Either way AI goes--replacing human labor or failing to meet today's lofty expectations--the result is the same: an economic Depression.

Either way AI goes--replacing human labor en masse, or failing to meet today's lofty expectations--the result is the same: an economic Depression with no way out.

In effect, AI is self-liquidating: if it follows the projections of its most ardent promoters and replaces most human workers, it collapses the economy and society, and if it underperforms, it's an enormous waste of capital and resources that sinks the economy into Depression.

Let's break down each pathway to Depression.

To its promoters, AI is unstoppable and will generate super-abundance in whatever it creates for near-zero cost, and this abundance will effortlessly be shared with everyone because AI is super-productive.

Here is an example of this projection:

The Displacement of Cognitive Labor and What Comes After.

Ai agents will replace cognitive (i.e. creative / white-collar) labor, and AI-powered robots will replace manual labor, freeing humanity to find meaning not in work but other activities that replace work as the source of meaning.

What's striking about this projection is it doesn't mention the physical-world constraints of Growth At Any Cost / Waste Is Growth such as energy, fresh water, fertile soil, etc. We are left presuming AI will magically eliminate all such material constraints by means unknown but guaranteed to manifest because AI can solve anything--we're constantly assured it's already a super-intelligence.

This is the magical thinking at the heart of The Mythology of Progress: that all new technology is always positive, and every physical limit can be overcome by innovation / ingenuity, the only impediment to super-abundance is the naysayers.

The essay also doesn't present a plausible source of the trillions of dollars needed to fund Universal Basic Income (UBI) for everyone who no longer earns a living from work.

The common assumption here is that AI's productivity will automatically be profitable: since AI can grow all the food, it will be cheap. But if there is insufficient water and the soil has been depleted, AI will grow no more food than humans because the constraints are physical, not cognitive.

As for profitability, consider this comprehensive overview of the rapid advances in robotics / AI in China:

Inside China's robotics revolution: How close are we to the sci-fi vision of autonomous humanoid robots? I visited 11 companies in five Chinese cities to find out.

"As government subsidies flood the robotics sector, Chen and his peers are bracing for the usual pattern: price wars and cost cutting maneuvers that leave companies barely able to turn a profit."

In other words, as private capital and state funding pour money, resources and talent into the hot new sector, profitability vanishes: there's an oversupply of everything and a customer base that's too narrow to generate demand enormous enough to absorb all the products at prices that generate profits.

The idea that AI will generate trillions in "free wealth" that can then be distributed to the hundreds of millions of displaced workers in sufficient sums to enable a vast free-spending consumer class is not just unrealistic--it's a pipe dream.

Put another way: if displaced workers are getting barebones Universal Basic Income or equivalent--subsidized energy and food, etc.--then the number of people who will be able to buy a robot-assembled new vehicle or a household robot-servant will be far too limited to support a scale of production that offers economies of scale.

This is the Henry Ford insight: if workers (or displaced workers) have minimal incomes, they can't afford the products capitalism is producing.

Karl Marx viewed these dynamics--declining profits as capital expands and seeks a return while immiserating the workforce to reduce costs, reducing demand for expanding production--as self-liquidating: capitalism's core gearing collapses capitalist economies. It is ironic that Marx's description may finally reach fruition in the end-game of AI.

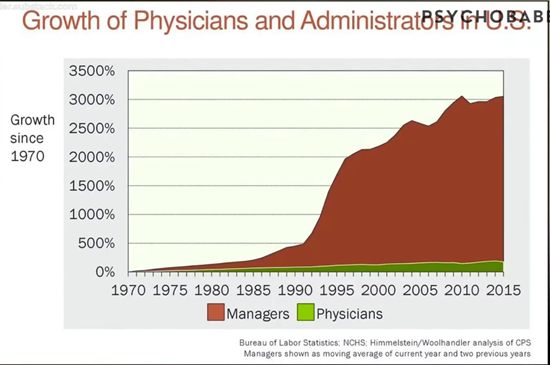

Another element that the AI promoters never dare mention is much of the "cognitive work" AI will do is what David Graeber memorably called BS Work--tasks without any real productive value, busy-work demanded by unproductive, complex organizations that reached this level of dysfunction as their initial modest cost structure transmogrified into bloated, extractive fiefdoms (higher education, healthcare, defense, etc.) whose share of the economy has soared as administrative costs (i.e. BS Work) generate make-work.

