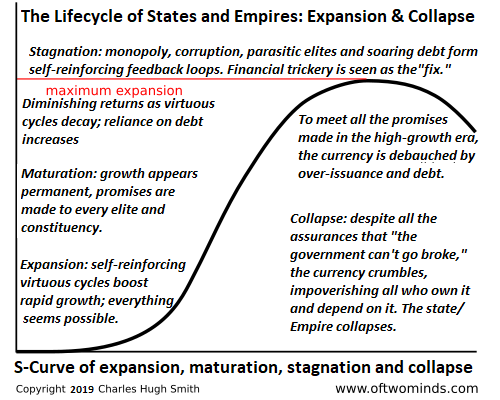

The sooner we start preparing for degrowth, the better off we'll be.

A Chinese proverb captures this succinctly: By the time you're thirsty, it's too late to dig a well.

Let's consider livelihood options in an unsustainable economy of extremes that are unraveling, an economy

that is being forced to transition to Degrowth.

Nassim Taleb's book Antifragile explains the differences between fragile systems

(systems that cannot survive instability), resilient systems (systems that can survive

instability and stay the same) and antifragile systems (systems that adapt and emerge stronger).

The ideal way of life is antifragile: resilient enough to survive adversity and adaptable enough to evolve solutions to whatever comes our way.

The key antifragile traits are adaptability and rapid, flexible evolution. Adversity puts selective pressure on organisms: only those organisms which adapt successfully survive.

The more antifragile our livelihood and way of life, the better prepared we will be to recognize and pursue opportunities.

An unsustainable, unstable economy puts a great deal of pressure on its participants. Only those with the skills and agency to move, adapt and experiment will emerge stronger.

Adaptability requires agency. Those without much control are stuck with the consequences of others’ decisions and actions.

In my experience, self-reliance is integral to an antifragile way of life. Self-reliance and self-sufficiency are similar but not identical.

Self-sufficiency means reducing our dependence on resources provided by others: growing our own food, doing our own repairs, etc. Self-sufficiency can also be understood as shortening dependency chains.

Compare being dependent on food shipped thousands of miles to relying mostly on food grown within 50 miles of home. There are so many ways long supply chains can break down because the entire system breaks down if even one link in the dependency chain breaks.

Total self-sufficiency isn’t practical. We all rely on industrial production of metals, tools, plastics, fertilizers, etc. But reducing our dependence on systems that are fragile by consuming less and wasting nothing increases our antifragility.

Self-reliance is being able to take care of oneself, being independent in thought and action, and maintaining control

of decision-making--what I’ve been calling agency.

Self-reliance means being able to go against the crowd. This requires independence and confidence in one’s inner compass.

Being able to take care of oneself means drawing upon inner resources, being able to identify the essentials of a situation and coming up with solutions that are within reach.

Since households with multiple incomes are far more resilient than households with all their eggs in one basket, our goal is to develop income streams that we control. The ownership is more important than the scale of the income. A modest income we control is far more antifragile than a larger income we have little control over.

Developing income streams is easier if we approach the task with an entrepreneurial mindset.

This mindset looks at work in terms of markets, unmet demand, pricing power, networks of trustworthy peers, trial

and error (experiments), optimizing new skills, seeking mentors, learning to make clear-eyed assessments of what’s

working and what isn’t, and then acting decisively on the conclusions.

All these skills can be developed. They are very useful in navigating unstable conditions because they prepare us to act decisively rather than passively await others to decide what happens to us.

Some skills can be applied to virtually every field: project management, bookkeeping, working well with others, computer skills and communicating clearly. Being a fast learner is valuable in every field.

In my books and blog posts, I've covered the difference between tradable work--work that can be done anywhere--and untradable work, work that can only be done locally. Having skills that are untradable is advantageous, as the competition is local rather than global.

Skills that can't be automated are also advantageous. Robots are optimized for repetitive tasks and factory / warehouse floors with sensors. They are not optimized for tasks that must be figured out on the fly and that require multiple skills.

Who fixes the robot when it fails out in the field? Another robot? Who replaces the dead battery in the drone? Another drone? The point is there are real-world limits on robotics, artificial intelligence, machine learning and automation that proponents gloss over or ignore.

Those with multiple skills who can problem-solve on the fly will continue to be valuable.

The models of work are changing, and this offers a wider range of options which is especially valuable to those emerging from burnout.

Combining various kinds and modes of work is called hybrid work. This could be mixing work from home (remote work) with occasional visits to an office, or it could be mixing a part-time job with self-employment.

I’ve written about one example in Japan called Half Farmer, Half X, where young urban knowledge workers move to the countryside to pursue small-scale farming while keeping a part-time, high-pay tech job they do online. Since the cost of living is so much lower in the countryside, these hybrid workers don’t need to work many hours remotely to cover their expenses, nor do they need their small-scale farming to be highly profitable.

Not all work is paid. Indeed, only a slice of human work globally is paid. The work that gives us the greatest fulfillment may well be unpaid or poorly paid. We may have to do some work to pay the bills while looking forward to the work we do that doesn’t earn much money.

