Lesson of the S-Curve: Doing More of What's Failed Will Fail Spectacularly

That nothing is truly "free" will be another lesson of the S-Curve.

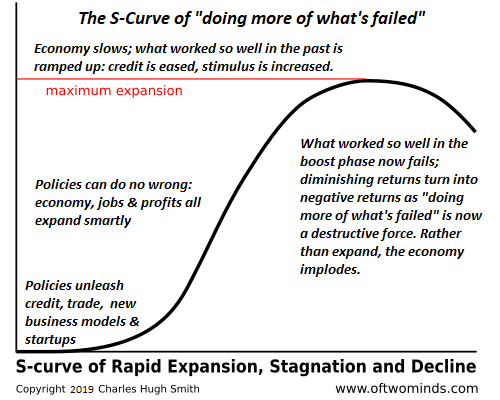

I often refer to the S-Curve because Nature so often tracks this curve of ignition, rapid expansion, stagnation and decline.

One lesson of the S-Curve is that the human bias to keep doing more of what worked so well in the past leads to doing more of what failed even as results turn negative.

The dynamic in play is diminishing returns: the yield on the policy that worked so splendidly at first diminishes with time.

Credit offers a cogent real-world example. When credit becomes available in a credit-starved economy, it generates a rapid, sustained expansion as credit-worthy borrowers borrow and spend on new productive capacity, consumer goods, housing, etc., all of which further drives expansion.

But once credit has saturated the entire economy, the only pool of borrowers left are uncreditworthy (i.e. at risk of default), and the only projects left unfunded by credit are laden with risk.

Either way, credit expansion stops: either lenders prudently refuse to issue credit to risky borrowers and ventures, and credit expansion grinds to a halt, or they foolishly lend money to borrowers and ventures which predictably default, triggering a credit crisis that brings imprudent lenders to their knees and triggers cascading defaults as declining asset prices push marginal borrowers into bankruptcy.

Doing more of what was successful in the boost phase of the S-Curve--expanding credit-- is now doing more of what's failed. Expanding credit in a credit-saturated economy only sets up cascading defaults.

The human response to the failure of what worked so well is disbelief: the problem, we reckon, is we didn't do enough the first time. So the answer to the failure of extending more credit is to extend even more credit and lower lending standards so anyone who can fog a mirror can get a loan.

At this point, diminishing returns become negative returns: doing more of what's failed is now not just unhelpful--it's actively destructive. Cramming more credit down the throats of risky borrowers and ventures guarantees a full-blown credit crisis when the defaults start taking down lenders and crushing asset prices that were dependent on credit expanding into eternity.

We are at the juncture where doing more of what's failed will push the economy into profound recession. Now that the economy is totally dependent on ever-expanding credit, there is no alternative (TINA) to expanding credit, no matter how destructive this expansion of bad credit will be in the near future.

It's no surprise that calls for free money (Universal Basic Income, UBI) are rising: the only real "solution" to soaring defaults is to give the borrowers free money to service their debt, or print trillions of dollars to pay off the soon-to-default debts.

That nothing is truly "free" will be another lesson of the S-Curve. The initial wave of free money will work wonders. Then diminishing returns will set in, and the response will be to jack up the printing and distribution of free money, i.e. do more of what's failed until the free money printing and distribution destroys the currency and the economy.

Thanks to the S-Curve, all this is clearly visible in the crystal ball.

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic ($6.95 ebook, $12 print, $13.08 audiobook): Read the first section for free in PDF format.

My new mystery The Adventures of the Consulting Philosopher: The Disappearance of Drake is a ridiculously affordable $1.29 (Kindle) or $8.95 (print); read the first chapters for free (PDF)

My book Money and Work Unchained is now $6.95 for the Kindle ebook and $15 for the print edition. Read the first section for free in PDF format.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com. New benefit for subscribers/patrons: a monthly Q&A where I respond to your questions/topics.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com. New benefit for subscribers/patrons: a monthly Q&A where I respond to your questions/topics.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Cooper K. ($10/month), for your outrageously generous subscription to this site-- I am greatly honored by your support and readership.

|