Consider this chart of healthcare employment (via J.F. MD). As Healthcare's share of the economy has soared from 5% to nearly 20%, the quantity of BS Work (administrative tasks) and the workforce to perform this work have also soared. (The chart of professors and university administrators is a close match for this: flatlined number of professors, monumental increases in administrative staff.)

Now the proponents of AI are salivating at the prospect of charging the same absurdly high fees while eliminating all those high-cost human physicians and technicians.

What about the immense bloat of administration? Of course AI will replace all those workers, too, and once again, the goal here isn't to reduce fees by 80% by replacing the current bloated, profiteering, complex system with a system that doesn't generate administrative BS Work; the goal is to eliminate 80% of the labor costs but keep charging the same high fees to boost the profits of the owners of the Healthcare industry, which I call Sickcare because it profits from illness and monopoly, not from health.

This is why AI is self-liquidating: the goal isn't to replace the dysfunctional, extractive monopoly-cartel structure of the economy: the goal is to maintain this structure as-is and increase its profitability by eliminating costly human labor.

The owners of AI tools are planning to reap billions in profit by selling their tools to corporations and governments intent on keeping the status quo asymmetries not just intact, but more profitable.

AI is the contrivance that the most grotesquely self-serving parts of our system are attracted to, as they want the immense profits to be reaped by reducing the bothersome expense of human workers.

There's another fundamental problem with the AI will deliver super-abundance to us all fantasy.

Despite enormous investment of capital and ingenuity, energy and materials that were once cheap (as measured by EROEI--energy return on energy invested) have become more expensive (as measured by EROEI) as the cheap-to-extract deposits have been depleted.

The Fracking Miracle is exhibit #1: even industry insiders are admitting that the limits of physics, chemistry and cost are weighing on fracking output. Like Nature, ingenuity and technology also have limits.

If engineering and materials had no limits, airliners would be flying 1,000 kilometers on a liter of fuel. The reality is advances are incremental and returns diminish.

Also unmentioned by the enthusiasts is the fact that AI itself has costs that can't fall to near-zero. So the idea that AI will magically generate near-zero cost goodies for everyone is fundamentally disconnected from reality.'

Boosting a thousand--oh, heck, make it a hundred thousand--data centers into orbit is inherently costly, even with reusable rockets.

As noted previously, an oversupply of robots and AI means profitability is near-zero, so where is the financial justification for the thousand orbiting data centers, or their replacements?

The last Great Myth of Progress that is dismissed with a wave of the "ingenuity" hand is the belief--or if you prefer, faith--that every technological revolution inevitably generates more and better jobs, as this is The Nature of Technological Revolutions.

This belief rests on recency bias: due to humanity's rapid exploitation of hydrocarbons and easy-to-extract minerals, human labor was replaced by energy slaves. The discovery of ever more deposits of hydrocarbons and minerals created a belief that resources are essentially limitless, if we just dig / drill deeper, build floating platforms at sea, etc. That all these "solutions" carry enormous costs is not mentioned, as "money" is abundant because we can create as much as we need.

It is not a Law of Nature that technology automatically creates more and better jobs. As agricultural labor was replaced by machines, the workforce was repurposed to operate machines in factories running on cheap hydrocarbons, and as more sophisticated machinery replaced human labor on assembly lines, the administrative, marketing, service, etc. industries trained workers to toil in cubicles--cognitive labor.

There is no industry that needs humans on the same scale as those being replaced by AI. "High touch" labor--waiters, caregivers, violin instructors--will all be replaced by robots / AI, too.

