Fear moves fast enough to get inside our OODA loop--observe, orient, decide, act--so we decide and act only after the damage has been done.

The dynamics discussed here have nothing to do with the headlines of the past few weeks or months, or with geopolitics or stock market gyrations. These dynamics have been at work for years or decades, and now the banquet of consequences is finally being served, and we each get a seat whether we want one or not.

In Hawaii, calabash uncle (or auntie) describes a friend who is so close to the family that he/she is like a family member. In many cases, the calabash uncle/aunt has spent far more time with the kids than the blood-relations uncles and aunts.

I am a calabash uncle to my old friend's two sons, having spent quality time with them from their infancy to their current age (mid-40s). I've shared vastly more time with them, together and as individuals, than their father's brother.

One of the sons is an entrepreneur who with his wife is busy raising two young daughters and expanding their enterprise. Recently, they bought a parcel of land in the Pacific Northwest near their current home with an old farmhouse that they consider their "dream homestead." They've already planted an impressively diverse "food forest" of trees, and are planning a complete renovation of the old farmhouse, parts of which were built in the 1800s.

All of this activity involves long-term leases of commercial space and home mortgages--major debt and lease commitments that are essentially equivalent to debt, as the lease must be paid regardless of how the business is doing.

The parents are actively engaged with their sons and their families, so my role is peripheral. But I do feel a responsibility to each family member, and I concluded that I would not be serving this son's best interests by remaining silent about what I see coming financially and economically, given the risks that accompany debt.

So I laid out the case to sell now to reduce or eliminate debt / obligations.

My point was the one essential strategy to survive a deep, prolonged recession is to act decisively before it's too late to sell--to get ahead of the crowd before they realize the economy they assumed was stable and risk-on is unraveling faster than they thought possible.

I was careful not to claim predictive powers. I couched it in these terms: "I'm not saying this is going to be right. What I'm saying is: if you see these things start happening, then those are solid reasons to expect a recession that's deeper and longer than most people think possible, and respond accordingly."

In other words: pay close attention to the key signals and don't get distracted by noise.

The key signals include the entire credit system: what's going on with lenders and borrowers, how risk is being distributed or masked, what's going on beneath the surface.

For example: this is not a sign of a healthy economy.

Record Numbers of Workers Are Raiding Their 401(k) Savings (wsj.com).

Investment funds cutting off redemptions / return of your capital is not a sign of a healthy financial system.

The noise is all the indicators that are easily gamed or inherently flawed: growth (GDP), inflation, unemployment, the stock market.

What's harder to game are bond yields and interest rates, because the price of these are "discovered" by the risk intrinsic to sinking cash into a risk asset (and every asset is a risk asset) or lending money. Once cash is sunk in an asset, the owner could lose money should the asset's market value drop. Once a loan has been originated, the lender could lose money of the borrower defaults.

I described these dynamics in recent posts:

Paging Nostradamus: You Have a Margin Call and

This Polycrisis Is Unique:

1. Recessions don't replicate the last recession; they tend to track the recessions before the last recession.

2. A unique confluence of long-term cycles and waves is occurring in 2026-27, which will generate consequences / second-order effects far beyond this two-year time frame.

Since I experienced the market declines / recessions of 1973-5, 1980-83, 1991-92, 2000-03 and 2008-09, and was actively exposed to the downsides as a self-employed / entrepreneur, I wanted to share what happens in a recession that few seem to highlight: the door slams shut faster than anyone thinks possible, due to the recency bias of "good times" and stable markets.

Here is how I described this dynamic:

"People are using debt to maintain their spending, and when they hit the wall, spending drops suddenly.

The same thing happens in real estate: the door suddenly slams shut. Sales plummet, lending tightens--nobody's buying because the economy is making them cautious."

I explained how those trying to sell their house get trapped by recency bias: they fail to lower their price to conditions as they are now (deteriorating fast), and then the door slams shut and they can only sell at fire-sale prices:

"It's human nature to think the highest recent price is 'the real value of my house,' but in a recession coupled with high interest rates, the only sales that close are those where the seller dropped their asking price a lot.

So the house was worth $850K in good times, and so the seller lowers their asking price to $825K. The only way to sell it is to get ahead of the trend and drop it to $775K or even $750K. The people who think prices will rebound end up being foreclosed or selling for $550K.

If this seems unreal, I followed markets very closely from 2005 on, and that's why my blog took off: I was being realistic because I'd lived through 1973-75 and 1980-83, and I saw how the door slams shut faster than anyone thinks possible.

Credit dries up, and that reduces spending and makes it very difficult to re-finance anything, no matter how good your credit."

I ended with this simple advice: sell now. Sell whatever it takes to liquidate debt, because it's harder for bad things to happen when you have no debt, and greed is a wonderful motivator but fear works much faster. (Put another way: fear moves fast enough to get inside our OODA loop--observe, orient, decide, act--so we decide and act only after the damage has been done.)

I shared the personal experiences that inform my context / orientation: "I was living on fumes in 1973-74 and only survived 1980-83 because I had no debt and a low-cost of living."

In summary: sell now because:

1. It's harder for bad things to happen when you have no debt.

2. Greed is a wonderful motivator but fear works much faster.

3. Fear moves fast enough to get inside our OODA loop--observe, orient, decide, act--so we decide and act only after the damage has been done.

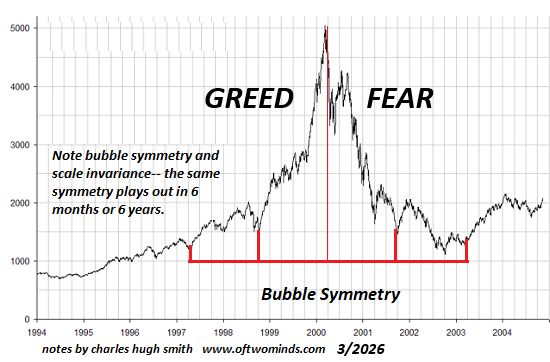

What happens in a recession / financial crisis is greed is quickly replaced by fear. This is one of our core survival instincts. That transition is the door slamming shut: everything that was possible in the risk-on euphoria of greed becomes impossible in the risk-off wilderness of fear.

My book Investing In Revolution is available at a 10% discount ($18 for the paperback, $24 for the hardcover and $8.95 for the ebook edition).

Introduction (free)

Check out my updated Books and Films.

Become

a $3/month patron of my work via patreon.com

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.

|

Thank you, John D. ($100), for your ourageously generous subscription

to this site -- I am greatly honored by your steadfast support and readership.

|

|

Thank you, David E. ($100), for your ourageously generous subscription

to this site -- I am greatly honored by your steadfast support and readership.

|

|

Thank you, Michael D. ($150) for your beyond-outrageously generous subscription

to this site -- I am greatly honored by your steadfast support and readership.

|

|

Thank you, Maury W. ($7/month) for your fantastically generous subscription

to this site -- I am greatly honored by your support and readership.

|