Personally, I have always been drawn to both knowledge work and hands-on work. I worked my way through my university with a part-time job in construction. This was the ideal mix for my enthusiasms. Whenever I’ve been limited to one or the other, I feel dissatisfied. For me, hybrid work means having both knowledge work and hands-on physical labor, and having control of both.

Many people believe they need additional credentials to expand their opportunities. The alternative is to

accredit yourself.

Since I’m enthusiastic about working with fruit trees and vegetable gardens, let’s say I decide to offer my services to potential customers.

One avenue is to spend money and time to get a certificate in horticulture. Alternatively, I could take photos of my own yard to document the trees I planted and how fast they’ve grown under my care. In other words, I could accredit myself, providing direct evidence of my skills and experience.

Employers have learned that completing a credential doesn't mean the graduate will be productive. The diploma doesn’t prove the graduate learned much or has what it takes to work well with others.

The diploma actually tells us very little about the graduate. We learn much more from someone who accredits themselves by documenting projects they’ve completed.

The only real source of prosperity is improving productivity: doing more with fewer resources and labor. Economists expected the adoption of computers and the Internet to boost productivity. Instead, productivity gains have been extremely modest, 1% or 2% per year, far lower than the 10% annual gains achieved during industrialization.

This productivity paradox has puzzled economists for decades. One reason why the productivity of knowledge work ((white-collar work) has barely improved when compared to factory productivity (blue-collar work) is the methodical optimization of tasks is more difficult to apply to knowledge work. Much of this work is done by rule of thumb and what was passed down by senior workers.

There are a number of reasons for this. One is it’s easier to study the assembly of products than it is to break down the production of services.

Another is that many fields of knowledge work are so new that it’s difficult to optimize tasks because they’re constantly changing.

A third factor is that we’ve been wealthy enough to waste labor and capital on unproductive bureaucratic friction. Just as we waste water when it’s abundant and free, we also waste energy and money when they’re abundant.

In Global Crisis, National Renewal I describe the changes in the process of obtaining a building permit in the past 40 years.

In the early 1980s, I could submit a set of plans for a modest house in the morning and pick up the approved plans and building permit that afternoon. Now the process takes many months, even though the house being built hasn’t changed much at all. What changed was the permit approval process became terribly inefficient.

Since there’s few incentives to improve efficiencies in bureaucracies, it now takes a decade or longer to approve a bridge or landfill While the number of professors and doctors has increased modestly, the number of university and hospital administrators has soared.

Now that energy will no longer be cheap over the long term, incentives to improve the productivity of knowledge work will increase.

Unsustainable economies are prone to sudden changes in finance and the availability of essentials. We're accustomed to predictable stability, and so few are prepared to respond effectively to instability.

If our lives only work when things are stable, our way of life is fragile. Recall Sun Tzu’s advice: "If a battle cannot be won, do not fight it." If we’re only prepared for everything to stay the same, we’re fighting a battle we can’t win. We want to be prepared for sudden changes and scarcities by planning ahead and being flexible, nimble and responsive.

One facet of being antifragile is having a buffer or cushion against sudden shocks. In a 2018 interview, Nassim Taleb said, “Money can’t buy happiness, but the absence of money can cause unhappiness. Money buys freedom… to choose what you want to do professionally.”

Taleb went on to note that it takes great discipline to keep enough money stashed to give us the freedom to maintain our agency when faced with adversity. Self-reliance requires a buffer so we have time to figure out solutions and the means to pursue them.

In my experience, our willingness to consider all options, our ability to make careful decisions and take

decisive action are just as important as a cushion of cash. Cash widens our options, but if we’re frozen by

inexperience and fear then our options are severely limited.

The wider our range of skills, the greater our opportunities to add value. The basic needs of human life must be met and so those who can meet those needs will always be valued. This range of skills is also a buffer because it gives us more options in adversity.

How much money do we need as a cushion? The less we need, the lighter our expenses and the more options we have. If we need $10,000 a month just to pay our basic expenses, that demands a large cushion. If we’ve simplified and downsized our way of life so $1,000 a month is enough to keep us going, our cushion can be much smaller.

In other words, frugality, self-reliance and simplicity are key parts of antifragility, for they lower the cost of freedom. Money can lose its value in crisis, but our buffer of skills and self-reliance cannot be taken from us or devalued by a global crisis.

One final consideration is timing. The sooner we start preparing for degrowth, the better off we'll be.

A Chinese proverb captures this succinctly: By the time you're thirsty, it's too late to dig a well.

Recent podcasts/videos:

The Big Problems And Crash Dynamics Of The Spring/Summer 2022 Housing Market Crisis, Simplified (1:08 hr)

My new book is now available at a 10% discount this month:

When You Can't Go On: Burnout, Reckoning and Renewal.

If you found value in this content, please join me in seeking solutions by

becoming

a $1/month patron of my work via patreon.com.

My recent books:

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

(Kindle $9.95, print $24, audiobook)

Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic

($5 Kindle, $10 print, (

audiobook):

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake

$1.29 Kindle, $8.95 print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print)

Read the first section for free

Become

a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Glenn H. ($5/month), for your splendidly generous pledge

to this site -- I am greatly honored by your support and readership.

|

|

Thank you, Ron G. ($50), for your marvelously generous contribution

to this site -- I am greatly honored by your steadfast support and readership.

|

Read more...