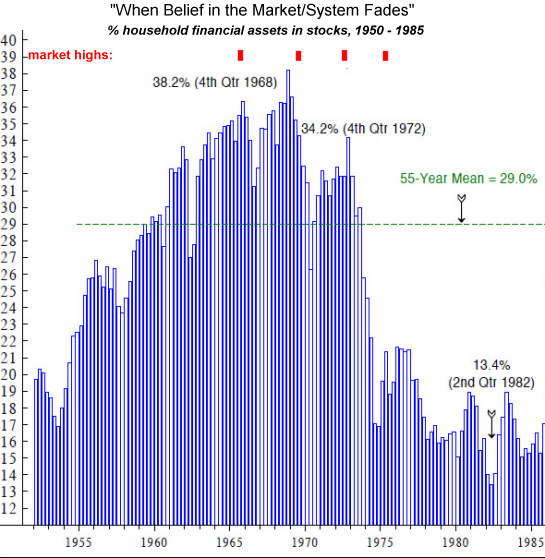

Rome Was Eternal, Until It Wasn't: Imperial Analogs of Decay

The tricky part is distinguishing the critical dependencies--those resources the empire literally cannot do without--from longer-term sources of decay and decline.

In response to my recent post

What If There Are No Analogs for 2024?, an astute reader nominated the Roman Empire as a fitting analog. Longtime readers know I've often discussed the complex history of Western Rome's decay and collapse, for example, Why Rome Collapsed: Lessons For the Present (August 11, 2023).

Dozens of other posts on the topic stretch back to 2009:

Complacency and The Will To Radical Reform (February 12, 2009)

What conclusions can we draw from recent research and the voluminous work done by previous generations of historians? Our first conclusion is simply to state the obvious: it's complicated. There was no one cause of Western Rome's decay and collapse. A multitude of factors generated feedback loops and responses over hundreds of years, some more successful than others.

Indeed, we cannot help but be struck by how many times impending collapse was staved off by brilliant leadership and policy adjustments.

Our second conclusion is to distinguish between the erosive forces of decay and critical vulnerabilities that can trigger collapse. Many authors have pointed to moral decay and fiscal over-reach as sources of Rome's eventual fall, but there were far more pressing dependencies that created potentially fatal vulnerabilities.

In the case of Western Rome, these included:

1. The depletion of the silver mines in Spain (and the eventual loss of Spain to the Visigoths). Once you run out of hard currency, your free-spending days are over. This dependence on large quantities of hard currency to fund your armed forces is a trigger for collapse.

2. Dependence on revenues from foreign trade with India, Africa and central Asia. Western Rome's income was highly asymmetric, depending heavily on import duties from foreign trade funneling through the Red Sea and the Roman ports in Egypt. Many of Rome's far-flung provinces were net drains on the imperial coffers; rather than generate income, they were costs.

3. Military defeats. In his recent book

The fall of the Roman Empire: a new history of Rome and the Barbarians,

historian Peter Heather persuasively argues that the Roman Empire was neither on the brink of social or moral collapse, nor fatally weakened by resource depletion. What brought it to an end were the Barbarian invasions from what is now Germany and Eastern Europe, mass tribal movements triggered by the Huns pushing into Europe from the east.

Heather argues Rome's great success eventually led to its undoing, as the small, loosely organized Barbarian tribes learned from the Romans how to form larger, more cohesive and thus more powerful social and military organizations.

We must also note Rome's many defeats at the hands of Attila the Hun. It is not coincidence that Attila died in 453 AD and the Western Roman Empire expired in 476 AD, unable to recover from the losses incurred by the Huns, Visigoths and Vandals.

4. Dependence on wheat from North Africa. Rome depended entirely on the bread-basket of North Africa to feed its populace. Once the Vandals swept through Spain and conquered North Africa, cutting off Rome's supply of wheat, the empire was doomed.

5. Incompetent leadership. Western Rome--and every empire, if we look closely--was critically dependent on competent leadership when faced with existential threats to the Empire's cohesion. We can cite Marcus Aurelius and Constantine as two examples of many.

When the leadership was weak and/or incompetent, defeats and failures piled up and things fell apart.

We must also note the role of the great tidal forces of demographics, disease, climate change, regional rivalries and cultural sclerosis in weakening the empire's ability to respond to polycrisis. The rise of the Barbarian tribes led to Rome's successful melding of diplomacy, bribes and military victories, a strategy mirrored by the Han Dynasty in China at the same time.

(I'll have more to say on the Han Dynasty this weekend for my subscribers.)

Rome successfully Romanized the Barbarian tribes, but made the critical cultural error of dismissing this new cohort of productive Roman citizenry as second-class. Romans who happened to have been born in Gaul (France) or Germany eventually chafed at these institutional biases, and this contributed to their eventual replacement of Italian leadership and its centralized control.