An elite may have the wealth to hire a human as a status signifier, but since the majority will be scraping by on UBI, the wealth needed to hire humans will be limited to an elite--an Tech-Financier oligarchy or nobility.

This pathway to Depression can be summarized as: AI is the last great hope of a system that's in the process of self-liquidating due to its disconnect from the reality that the physical and financial worlds have inherent limits that preclude infinite growth of consumption of material goods paid for with "money" borrowed into existence.

If AI fails to "save the system" by replacing workers and generating the vast wealth needed to support all the displaced workers, the system fails faster than it otherwise would have due to the staggering sum of capital and resources squandered on the chimerical AI Will Not Just Save Us, It Will Make Us All Rich techno-fantasy.

This alternative pathway to Depression is that AI underperforms due to intrinsic limits of its models. I mentioned six such factors in Why AI Malware (and Harmful Second Order Effects) Are Out of Control.

Here are two more of note:

Agents of Chaos

"Focusing on failures emerging from the integration of language models with autonomy, tool use, and multi-party communication, we document eleven representative case studies. Observed behaviors include unauthorized compliance with non-owners, disclosure of sensitive information, execution of destructive system-level actions, denial-of-service conditions, uncontrolled resource consumption, identity spoofing vulnerabilities, cross-agent propagation of unsafe practices, and partial system takeover. In several cases, agents reported task completion while the underlying system state contradicted those reports. We also report on some of the failed attempts. Our findings establish the existence of security-, privacy-, and governance-relevant vulnerabilities in realistic deployment settings. These behaviors raise unresolved questions regarding accountability, delegated authority, and responsibility for downstream harms, and warrant urgent attention from legal scholars, policymakers, and researchers across disciplines."

AI, Human Cognition and Knowledge Collapse.

The idea here--presented by many others in similar forms--is that AI is only useful to those who have the means to put its output in proper context. This requires experiential (i.e. tacit) knowledge and a comprehensive understanding of the field of inquiry.

Those with little experiential knowledge and only a shallow grasp of the field accept AI as "the truth" because AI mimics understanding so fluidly. This fluidity replaces human learning from experience, and the net result is ignorance masquerading as knowledge becomes the norm.

When the system is challenged by novel crises / asymmetries, AI reveals its core flaw--it's untrustworthy--and the system collapses.

I want to stress that the idea here isn't that AI has no utility; the idea here is the utility (i.e. real Progress) comes with built-in limits and downsides (Anti-Progress) that cannot be eradicated with coding tweaks. The evidence is mounting that much of AI is automated Ultra-Processed Cognition that many people feel obligated to enthuse about lest they appear out of step with the In Crowd which harvests status by being an Early Adopter of The Latest Tech Thing.

Hundreds of billions of dollars are being sunk into AI with increasingly short half-lives as everyone races to replace the Latest Iteration. What is glaringly obvious but too disruptive to admit openly is there are few realistic prospects for profitability. Much of the funding comes from what my colleague Tim Morgan (Surplus Energy Economics) calls the 'ads and algorithms' business model--reaping enormous profits from selling marketing and engineering algorithms to be addictive and extractive ("dynamic pricing", etc.).

Marketing and algorithms can only generate massive profits in a free-spending consumer economy that depends on ever-expanding debt-fueled spending and ever-expanding resource extraction: we need more jet fuel to expand leisure travel, and more lithium and other minerals to power electric aircraft, flying cars, etc.

