Not the 1970s or the 1920s: We're in Uncharted Territory

All of these similarities and differences are setting up a sea-change revaluation of capital, resources

and labor that will be on the same scale as the extraordinary transitions of the 1920s and 1970s.

The awakening of inflation after decades of slumber has triggered a flurry of comparisons to the 1970s

accompanied by a chorus of projections for 1970s-type stagflation, defined as inflation plus economic stagnation--

limited or negative growth and high unemployment.

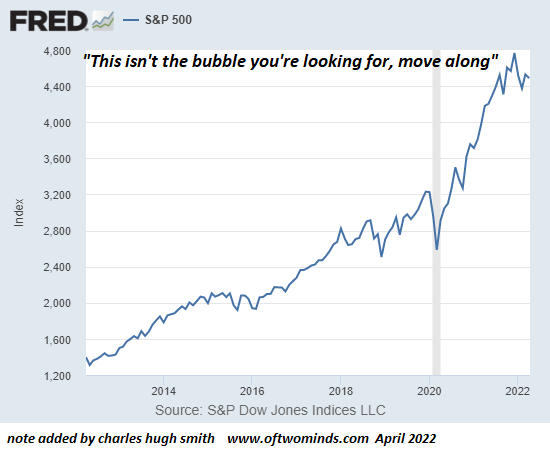

A less popular comparison is with the 1920s: a massive expansion of debt, an equally massive speculative bubble

in assets and extreme wealth-income inequality, all against a backdrop of slowing growth and debt saturation.

Each of these eras shares certain characteristics with the present, but beneath the surface there are

consequential systemic differences. Let's start with the 1970s.

The oil shock that fueled inflation had two sources: 1) the oil-exporting nations took control of their

hydrocarbon resources and repriced them in the context of 2) declining reserves and production in the West,

particularly the U.S., which had been the Saudi Arabia of the world through the 1930s, 40s and 50s.

A second, much less understood dynamic was the immense investment required to clean up the U.S. industrial

base. Pollution in the U.S. was out of control by the early 1970s, with toxic rivers catching fire and

high levels of air pollution. The oil shock prompted federal regulations on pollution and improvements in

the basic efficiency of appliances, vehicles, etc.

This was a major sea change for the entire industrial sector, and it required immense investments of capital

and a painful learning curve. This diversion of capital depressed profits and acted as an economy-wide tax on

the system. In today's money, the overall cost of this transition was in the trillions of dollars.

The debt levels in the 1970s were by today's standards absurdly modest. The cultural values of frugality

and avoidance of debt still held, and there was resistance to heavy public-private borrowing that has completely

vanished.

The demographics of the 1970s was also completely different from today. The 65-million strong Baby Boom

generation was entering the workforce and starting families and enterprises. The demographic double-whammy was

the mass entry of women into the workforce as opportunities and ambitions expanded.

Meanwhile, the energy picture was brightening under the radar as the development of newly discovered

super-giant oil fields in Alaska, the North Sea and Africa began. It took many years to bring these new

hydrocarbon sources online, but by the mid 1980s, the price of oil had fallen to lows that slashed the income

of oil exporting nations, including the Soviet Union.

None of these conditions are present today. Much of America's domestic production was offshored in the past 20 years,

the demographics are no longer as favorable (soaring population of elderly and flatlined workforce)

and the production from the super-giant fields brought online in the 1970s

is declining. There are no new super-giant fields in the global pipeline to replace those in the depletion phase

of declining production.

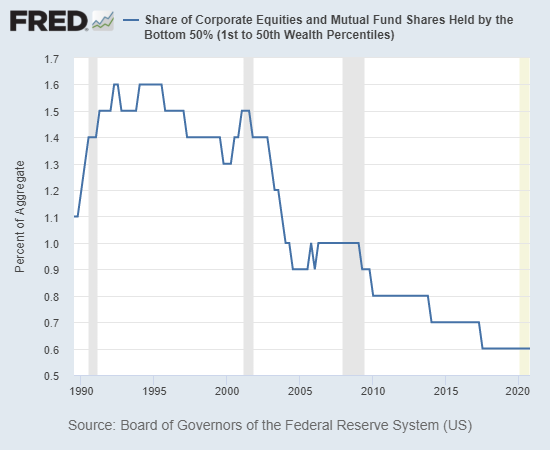

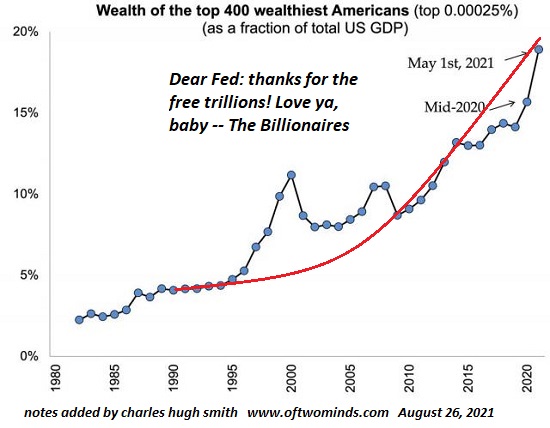

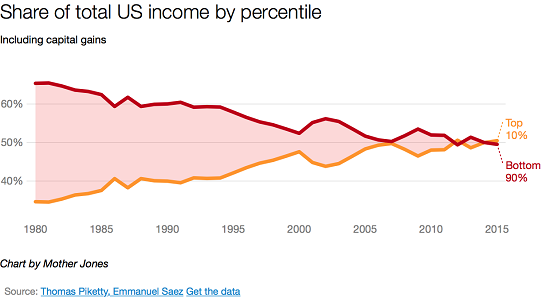

As for the 1920s: the parallels are debt saturation and speculative excess against a backdrop

of an economy that feasted on debt-fueled spending and speculation while absorbing new technologies.