Indeed, the Roman Empire did not disappear in 476 AD as much as break apart into Barbarian-led pieces of what they reckoned was a continuation of the Imperial era. This complex history is ably addressed in the remarkable volume The Inheritance of Rome: Illuminating the Dark Ages 400-1000.

In some ways, the Catholic Church replaced the political-military empire as a centralized authority in western Europe. In the Eastern Roman Empire (the Byzantine Empire) that continued on for another thousand years, the Orthodox Church played a central role in its coherence.

The Antonine Plague of 165 to 180 AD weakened the empire. Generally ascribed to smallpox, the plague killed millions and decimated the Roman military. Rome recovered, but arguably never quite to the same level.

Empires tend to do just fine until climate change disrupts their agriculture and water supplies. Climate change--cooling weather across the prime agricultural regions--weakened both Rome and the Han Dynasty. Historian Kyle Harper describes the gradual and eventually consequential changes in his book The Fate of Rome: Climate, Disease, and the End of an Empire.

The centuries-long rivalry with the Persian Empire also drained the Empire of resources, even as new challenges from Barbarians and Huns demanded increasing military expenditures.

We would be remiss not to include the internal decay wrought by clinging to the alluring fantasy that past success guarantees future success, without any nasty sacrifices by the ruling elites. Historian Michael Grant addressed this in his book

The Fall of the Roman Empire:

"Enmeshed in classical history, all he can do is lapse into vague sermonizing, telling the Romans, as many a moralist had told them throughout the centuries, that they must undergo an ethical regeneration and return to the simplicities and self-sacrifices of their ancestors.

There was no room at all, in these ways of thinking, for the novel, apocalyptic situation which had now arisen, a situation which needed solutions as radical as itself. His whole attitude is a complacent acceptance of things as they are, without a single new idea.

This acceptance was accompanied by greatly excessive optimism about the present and future. Even when the end was only sixty years away, and the Empire was already crumbling fast, Rutilius continued to address the spirit of Rome with the same supreme assurance.

This blind adherence to the ideas of the past ranks high among the principal causes of the downfall of Rome. If you were sufficiently lulled by these traditional fictions, there was no call to take any practical first-aid measures at all."

Roman elites in Gaul were still writing letters to one another complaining of the breakdown of everyday life right up until the system collapsed. Their letters complaining of the collapse were never delivered, it seems. Their estates continued to exist for a time at the behest of their new Barbarian overlords, but power shifted away from old elites to new elites.

Lastly, let us note how cycles tend to impact empires. Systems arise due to their superior performance, reach their limits and then become obsolete as new selective pressures are met with half-measures and doing more of what's failed.

There are many Imperial Analogs of Decay. The tricky part is distinguishing the critical dependencies--those resources the empire literally cannot do without--from longer-term sources of decay and decline.

Here is a short list of recommended reading on these topics.

The History of the Decline and Fall of the Roman Empire (abridged)

How Rome Fell: Death of a Superpower

War and Peace and War: The Rise and Fall of Empires

The Great Wave: Price Revolutions and the Rhythm of History

The Upside of Down: Catastrophe, Creativity and the Renewal of Civilization

The Grand Strategy of the Roman Empire: From the First Century CE to the Third

The Roman Empire and the Indian Ocean: Rome's Dealings with the Ancient Kingdoms of India, Africa and Arabia

End Times: Elites, Counter-Elites, and the Path of Political Disintegration

The Collapse of Complex Societies

Overshoot: The Ecological Basis of Revolutionary Change

My new book is now available at a 10% discount ($8.95 ebook, $18 print):

Self-Reliance in the 21st Century.

My new book is now available at a 10% discount ($8.95 ebook, $18 print):

Self-Reliance in the 21st Century.

Read the first chapter for free (PDF)

Read excerpts of all three chapters

Podcast with Richard Bonugli: Self Reliance in the 21st Century (43 min)

My recent books:

Disclosure: As an Amazon Associate I earn from qualifying purchases originated via links to Amazon products on this site.

The Asian Heroine Who Seduced Me

(Novel) print $10.95,

Kindle $6.95

Read an excerpt for free (PDF)

When You Can't Go On: Burnout, Reckoning and Renewal

$18 print, $8.95 Kindle ebook;

audiobook

Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

(Kindle $9.95, print $24, audiobook)

Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel)

$4.95 Kindle, $10.95 print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print)

Read the first section for free

Become

a $1/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Jose S. ($200), for your beyond-outrageously generous contribution to this site -- I am greatly honored by your steadfast support and readership. |

Thank you, Mark S.C. ($50), for your monstrously generous contribution to this site -- I am greatly honored by your steadfast support and readership. |

|

|

Thank you, Colin G. ($50), for your fantastically generous contribution to this site -- I am greatly honored by your steadfast support and readership. |

Thank you, Duane S. ($25), for your superbly generous contribution to this site -- I am greatly honored by your steadfast support and readership. |