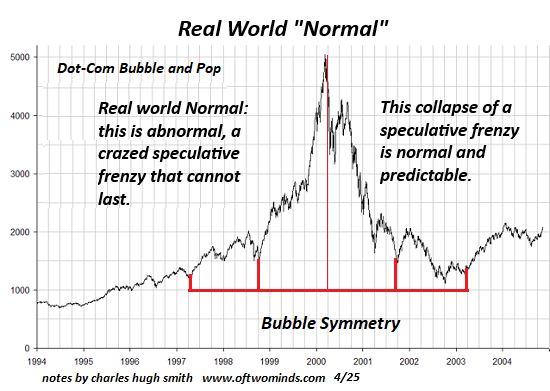

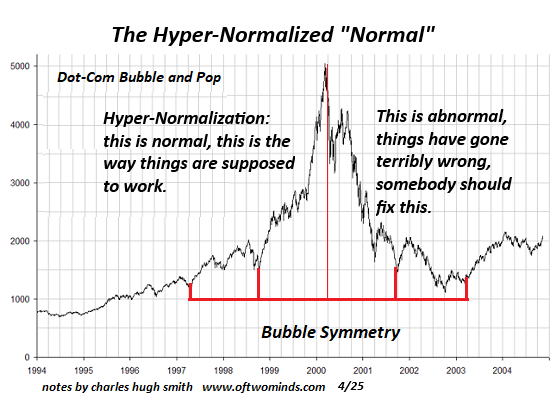

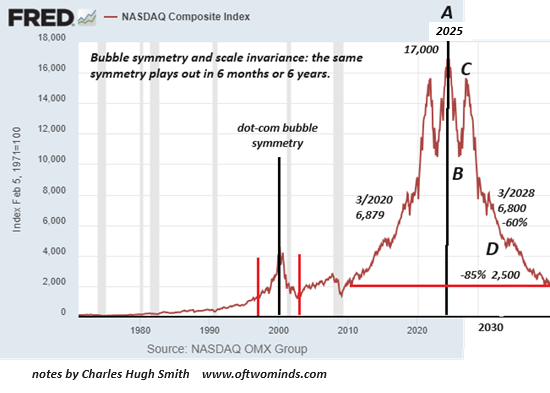

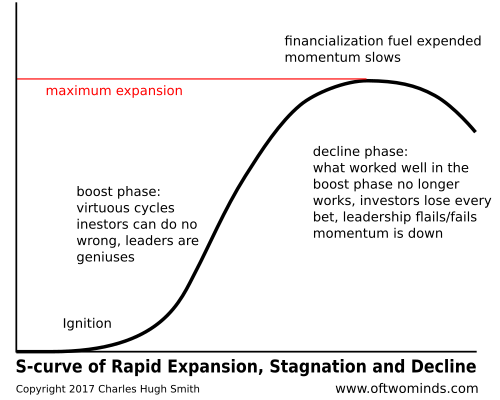

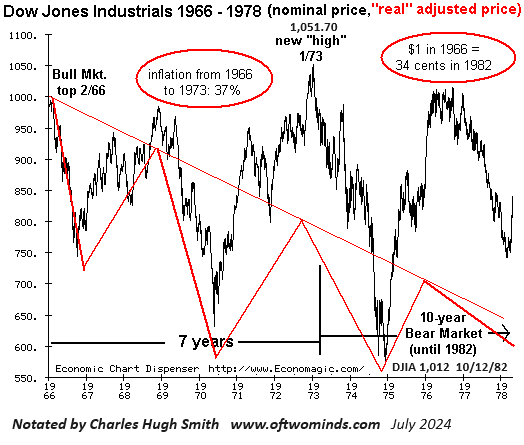

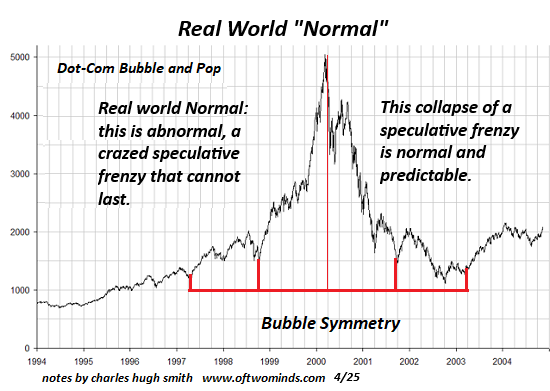

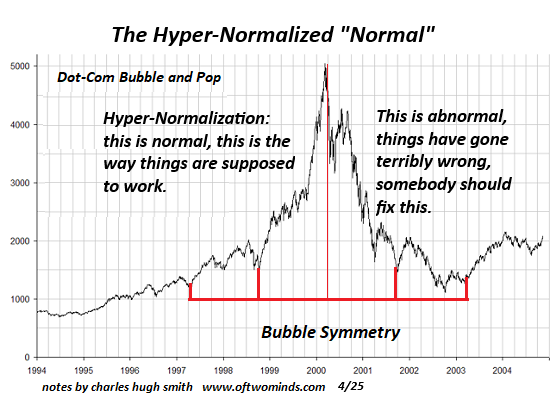

That this free-spending consumer economy is also self-liquidating is taboo: growth at any cost demands debt expands fast enough to fund the Waste Is Growth Landfill Economy, which itself demands ever more resources to be squandered and tossed in the landfill (i.e. "consumed"). Here is "growth" in action:

Here is an artificial mountain of Waste Is Growth consumption:

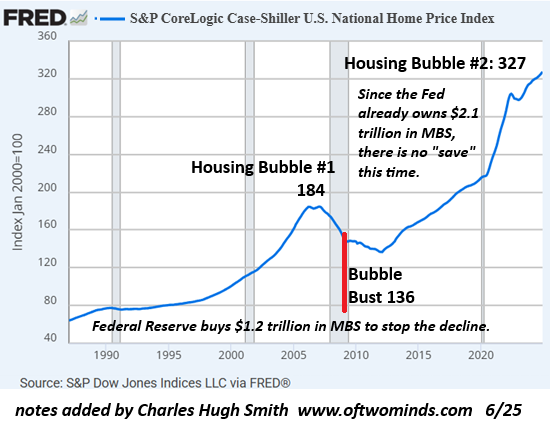

Abundant credit generates credit-asset bubbles that pop with devastating consequences, and squandering resources on the belief that ingenuity and AI will magically replace easy-to-extract resources with hard-to-get resources at the same cost and rate of expansion leads to higher costs and scarcities that eventually limit the "growth" the system needs to avoid collapse.

Both pathways rest on the quicksand of moral decay: per Adam Smith, capitalism only functions as the idealists believe--allocating capital and resources with unmatched efficiency--if there is a culture and social structure that imposes a moral order on how private gains are amassed.

In the present era of moral collapse, the ideal way to amass private gains is by establishing a monopoly or cartel that fixes prices and buys political protection in a thoroughly corrupted political system: "democracy" as an open auction for political favors.

AI fits seamlessly into this extractive, self-liquidating system: AI will boost profits by replacing costly human labor. The owners of AI and the owners of sectors that buy AI will profit immensely. That's all we need to know about it.

