2019: The Three Trends That Matter

Look no further than Brexit in Britain, the yellow vests in France and the Deplorables in the U.S. for manifestations of a broken social contract and decaying social order.

Among the many trends currently in play, Gordon Long and I discuss three that will matter as 2019 progresses: 2019 Themes (56 minutes)

1. Final stages of the debt supercycle

2. Decay of the social order/social contract

3. Social controls: Surveillance capitalism, China's Social Credit system, social globalization

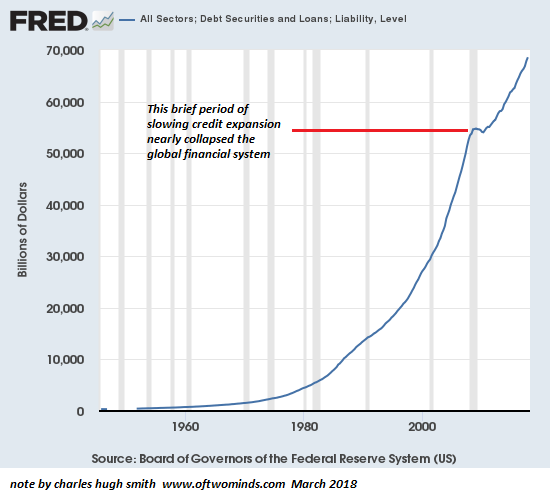

The basic idea of the debt supercycle is simple: resolving every crisis of over-leveraged speculative excess, evaporation of collateral and over-indebtedness by radically increasing debt eventually leads to an implosion of the entire credit-based financial system.

The final stages of the current debt supercycle are manifesting all sorts of interesting cross-currents: de-dollarization and the unprecedented expansion of debt in China to name just two.

De-dollarization describes the efforts of many nations to reduce their dependence on U.S. dollars for trade and reserves. Since the USD remains the largest reserve currency in both trade and reserves, this trend threatens to reorder the entire global financial system, with potentially disruptive consequences not just to the USD but to a variety of institutions and norms.

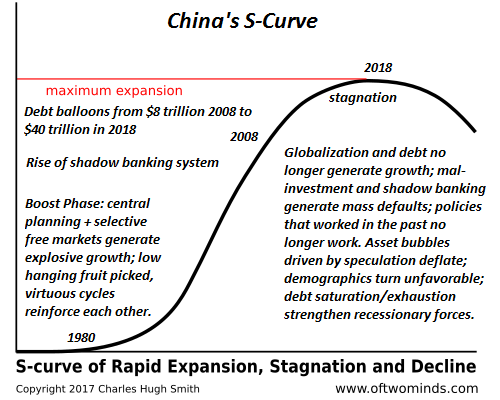

China's total systemic debt has soared from $7 trillion in 2008 to $40 trillion in 2018. This is of course only a rough estimate, as China's enormous Shadow Banking System is famously opaque, as are many of its institutional and corporate balance sheets.

China has embraced the narrative of "growing our way out of stagnation by quintupling debt," but the banquet of consequences of this speculative orgy is finally being served: China's dramatic slowdown in 2018 is just the appetizer course of the banquet of consequences.

This excerpt of a recent (and immediately censored) talk given by a Chinese economist illuminates the result of debt-fueled mal-investment and speculation on a grand scale:

Look at our profit structure. To put it plainly, China’s listed companies don’t really make money. Then who has taken the few profits made by China’s more than 3,000 listed companies? Two-thirds have been taken by the banking sector and real estate. The profits earned by 1,444 listed companies on the SME board and growth enterprise board are not even equal to one and half times the profit of the Industrial and Commercial Bank of China. How can this kind of stock market become a bull market?

When we buy stocks, we are buying the profits of the company, not hype and rumors. I recently read a report comparing the profits of China’s listed companies with those in the U.S. There are many U.S. public companies with tens of billions dollars in profits. How many Chinese tech and manufacturing companies are there that have accomplished this? There is only one, but it’s not listed, and you all know which one that is. [Xiang is referring to Huawei, the Chinese tech company.]

What does this tell us? As Yale professor Robert Shiller said: stock market performance may not work as a barometer of the economy in the short run, but it does for sure in the long run. So I think that the terrible stock performance only demonstrates one thing, which is that the real economy in China is in quite a mess. Where is the stock market rebound? I think it’s obvious that investor confidence has yet to recover."

Look no further than Brexit in Britain, the yellow vests in France and the Deplorables in the U.S. for manifestations of a broken social contract and decaying social order. The politically invisible / financially vulnerable have declared we're still here to their globalized elite aristocrats, and this rebellion against elite domination and profiteering is being demonized by the corporate-state media as populism rather than what it really is: a full-blown revolt of the working class.

In response, the ruling elites have instituted social controls via ramped up official propaganda, Social Credit Scoring in China and private-sector Surveillance Capitalism in the U.S.

All these forms of social control seek to marginalize, suppress and censor dissent, alternative sources of information, alternative narratives and financial independence: hence the sudden eltist interest in Universal Basic Income (UBI) and similar central-state dependency programs: nothing suppresses a working class revolt quite like free money for keeping quiet, passive and obedient.

But some sectors of the working class are not willing to accept the bribes; they're holding out for actual political power, and this is why the ruling elites of France have responded to the yellow vest movement with such savagery.

Gordon and I discuss these trends and much more in our podcast 2019 Themes(56 minutes).

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic ($6.95 ebook, $12 print): Read the first section for free in PDF format.

My new mystery The Adventures of the Consulting Philosopher: The Disappearance of Drake is a ridiculously affordable $1.29 (Kindle) or $8.95 (print); read the first chapters for free (PDF)

My book Money and Work Unchained is now $6.95 for the Kindle ebook and $15 for the print edition. Read the first section for free in PDF format.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Terrance J. ($60), for your stupendously generous contribution to this site -- I am greatly honored by your steadfast support and readership.

|

Thank you, Peter M. ($50), for your superlatively generous contribution to this site -- I am greatly honored by your steadfast support and readership.

|