The differences are the U.S. still had immense natural resources and relatively limited infrastructure in the 1920a.

While private debt was through the roof--$100 in a stock market account leveraged $900 in stock purchases

due to the 10% cash margin requirement--federal debt was still modest compared to modern levels.

This set the stage for massive expansions of federal debt in World War II that funded sustained investments in

infrastructure through the 1940s, 50s and 60s.

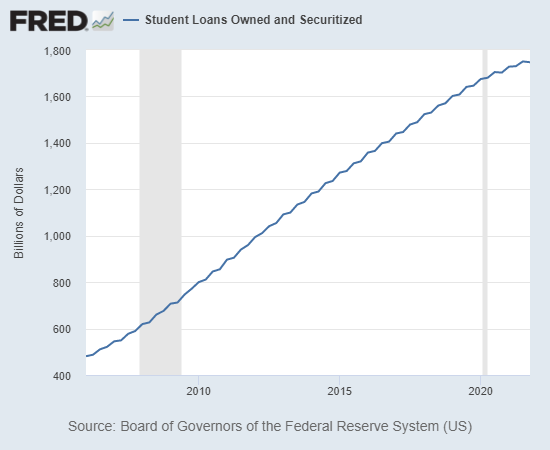

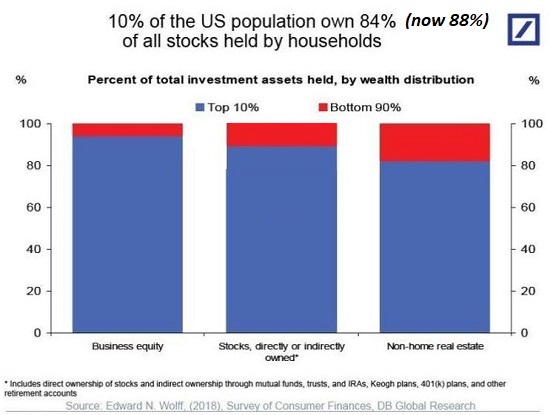

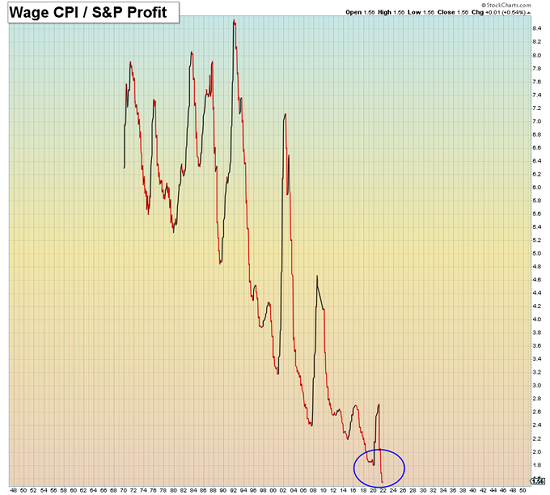

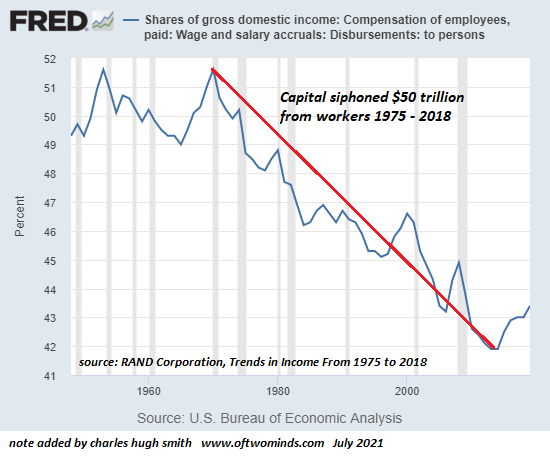

In the present, we have all the fragilities of the 1920s and few of the strengths. We have all the debt

saturation and speculative bubble excesses but our resources have been heavily tapped and every sector of the

economy is heavily indebted.

All of these similarities and differences are setting up a sea-change revaluation of capital, resources

and labor that will be on the same scale as the tumultuous transformations of the 1920s and 1970s.

We're in uncharted territory. More on these revaluations next week.

My new book is now available at a 10% discount this month:

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States (Kindle $8.95, print $20)

If you found value in this content, please join me in seeking solutions by

becoming

a $1/month patron of my work via patreon.com.

Recent Videos/Podcasts:

The Dam Has Cracked (37 minutes, with Gordon Long)

My recent books:

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

(Kindle $9.95, print $25, audiobook)

Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic

($5 Kindle, $10 print, (

audiobook):

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake

$1.29 Kindle, $8.95 print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print)

Read the first section for free

Become

a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Richard W. ($20), for your splendidly generous contribution to this site -- I am greatly honored by your support and readership. |

Thank you, Robert J. ($50), for your magnificently generous contribution to this site -- I am greatly honored by your support and readership. |