value, a "windfall tax" will become politically appealing. Since all this soaring wealth is unearned, shouldn't the fortunate owners pay a bit more due to the windfall nature of their unearned wealth? Of course they should.

The key point to understand is the system will have to grab enough collateral to fund itself while collateral evaporates in the deflation of the Everything Bubble. This will truly be a case of TINA--there is no alternative. Desperation will drive policy extremes few think of as possible, much less inevitable.

Something else that may be revealed as naive is the faith that moving to another nation-state will offer secure respite from those demanding we render unto Caesar that which is Caesar's. This faith overlooks the global reach of these dynamics: rampant inflation, the debasement of currency, the increasingly desperate need for collateral and revenue to keep the system from imploding, the rising cost of risk and credit, the scarcity of collateral, and so on. How will the nation-state we're moving to respond to these financial crises? What are the odds that they will magically escape the crisis, or come up with a painless solution that doesn't demand any sacrifices of residents? How secure will the rule of law and the wealth of foreigners be once push comes to shove?

In summary: to understand the next 8 to 10 years, start by having some sympathy for the fox and not just for the hare. Here we are, trying to save the system that everyone depends on, taking a modest 10% wealth tax, and the ungrateful wretches are whining and trying to evade paying their fair share.

Rather than attempt to evade Caesar's reach, a better strategy might be to go gray: blend in, look average: post photos of kittens and puppies, complain about the cost of groceries, drive a look-alike vehicle, live in an unremarkable house, render unto Caesar that which is Caesar's, forget about emerging as one of the rich who evaded Caesar and get on with enjoying one's private life focused on well-being, and as difficult as it may be, work up a little gratitude for those carrying the responsibility for keeping the system from collapsing. A system that degrades but coheres is a far better place to live than a system that completely collapses.

It gives me no joy to suggest please don't be naive, but a realistic appraisal of what happens when things unravel suggests there are few limits on "emergency measures" anywhere on the planet and it's best to plan accordingly and focus on what we can control rather than what we can't control.

For more on this approach, here are free excerpts of my book on self-reliance.

My recent books:

Disclosure: As an Amazon Associate I earn from qualifying purchases originated via links to Amazon products on this site.

Self-Reliance in the 21st Century print $18,

(Kindle $8.95,

audiobook $13.08 (96 pages, 2022)

Read the first chapter for free (PDF)

The Asian Heroine Who Seduced Me

(Novel) print $10.95,

Kindle $6.95

Read an excerpt for free (PDF)

When You Can't Go On: Burnout, Reckoning and Renewal

$18 print, $8.95 Kindle ebook;

audiobook

Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

(Kindle $9.95, print $24, audiobook)

Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel)

$4.95 Kindle, $10.95 print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print)

Read the first section for free

Become

a $3/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Chao Goblin ($50), for your magnificantly generous subscription

to this site -- I am greatly honored by your support and readership.

|

|

Thank you, Wa W. ($5/month), for your marvelously generous subscription

to this site -- I am greatly honored by your support and readership.

|

|

Thank you, BL T. ($50), for your splendidly generous subscription

to this site -- I am greatly honored by your support and readership.

|

|

Thank you, Michael J. ($50), for your superbly generous subscription

to this site -- I am greatly honored by your support and readership.

|

Read more...