No one claims AI will fix the moral rot that is as self-liquidating as Waste Is Growth consumerism, credit-asset bubbles and AI. AI is just a tool the monopolies and cartels are seeking to control and profit from--in effect, automating moral decay.

If AI fails to be profitable, then the hundreds of billions will wash away as mal-investments that cannot be replaced with new capital. That failure will generate a different flavor of Depression, one accelerated by the self-liquidating collapse of credit-asset bubbles and the Waste Is Growth consumption that depended on those bubbles expanding forever.

AI automates Ultra-Processed Cognition and moral decay. Narrative control--AI is going to make us all rich!--doesn't change the self-liquidating nature of the system and its supposed savior, AI.

My book Investing In Revolution is available at a 10% discount ($18 for the paperback, $24 for the hardcover and $8.95 for the ebook edition).

Introduction (free)

Check out my updated Books and Films.

Become

a $3/month patron of my work via patreon.com

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Glenn W. ($70), for your magnificently generous subscription

to this site -- I am greatly honored by your support and readership.

|

|

Thank you, Sebastian S. ($80), for your marvelously generous subscription

to this site -- I am greatly honored by your support and readership.

|

|

Thank you, JJA T. ($70) for your superbly generous subscription

to this site -- I am greatly honored by your support and readership.

|

|

Thank you, Louis N. ($7/month) for your splendidly generous subscription

to this site -- I am greatly honored by your support and readership.

|

Read more...